18 Jan 2017 | 10:31 UTC — Insight Blog

Gold skips the January blues

Unlike the rest of us, gold loves Januaries. Up just over 5.5% year-to-date, sailing through two-month highs above $1,215/oz this week on Brexit and Trump uncertainty, gold has seen gains in the first month of the year for nearly two-thirds of the past decade and a half.

In fact, 65% of Januaries have recorded gains since 2001.

| January | Gain? | Year end | Gain? | |

| 2001 | -2.4% | N | 2.0% | Y |

| 2002 | 1.4% | Y | 24.7% | Y |

| 2003 | 6.9% | Y | 21.1% | Y |

| 2004 | -3.7% | N | 4.9% | Y |

| 2005 | -1.3% | N | 23.9% | Y |

| 2006 | 7.4% | Y | 19.4% | Y |

| 2007 | 1.7% | Y | 30.3% | Y |

| 2008 | 9.0% | Y | 2.7% | Y |

| 2009 | 5.1% | Y | 24.4% | Y |

| 2010 | -3.8% | N | 25.3% | Y |

| 2011 | -4.4% | N | 10.3% | Y |

| 2012 | 9.1% | Y | 3.7% | Y |

| 2013 | -1.7% | N | -28.9% | N |

| 2014 | 2.1% | Y | -1.6% | N |

| 2015 | 7.5% | Y | -9.6% | N |

| 2016 | 2.7% | Y | 5.9% | Y |

| 2017 | 5.6% | Y | ||

| Yes | 65% | 81% | ||

| No | 35% | 19% |

Is it something to do with sentiment at the beginning of the year: a post-Christmas hangover that falls into sentiment the first week of January? As we know, risk-off sentiment feeds well into gold prices. Or is it something more significant — say, the time of year when physical demand peaks in the large consuming Asian countries?

Taking the S&P 500 as a (rudimentary) guide to market sentiment, we can see that 65% of the time when the index falls over January, gold has a positive month — and vice versa.

In fact, it is true for four of the last five years from 2012 to 2016 and seven of the last 10 years. So if anything, the correlation has been getting stronger. Except, however, this year: the S&P remains in positive territory, for now, up just below 1% year-to-date.

What about the dollar, so often the main driver of gold prices in recent years? Looking back at the US Dollar Index over the last eight years, its relationship is surprisingly weak: A falling dollar in January has only coincided with a rising gold price, or vice versa, 40% of the time. The opposite relationship in fact appears more true: the dollar and gold price moving the same way more often than not. Except, again, this year.

| January moves | |||

| Gold | S&P500 | USDX | |

| 2008 | 9.0% | -4.7% | -1.0% |

| 2009 | 5.1% | -11.4% | 4.4% |

| 2010 | -3.8% | -5.2% | 2.3% |

| 2011 | -4.4% | 1.3% | -2.3% |

| 2012 | 9.1% | 2.8% | -0.6% |

| 2013 | -1.7% | 2.4% | -0.9% |

| 2014 | 2.1% | -2.7% | 0.8% |

| 2015 | 7.5% | -3.1% | 4.0% |

| 2016 | 2.7% | -3.6% | 0.7% |

| 2017 | 5.6% | 0.9% | -1.4% |

So does this suggest something else about January, given it comes at a time when physical buying peaks in both China and India?

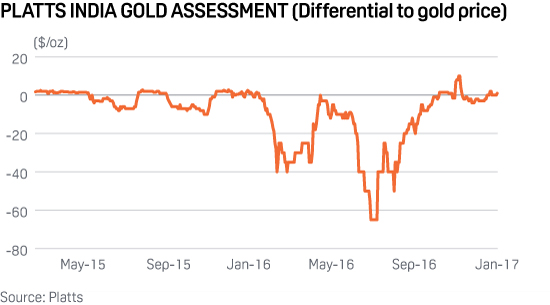

The differential paid for gold in both countries have been positive since the start of the year, with premiums in China reported at $15-20/oz this week ahead of its New Year holidays next month. India — which spent nearly the entire 2016 in discount — has been in premium since January 1, its longest period since, you guessed it, last January.

India and China account for over half the world’s physical gold consumption, with demand in both countries usually seen as a floor to prices falling too low. Given the huge slide in Indian demand in 2016 (expected to come in at half 2015’s level at around 500 mt), a January lift in demand could finally have an impact on prices. In fact, sources in India have been talking about consumers returning to the market feeling that prices may have bottomed out. Unlike western consumers, Indian investors notoriously buy gold at the bottom and are happy to wait out peaks.

In China, currency controls have made headlines in recent weeks as the People’s Government attempt to shore up the yuan, but it has also pushed consumers towards gold, with premiums above $30/oz before Christmas. However, the currency controls have also included strict limits on gold purchases by banks operating in the country, so its impact on international gold demand in recent weeks, and therefore prices, may be limited.

Either way, gold’s tendency to do well in January is hard to explain without looking at both investment and physical demand.

Or, perhaps, it’s just a psychological trade as investors return to work after two weeks of drinking and eating too much (a number of studies into trading psychology talk about a January-effect in equity markets). While for the last two years, December just happened to be when the US Federal Reserve Board lifted interest rates.

Either way, over the course of the year, a bright January doesn’t mean much ... the last three years have averaged just over 4% returns in January and we know how that ended.