11 Feb 2019 | 12:00 UTC — Insight Blog

Balance of power tilts towards renewables in Asia Pacific

By Eric Yep

Renewable energy sources are now a commercially profitable business in many parts of Asia Pacific without government largesse and subsidy support. But the renewables story has just started.

Primary energy demand in the region is expected to grow by over 40% to 2040, based on the International Energy Agency’s central scenario, accounting for two-thirds of global growth.

Renewables will play a major role in meeting the new demand, their expansion supported by rapidly falling costs of key technologies, the drive to reduce air pollution, particularly in China, and the rising popularity of electric vehicles that is pushing forward battery technology.

A tipping point now looks close on multiple fronts. Here are six trends that will have a decisive impact on the renewables landscape in the Asia Pacific region.

China’s last new coal plant in sight

There’s a joke that the Chinese government’s facial recognition technology is so advanced because it has to operate in hostile conditions like the thick smog that regularly envelops Beijing city.

Chinese cities have been some of the most polluted in the world on the back of rapid industrialization and coal consumption. The government tried to remedy this with its "war against pollution" that initially covered 28 major cities including Beijing and Tianjin.

Go deeper - The Chinese dream: Energy and commodities in an era of change

In July 2018, it expanded the initiative to other pollution hotspots like the provinces of Shanxi, Shaanxi and Henan and the industrial hubs of the Yangtze River Delta.

China’s blue sky policy, the enforcement of coal-to-gas switching, and the structural shift in China’s economy to a consumer base from an industrial base will ensure its last coal-fired plant is built sometime in the next decade.

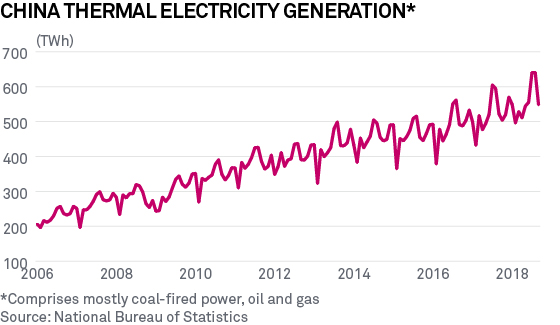

While China’s overall energy demand will continue to rise, an increasing proportion of the growth will come from natural gas, renewables and nuclear, especially as coal demand growth plateaus.

Several indicators show China’s coal demand growth hitting a wall.

China’s coal demand grew by 8.9% per year on average over 2000-2013 and contributed more than three-quarters of total energy demand growth over that period. By 2017 it constituted around two-thirds of China’s energy demand, according to the IEA.

In its 2018 report, the IEA said investment in new Chinese coal-fired power plants in 2017 fell to its lowest level in a decade, and while capacity additions were still larger than retirements, they had slowed dramatically.

“The boom years for coal-fired power investment, driven by an extraordinary expansion of capacity in China in the 2000s, are over,” the IEA said.

It said that once plants currently under construction enter into service, the rate of capacity additions will slow sharply along with a marked shift in the technologies being deployed in favour of more efficiency and lower emissions.

“China had been adding about 47 GW of coal [plants] per year over the past decade, but the pace of the coal additions has been steadily declining from a high of 51 GW in 2015 to only about 40 GW in 2017,” according to S&P Global Platts Analytics’ December report.

Beijing has restricted many provinces from adding new thermal capacity to the grid, but the provinces have been finding loopholes to proceed with the projects. Regardless of a further crackdown by the government, overcapacity will force the pace of new coal plant construction in China, the world’s largest coal user and producer, to decelerate further.

“Our view is that coal-fired generation will peak in the early to mid-2020s, although that peak could come earlier if renewables growth continues to surprise and the nuclear newbuild continues to be successful,” Platts Analytics said.

Indian solar becomes cheaper than coal

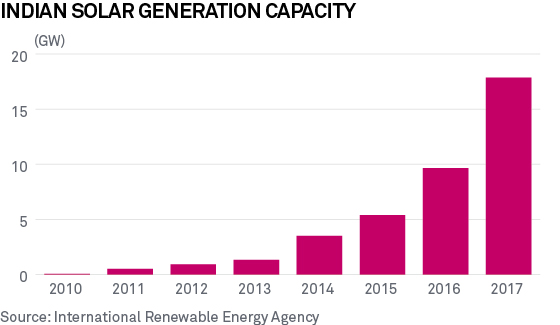

India has become one of the largest solar markets in the world.

