01 Nov 2018 | 12:00 UTC — Insight Blog

Insight from Shanghai: China courts international traders with new crude contract

The Shanghai International Energy Exchange’s crude oil futures contract has got off to a good start.

The contract’s first expiry at the end of August marked another step on the road to developing a crude futures contract that China hopes will one day stand alongside ICE Brent and NYMEX light sweet crude.

The launch of the Shanghai contract on March 26 this year also coincided with the “internationalization” of other Chinese derivatives. Less than two months later, the Dalian Commodity Exchange’s well established iron ore contract was also opened up to international investors.

In actual fact, foreign companies have been able to trade Chinese commodity futures onshore for some time. But to do so requires setting up a domestic Chinese entity, with all the associated costs and approvals operating a company in China requires. By internationalizing futures contracts and making it easier for overseas capital to participate directly in price formation in China, the hope is that local exchanges will vie for international influence with incumbents like the Chicago Board of Trade, Intercontinental Exchange and the London Metal Exchange, which host many global agriculture, energy and metals benchmarks.

China’s leaders hope not only that Chinese exchanges will become international centers of price discovery, but also that prices discovered on these venues will become the benchmarks that are used to price commodities sold to China. Should this happen, these contracts will support another government objective: the internationalization of China’s currency, the yuan.

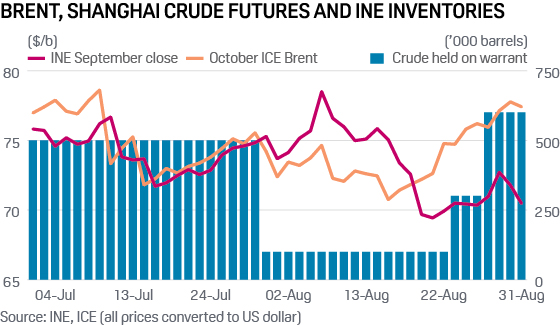

Good start

Volumes for the Shanghai contract have steadily grown, with 3.4 billion barrels traded in August, a fifth of the volume for ICE Brent during the same month. ICE Brent marked its 30th anniversary this year; the Shanghai crude contract has only been in existence for six months.

However, liquidity is rarely a problem for Chinese futures exchanges, which host a number of well-established metal and agriculture derivatives. Many of these have higher trading volumes than international benchmarks hosted on platforms like CBOT and LME. Outside China, institutional investors and companies hedging physical exposure tend to be the main users of commodity derivatives. In China, retail speculators dominate.

This can clearly be seen by looking at exchange statistics. Open interest – positions held open at the end of the day and a measure of the contract’s use for physical hedging – is typically significantly larger than daily trading volume for contracts such as ICE Brent. This is because many traders are holding positions to expiry to hedge physical positions. In China, the presence of significant numbers of retail speculators trading in and out of positions boosts daily volume, which can at times exceed open interest.

At times, these speculators exacerbate price volatility, rushing into the momentum of a rising market only to exit just as quickly as the market turns. Allowing overseas capital to play a greater part in price formation could improve price discovery and reduce the influence of domestic speculators, as foreign players arbitrage away differences in price between Chinese and overseas venues.

Supply vs. demand

Existing crude benchmarks tend to reflect the price of oil close to the source of production or distribution. For example, Brent and Dubai are widely used to price light sweet and medium sour crudes. They represent the price of crude loading on ships from the North Sea and oil fields in the Middle East. WTI, on the other hand, reflects the price of crude delivered to Cushing, Oklahoma, a small town that sits at the nexus of a myriad of pipelines connecting producers with refiners across the US.

The Shanghai crude contract reflects the price of crude oil held in tanks at one of eight approved storage sites. These are located up and down the coast close to refining centers.

The contract can be settled by physical delivery. Normally, this is by transfer of a warrant – a receipt that allows the holder to take delivery of oil held in a specific tank – from the seller to the buyer. The seller chooses the grade and location of the crude they wish to deliver. This mechanism is similar to the established system of warehouses used by the LME and Shanghai Futures Exchange for the delivery and storage of base metals like copper and aluminum.

The price of crude oil benchmarks like Brent and Dubai depends on a wide range of factors. These include the strength of global demand, inventories, production expectations, macroeconomic factors like interest rates, and geopolitical factors that might pose a risk to supply.

In the case of the Shanghai crude contract, the level of inventory held in INE-approved, as well as non-exchange storage, is also a factor influencing price. If the market believes there is insufficient oil in storage to settle open positions, prices can become volatile, as the market prices in this uncertainty. A fall in INE inventories at the end of July to just 100,000 barrels likely contributed to the volatility of the contract in August ahead of its expiry at the end of the month. Prices had previously been moving in line with other futures like ICE Brent, but rose and fell sharply as oil was removed from and returned to INE storage.

Long road

Chinese buyers currently have to bear exchange-rate risk and costs when they buy commodities priced in dollars. These would be eliminated if they were able to price them in yuan. Should other countries also use the yuan as the basis for pricing their sales and purchases of oil and other commodities, it could provide significant support for the internationalization of the Chinese currency.

But even if the Shanghai contract proves a runaway success, there is a long way to go. Among other things, it would require the Chinese government to liberalize its financial institutions and remove the restrictions that currently stop the free movement of capital in and out of the country.

In the first quarter of 2018, slightly under two-thirds of reported foreign exchange reserves were denominated in dollars, according to the International Monetary Fund. The yuan accounted for 1.4% of total holdings, lower than the equivalent figure for the Australian dollar. So it may be some time yet before the yuan challenges the hegemonic status of the US currency.