28 Oct 2016 | 10:31 UTC — Insight Blog

Northeast US power gen mix still malleable as winter approaches

By Eric Wieser

Winter is around the corner and for regions like the Northeast it can mean a shifting power generation picture.

And because the Northeast has increasingly turned to natural gas for its generation needs as older power plants have retired, it further puts Northeast power prices at the whim of natural gas prices.

This is nothing new to stakeholders in the region.

During past winters, spot natural gas prices, and therefore power prices, have become extremely volatile as generators compete with residential and commercial customers for the substance in the pipes.

To cope with, or avoid, these episodes of volatility, some dual-fueled generators switch to fuels that are more economical at the time, such as fuel oil, to produce electricity.

Looking at data for the months of January and February going back to 2011, oil-fired generation contributed between less than 1% to as much as 27% of the daily ISO New England generation mix.

Since 2013, the ISO-NE has operated a winter reliability program, developed as a way to help incentivize these generators that switch to ensure proper fuel inventory levels heading into the winter season.

The program pays the generators a portion of fuel costs related to any unused inventory levels at the end of winter.

This year there are 85 oil-fired units that are expected to participate in the winter reliability program, 8 more than last year's program. These units commit to the program in October, which means stockpiling ahead of winter.

S&P Global Market Intelligence data for the ISO-NE region shows a majority of oil purchases for past few years being done in October and November.

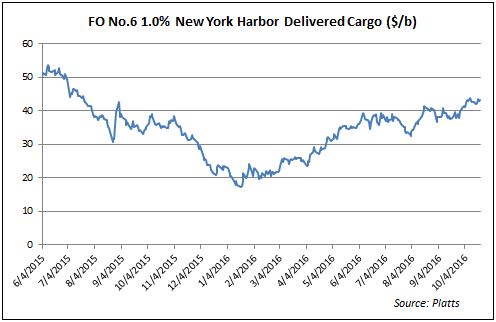

Currently, fuel oil No. 6 1% New York Harbor Delivery prices are assessed by Platts in low $40s/b range, which is 83% higher than where they sat at the start of year.

At this time last year, fuel oil No. 6 1% New York Harbor Delivery prices were around mid-$30s/b and ended the year lower in low $20s/b.

Shifting over to forward gas markets shows two of the most liquid Northeast natural gas trading hubs — Algonquin Citygate and Transco Zone 6 New York — shaping up differently from past years.

Typically ahead of winter, Algonquin forward prices have been higher than Transco Z6 NY.

However, January and February Transco Z6 NY forward gas prices are at a premium to Algonquin.

There has been rumblings in marketplace that Algonquin AIM pipeline expansion project slated to come on later this year has contributed to these pricing dynamics.

As far as weather goes, the National Oceanic Atmospheric Administration calls for equal chances for the Northeast to see normal precipitation and temperatures this winter.

But whether the region uses natural gas or oil-fired generation to meet electricity demand during any extremely cold days, the market could expect some volatility and a shift in generation mix if history is any indication.