This is primarily due to one important milestone – it is now cheaper to build 1 MW of a renewable energy project than an equivalent amount of coal-fired power, without subsidy support. The next key marker will be when the cost of renewable energy becomes cheaper than operating an existing coal plant.

India has the cheapest new wind and solar anywhere in the world, according to Bloomberg New Energy Finance, which says that while coal-fired electricity will continue to grow in the short to medium term, by 2050 wind and solar will dominate, supported by batteries and gas for flexibility.

New Delhi has laid out a renewables target of 175 GW by 2022, of which 100 GW will be solar and 60 GW wind energy; and a 2027 target of 275 GW renewables of which 150 GW will be solar and 100 GW wind.

It proposes to generate 46.5% of its electricity demand from non-fossil fuels by March 2022, including nuclear, hydro and other renewable sources, and increase this to 56.5% by March 2027. Currently, these sources account for 36.16% of electricity demand.

“The 2022 wind target is fairly realistic, with its 2027 target potentially harder to achieve absent additional policy measures to compensate for lower resource potential,” Platts Analytics said, adding that Indian solar installations will continue to grow through 2040, driven in part by ongoing competitive state auctions, although the magnitude of its targets as well as fiscal constraints will be challenging.

In October 2018, India announced that it had the fifth-highest solar installed capacity in the world of 24.33 GW, and the fourth-highest wind installed capacity in the world of 34.98 GW.

EVs will redefine mass power storage

Both in Asia and elsewhere, the biggest challenge in the growth of renewables is intermittency. 1 MW of solar or wind does not have the same round-the-clock stability as 1 MW of coal.

One way of filling the gap is battery storage, which is expensive and not commercially feasible for more than one or two hours today. The next renewable energy growth cycle is contingent on the development of low-cost battery technologies.

However, battery demand in the power sector is dwarfed by the automobile sector. And the economies of scale for EV battery production are much greater than in the utilities sector.

“Battery costs’ reductions are driven by increases in manufacturing scales driven by electric vehicle (EVs) growth expectations and improvements in chemistries that increase the energy density and reduce material needs,” according to Platts Analytics.

When EV production scales up it will drive down battery costs and increase the penetration of renewables in the energy mix, similar to how mass commercialization of lithium-ion batteries in electronics like smartphones made it possible for carmakers to produce the first wave of EVs.

Projections of demand for core battery metals give an idea of the scale of battery demand from EVs versus power grids. Glencore estimates nickel demand from non-petroleum vehicles at nearly sevenfold of grid storage by 2030 and cobalt demand will be nearly five times more.

Battery technologies are far from being fully standardized and are still evolving. Platts Analytics expects lithium batteries to remain the primary technology in the near to medium term, although the degree of convergence between EV and power markets will depend on supply and demand dynamics.

Battery manufacturing capacity was below 50 GWh per year in 2016, but annual capacity could reach more than 300 GWh within the next five years, with two-thirds of new capacity coming from plants in China, Platts Analytics said.

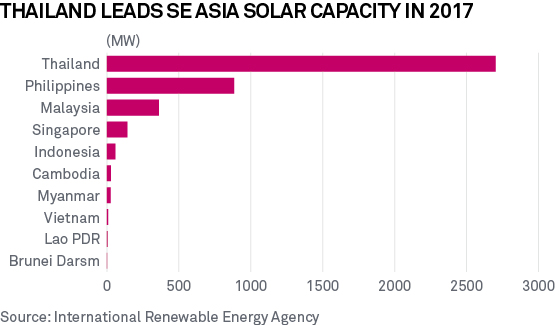

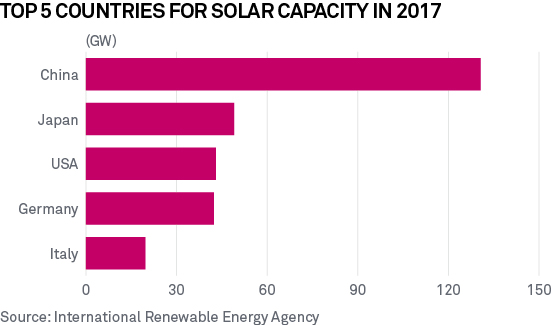

Solar power thrives in Thailand

Thailand is unique among developing Asian countries for consciously minimizing coal use in its power generation mix, due to a history of environmental and human casualties at coal-fired mines and power projects.

