31 Jan 2019 | 15:33 UTC — Insight Blog

UK electricity links to Europe multiply, even as Brexit looms

Featuring Glenn Rickson

This week marks the start of a new phase in London-Brussels relations. But it has nothing to do with Brexit, and it won't be political power returning to Westminster as a result of the UK's departure from the European Union.

Instead, the power flowing across the English Channel will be of the electrical variety, as the Nemo electricity interconnector - the first direct connection between the UK and Belgium - begins commercial operations on 31st January. The 1 GW link will be capable of supplying enough power to meet the electricity needs of 2.2 million UK homes.

Nemo is the first new interconnector between mainland Europe and the UK in 7 years and the timing of the link's start-up is loaded with irony. Just as the UK is on the brink of severing its political connections with the rest of Europe, Nemo marks the first of a number of new planned subsea electricity interconnectors that will bind the UK more closely to Europe's power markets than ever before.

Until now, the UK has had just two means of exchanging power with mainland Europe - the 2 GW IFA interconnector with France, which first came online in 1986, and the 1 GW BritNed interconnector with the Netherlands, connected in 2012. It also has 1 GW of interconnection with the island of Ireland - which since 2007 has operated as a Single Electricity Market (SEM) that unites Northern Ireland and the Republic of Ireland. Here too, electrical union has proved more palatable than political union, though a ”no-deal” Brexit requiring a ”hard” border between the north and south of the island would jeopardise the future of the SEM.

Go deeper - Outlook 2019: UK power hits peak uncertainty

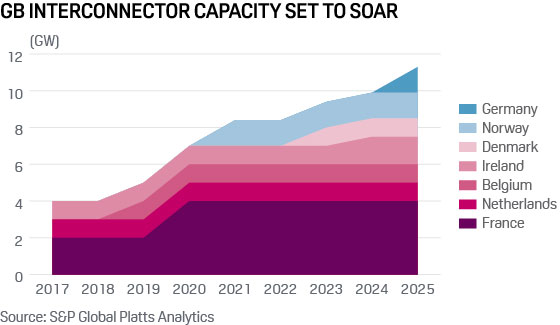

But Nemo marks the start of a new wave of interconnector projects - with a host of new subsea cables to countries including Germany, Norway and even Iceland at various stages of the planning process. In total more than 30 GW of new interconnection capacity between the UK and its neighbours has been proposed – enough to meet more than 50% of peak demand. Platts Analytics forecasts just 8GW of this will be built between 2019-2025, as the chart below shows. But this still represents a trebling in interconnection capacity vs pre-Nemo levels.

UK as premium market

Historically the UK power market has been priced at a premium to its mainland European counterparts, meaning that power has generally flowed from France and the Netherlands to the UK via the IFA and BritNed cables respectively. The premium in the UK is partly a reflection of its more expensive generation mix - with a greater proportion of coal and gas than France's nuclear-dominated capacity mix.

But a bigger factor in recent years has been Britain’s Carbon Price Support (CPS)– currently set at £18/metric ton of CO2 equivalent. The CPS, introduced in 2013, is a tax that applies to carbon-emitting generators in Great Britain – it excludes Northern Ireland. The tax is in addition to the cost of carbon allowances under the EU-wide Emissions Trading Scheme, currently priced at around €23/mt for the December 19 contract. The CPS is set to remain in place until at least 2021, while the UK government has said that in the event of a no-deal Brexit - which would require the UK to leave the EU ETS -it would impose a further £16/mt carbon tax to keep the total carbon cost for GB generators broadly unchanged from 2018 levels.

S&P Global Platts Analytics expects that the UK power price will retain its premium to Belgium until the middle of the next decade, and that the Nemo interconnector will flow power from Belgium to the UK on a net average basis. In summers, when the discount in mainland European power prices to their UK equivalent is typically widest, we assume Nemo flows at its full 1GW capacity into the UK. This should put further pressure onto the profitability of UK thermal generation.

S&P Global Platts Analytics forecasts clean spark spreads – a measure for gas plant profitability – for summer 2019 (Q2+Q3 2019) at only £0.6/MWh, or £2.2/MWh below summer 2018. Further interconnectors – including the 1 GW ElecLink connection with France, scheduled to start in early 2020, will weigh even further on UK gas and coal plant profitability in the coming years.

Coal has already largely been priced out of the market in UK summers. Generation has fallen by 95% in the last five years to just 0.6 GW in Summer 2018 and is forecast to fall to just 0.2 GW in Summer 2019. Platts Analytics forecasts that gas generation will fall by 2 GW (or 17%) year-on-year in Summer 2019 to 10GW, due to a combination of increased imports and an assumed 1.2GW increase in wind generation vs Summer 2018.

Winter risk

While we expect the UK to consistently import from Belgium in summers, the story is more nuanced for winter periods. On average the UK has imported from mainland Europe in winters too, and Platts Analytics expects this to continue under normal conditions. But recent months have shown the vulnerability of Belgian power prices to severe spikes, largely due to the unreliability of the country’s nuclear fleet. The ageing Doel and Tihange nuclear reactors have suffered a series of extended outages in recent years and problems this winter saw Belgian power prices rise to record highs.

Under such circumstances the UK would have been exporting at maximum to Belgium if Nemo had been online, and as recently as December, forward spreads for February 2019 indicated that the first month of Nemo’s operation would see the UK exporting to Belgium as a result of the latter’s nuclear supply issues. However, these issues have since subsided as plants have returned online and the UK-Belgium price spread has recovered to positive, implying UK imports from Belgium. Platts Analytics forecasts an average 0.2GW of imports to the UK via Nemo in February.

But on January 29, Engie, the operator of Belgium’s Doel and Tihange nuclear plants announced a revised outage schedule that would see Tihange 1 (1.0 GW) and Doel 1&2 (0.9 GW combined) offline for most of next winter. Another winter of heavy nuclear outages in Belgium would sharply lift the probability of Belgium, and potentially France, needing to pull on the UK for power at times of high demand. So while the startup of Nemo should on average push UK prices down, we also expect the risk premium for Belgian winter power prices to decline as the market has another potential source of power in the event of another supply crunch. In other words, Nemo is a win-win story of integration for Europe’s power markets. Now, about Brexit…