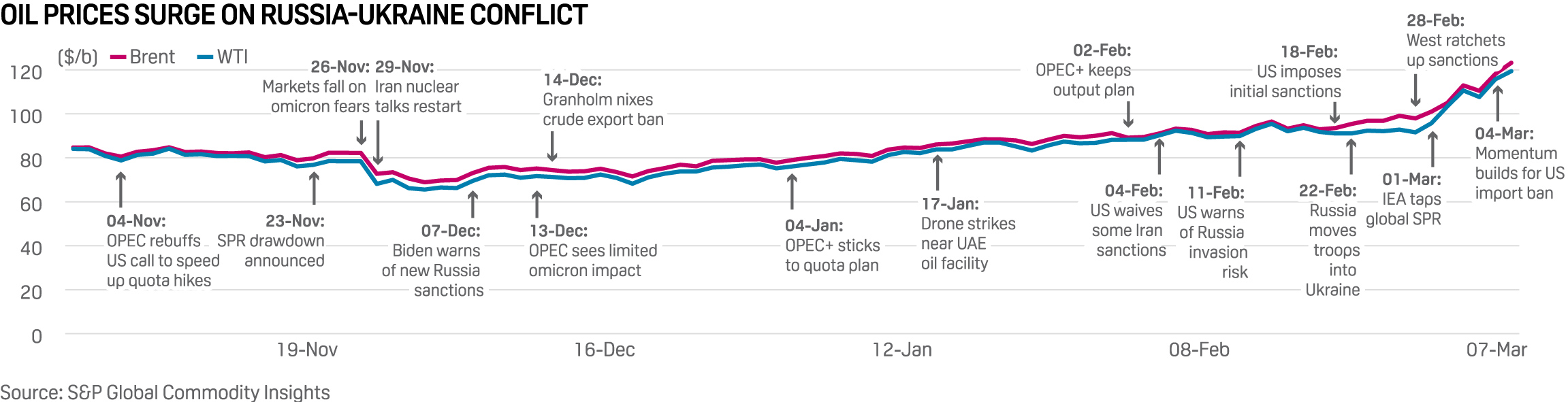

15 Mar 2022 | 06:03 UTC — Insight Blog

Fuel for Thought: US oil, gas industry not keen on playing ‘swing producer’ role, despite government pleas

By Gary Gentile and Starr Spencer

A popular saying comes to mind when considering the recent US government plea to boost domestic oil and gas production: What goes around comes around.

US officials have appealed to patriotism to persuade oil and gas producers to turn on the taps to ease consumer pain resulting from rising inflation and roller-coaster energy prices.

"We are on a war footing—an emergency—and we have to responsibly increase short-term supply where we can right now to stabilize the market and to minimize harm to American families," US Energy Secretary Jennifer Granholm told an industry crowd at the recent CERAWeek by S&P Global conference. "That means releases from strategic reserves across the world, like we've done. And that means you producing more right now, where and if you can."

While Granholm was playing "good cop" in Houston, White House Press Secretary Jen Psaki was taking the "bad cop" role from her perch in Washington.

In response to a Fox News reporter who asked during a daily press briefing why the US can't produce more oil instead of asking other countries to do so, as President Joe Biden has done, Psaki said domestic upstream operators have about 9,000 permits to drill wells that they could use if desired.

"The suggestion that we are not allowing anyone to drill is inaccurate," she said. "So, the suggestion that that is what is hindering or preventing [gasoline] prices to come down is inaccurate."

Granholm tried to thread the needle during her speech, claiming oil and gas producers could hit the gas pedal while simultaneously continuing their U-turn away from fossil fuels.

She emphasized US oil and gas producers can "walk and chew gum at the same time" and still focus on the energy transition.

She bemoaned "the same old DC BS," such as critics decrying canceled pipeline projects. She did not mention Keystone XL specifically, and she urged producers to partner with the administration.

Not so fast

Even if a concerted effort by domestic producers to ramp up oil output began at once, it would not immediately help because of the time lag factor, Nathan Hasbrook, analyst for supply and production for S&P Global Energy, and other analysts, say.

"It can take a fair amount of time to get permits approved, depending on who has to approve the permit," Hasbrook said. "Given a low cost to get permits, many operators will get permits for an abundance of wells."

Also, each geologic play or region has unique challenges with getting drill locations determined and permits approved, so companies try to have extra permitted well locations to provide flexibility, he said.

But a fair number of those "extra" permits are never drilled.

"They [are] for 'just in case'," he said, and if they aren't needed, operators will stick with their most-desirable well locations.

"The idea is that if there are delays with permitting or other land issues that the management team will have flexibility in deciding where they want to drill and not run short on options," he added.

E&Ps have restricted their capital budgets in recent years and given generous percentages of their cash flows to shareholders. They have become vastly more efficient and thus can hold production relatively flat or at low-growth levels while accomplishing their strategic goals.

And there appears to be no move to change that just yet, Evercore ISI analyst Stephen Richardson said.

"Our discussions with a number of the E&Ps suggested the price spikes and major policy shifts are not shifting corporate priorities just yet," Richardson said. "The recurring themes of our conversations was that US supply growth was already on a positive trajectory (rig count has doubled year on year) and 750,000 b/d to 1 million b/d of growth should be expected."

No turning back

During recent earnings calls, the CEOs of US oil and gas drillers said they were not inclined to return to the heady days of almost unlimited capex spending and production growth.

Pioneer CEO Scott Sheffield said barring a prolonged bloody Russia-Ukraine conflict, "none of us are going to jump out" on volunteering to suddenly jettison companies' carefully crafted goals of generally keeping yearly production growth to modest low-single-digit percent production growth. Pioneer's long-term growth projection is 5%, a figure also cited by many of its peers.

Shareholders and investors also look askance at instant or impulsive strategy shifts, Sheffield noted.

"Investor feedback ... [is] saying don't grow more than 5% regardless," he said.

While it may sound unpatriotic in the short term, company calculus has been based on years of frustration with political leaders and a pragmatic coming to terms with investor sentiment.

"This isn't something you can flip a switch and say, 'Okay, we're going to produce another million barrels of oil a day to get out there and drill those wells,'" Oklahoma City University professor and economist Dr. Steve Agee said in a recent article on the KFOR television website.

"If we get in there and drill new wells, spend a lot of new money, have to borrow that money in order to drill and complete those wells and then all of a sudden, six months from now, let's suppose this crisis is over and oil markets go back to normal. Then they could have spent a whole lot of money and the price of oil may drop back down to $70 a barrel."

With reporting from Jordan Blum