13 May 2016 | 10:31 UTC — Insight Blog

China's commodity exchanges capable of cooling any futures trade frenzy

By Hongmei Li

Roller-coaster game is the best metaphor to describe what has happened to China’s steel, coking coal, coke, and iron ore futures in the past two weeks where prices are concerned. And of course, not surprisingly, the exchanges — as the watchdogs — have contributed to the price fluctuation since over April 21-May 10.

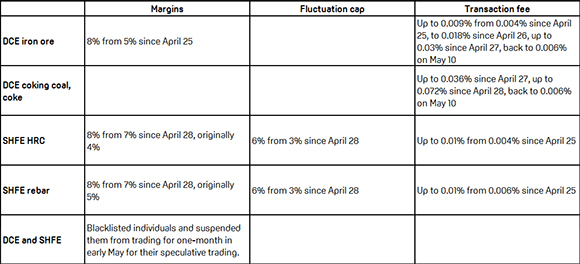

The Shanghai Futures Exchange (SHFE) and Dalian Commodity Exchange (DCE) both intervened a few times too during the past two weeks just to cool the trading frenzy in their respective rebar, hot-rolled coil and iron ore, coking coal and coke futures contracts, via the means of raising the daily price fluctuation caps, transaction fees, margins, and blacklisting those individuals that have been too frequently opening and closing positions on the daily basis, blocking them from trading for one month.

Besides, SHFE also shortened the night trading hours of rebar and HRC to 2100-2300 Beijing time starting May 3 from the original 2100-0100. This was welcomed by a Shanghai trader, saying, “Finally I can get some sleep instead of staying up late into the midnight.”

Related podcast: Will China's commodity exchanges be able to create international commodity benchmarks?

The bourses have taken these steps after future prices of all the above commodities hit daily caps on April 21 amid high trading volumes. This concerned China's central government, as it will inflate physical values and thus make it more difficult for Beijing to tackle overcapacity in the steel sector.

However, the frenzy of speculative trading in iron ore, coking coal, and coke futures — mainly by individuals — will only multiply the risks and expose investors to greater vulnerability, it added, confirming the Chinese market sources’ understanding.

A Beijing-based iron ore trader felt the impact keenly. “No one had expected physical iron ore price to have swung by $10/dry mt in a few days to hit $70/dmt in late April, as fundamentals, changing little, are unlikely to have caused such dramatic moves. So, it has been because of the iron ore futures on DCE, as too many people are speculating on it,” she said.

These emergency measures “have sent a strong message to investors, especially to individual investors, that recent price surges in steel-related futures are not welcome at all,” a Beijing-based steel analyst noted.

He acknowledged many more individuals in China have jumped into iron ore and steel futures trading.

The two exchanges’ cooling efforts have been effective so far — SHFE’s HRC trading volume, for example, dropped 15.1% day on day to 239,533 lots as of April 26, while that of DCE’s most popular September iron ore futures contract slumped 49% from April 21 to 3.3 million lots as of April 26, the exchanges’ data showed.

Declines have been continuing in the past two weeks, and as of May 10, the Platts IODEX for 62% fines was assessed at $56.1/metric ton CFR North China, down 20.5% from April 21’s high, and the billet price in Tangshan, north China’s Hebei province, the barometer of China’s steel market, fell to Yuan 1,920/mt ($294.5/mt) as of May 10, down 27.3% or Yuan 720/mt from the recent high on April 21.

The battle between speculative trading against the regulators’ intervention has illustrated explicitly that China’s futures market is yet to be 100% free-willed, and it will be under the close watch and surveillance to serve the “greater good” that is so full of Chinese characteristics.