It generates nearly 67% of its power supply from natural gas, 22% from coal and lignite, and the remaining 11% from renewables like solar, hydro and biomass, according to official data.

In terms of absolute capacity, Thailand not only has the most solar power generation capacity in Southeast Asia, it has added more solar capacity in the last five years than the rest of Southeast Asia combined.

In 2017, Thailand had 2,702 MW of solar generation, up from 49 MW in 2010, and compared with 1,515 MW in the rest of Southeast Asia combined. The Philippines came in at second place with 885 MW of solar, according to the International Renewable Energy Agency.

“Other regions can quickly catch up. We expect the solar capacity in Thailand to increase over threefold in the next 10 years and escalate further once the storage technology becomes commercial,” said Dr Bikal Pokharel, research director at Wood Mackenzie.

“We expect the share of gas in the mix to stay close to 50% by 2036,” he said, adding that dependence on LNG imports will increase as domestic and piped gas imports decline, and LNG will form more than 50% of the gas demand by 2036.

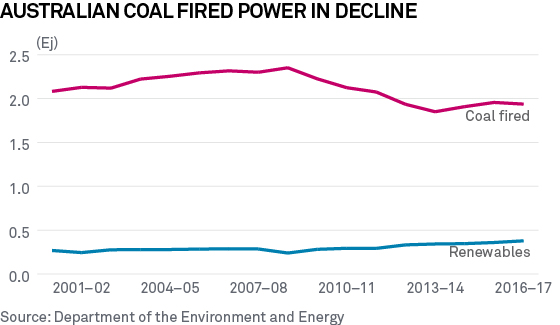

Australia’s turbulent transition to renewables

Australia is the world's largest coal exporter and coal ranks as the second-largest export commodity for Australia in terms of revenue, according to the US Energy Information Administration.

Yet the country is unlikely to build another coal-fired power plant, despite 63% of its power supply coming from the fossil fuel. Australia is a case study on how to, and sometimes how not to, make the transition from fossil fuels to renewables, as it struggles with the planned phase-out of old coal plants and the associated risks to energy security.

A massive power outage in South Australia in 2016 exposed the dangers of phasing out coal without contingency plans, to the extent that Tesla founder, Elon Musk, took up the challenge of building one of the world’s largest batteries in the state in record time.

The lack of a comprehensive national-level energy policy has not helped matters.

“The uncertain landscape continues to undermine investor confidence to plan and undertake investment in new generation capacity to meet variable market conditions,” according to a report by S&P Global Platts Ratings published last September.

It said Australia's energy policy uncertainty is delaying vital investments in system reliability amid a number of large-scale coal plant retirements in the coming decades.

However, its investments in renewables are still being driven by lower technology costs of wind turbines and solar panels compared with conventional coal or gas-fired generation. Individual state-based targets and renewable schemes, and international investors attracted to the Australian market are also factors supporting renewables growth.

China’s curbs on solar have global impact

China accounts for more than half of global solar demand and manufacturing.

But in May 2018, the Chinese government halted government support for its solar sector including the removal of subsidies, which had resulted in a growing deficit of several billion dollars at its Renewable Energy Development Fund.

The National Energy Administration also wanted to cool down the sector, as rapid growth has led to overcapacity concerns, and focus on improving the connectivity of solar plants to the power grid rather than adding more unused capacity.

The new policy went further to state that no construction quota would be allocated for utility-scale plants, and a quota for distributed generation was set at 10 GW, among other curbs.

This has massive implications for solar markets globally.

“The first impact of the policy is that we lowered our China PV demand forecast for 2018-20,” said Yvonne Yujing Liu, solar power analyst at BNEF, adding that it also resulted in a more significant equipment price drop that depressed global prices.

BNEF estimated that the utility-scale PV market in China contracted by more than a third in 2018 because of policy revisions. Liu said solar equipment manufacturers were under great price pressure, and developers and investors had been forced to cancel and postpone entire project pipelines.

“On the other hand, overseas PV developers can now enjoy cheaper equipment from China,” she added.

Researchers at Wood Mackenzie said China’s curbs created a global wave of cheap equipment that reduced the benchmark global PV cost to $60/MWh in the second half of 2018, a 13% drop from the first half of 2018.

With costs for solar equipment plunging globally, there is now a big incentive to build more solar projects outside China.