15 Jul 2019 | 14:56 UTC — Insight Blog

Commodity Tracker: 6 charts to watch this week

S&P Global Platts editors’ pick of unfolding commodities trends. This week, bunker values at Fujairah plunge, mine overcapacity puts pressure on key battery metal lithium, and US LNG exporters face tight margins over the summer. Plus Chinese refiners' growing taste for Saudi crude, EU CO2 prices and gas and coal profitability.

1. Fujairah bunker values plunge as Middle East risk rises

What’s happening? Marine fuel sales in the Port of Fujairah are estimated to have dropped about 16% in the second quarter versus the first quarter, on continued tensions in the Middle East. Recent alleged tanker attacks in the region have weighed on market sentiment, industry sources have told S&P Global Platts. Fujairah is among the world's top bunkering hubs and lies outside the Strait of Hormuz, which handles about 30% of the world's seaborne crude.

What’s next? Singapore has witnessed an increase in demand due to a slight switch in volumes from Fujairah against a backdrop of tight supply-side fundamentals in the world's largest bunkering port. War risk premiums in the Middle East have also risen after recent tanker attacks, contributing to weaker bunker sales in Fujairah, and the spotlight will remain on the region as geopolitical risk and Iran sanctions keep the oil market on tenterhooks.

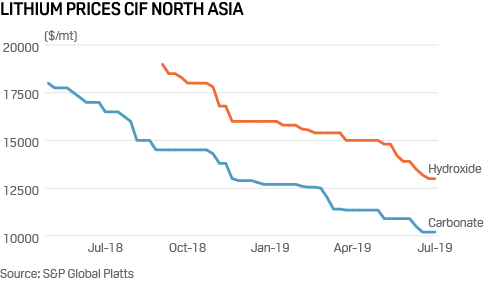

2. Lithium prices continue down on mine overcapacity

What’s happening? Lithium demand is expected to continue to grow between 14% and 16% annually. However, prices are falling from a 2018 peak after miners piled into the market, looking to capitalize on the growing need for battery metals for the electric vehicle sector. Lithium hydroxide has been under pressure because of an oversupply of spodumene. The lithium ore is more frequently converted into hydroxide.

What’s next? Market participants say there is an excess of spodumene production capacity and too little conversion capacity. But more processing capacity is expected to come online outside China, which could ease refining bottlenecks.

3. US LNG exporters’ margins squeezed this summer

What’s happening? The weighted-average netback for US LNG exports is at its lowest in over three years this month at an estimated 14 cent/MMBtu, data from S&P Global Platts Analytics shows. The netback for US exporters has been on a steady decline since September when the Platts JKM benchmark reached a multiyear high at over $12/MMBtu. Tepid demand growth in Asia, and limited capacity in Europe to absorb both strong Russian pipeline volumes and incremental LNG, have left much of the new supply from the US and Australia searching for buyers. Platts Analytics’ netback calculation factors in the cost of feedstock gas, onshore transport, shipping and related fees, but excludes sunk costs associated with liquefaction.

What’s next? The Stronger demand for early-winter cargoes should help to lift the netback on US LNG exports by later this year. JKM swaps for November are currently priced at over $6/MMBtu and first-quarter 2020 in the mid-$7s/MMBtu. At those prices, the netback on US exports would rise to about $2/MMBtu.

4. Gas more profitable than coal in European power generation

What's happening? The TTF Winter gas price is trading below the European coal switching price index (CSPI) and is expected to continue to trade at a discount in the near future. The CSPI is the theoretical threshold for a 50%-efficient, higher heating value gas-fired power plant to be more profitable than a 35%-efficient coal-fired power plant including emissions. The TTF discount means that gas for use in the power generation sector will theoretically be cheaper than the use of coal through the winter, having already proven to be cheaper in the summer months.

What’s next? Gas prices are at historically low levels despite having rallied in the past week, but how those prices evolve in the coming months will define how profitable gas-fired power generation will continue to be. The movement of the coal price and the trend for CO2 allowance prices are also indicators to watch – both are key to the CSPI.

5. Saudi crude makes inroads with Chinese independent refiners

What’s happening? Saudi Arabia's crude oil exports to major Northeast Asian customers have suffered so far this year amid stiff competition from light sweet US crude cargoes flooding the Asian market and OPEC's ongoing production cut commitment. But Saudi Aramco maintained a solid market share in China during the first half of 2019, with demand from China's independent refining sector playing a crucial role. Aramco's recent shift in strategy to diversify its customers has paid off, as the supply increments to China in H1 were mostly attributed to new customers in the independent refining sector – Zhejiang Petrochemical Co. and Hengli Petrochemical (Dalian).

What’s next? Saudi Arabia will likely continue to compete against Russian barrels to protect its market share in China. China's state-run and independent sectors continue to favor Far East Russian ESPO blend crude for the grade's attractive price tag and close supply proximity.

6. EU CO2 prices soar on gas price, Germany’s threatened allowance cuts

What’s happening? EU carbon dioxide allowance prices hit an 11-year high July 10, driven by a combination of factors including fresh signs that Germany could cancel allowances linked to planned coal-fired power plant closures, and scope for more ambition at the wider EU level for stronger emissions reduction targets. Carbon prices appeared to react to fresh comments by Germany’s environment minister Svenja Schulze last week who said she supports cancelling EUAs linked to coal plant closures. Adding further support, the proposed new European Commission president Ursula von de Leyen pitched more aggressive EU decarbonization policies.

What’s next? Carbon market participants will be watching closely for signs the latest gains can hold. Any fall back in gas prices could remove a supportive element for carbon. However, supply side factors continue to look bullish, with the Market Stability Reserve set to remove 397 million mt from auction supply this year, and an estimated 375 million mt from 2020 supply.

Reporting by Paul Hickin, Stuart Elliott, Frank Watson, Ben Kilbey, Diana Kinch, Philip Vahn and J. Robinson. Edited by Emma Slawinski