31 Jul 2018 | 21:30 UTC — Insight Blog

US utility coal stockpiles continue to decline; markets not alarmed

By Andrew Moore

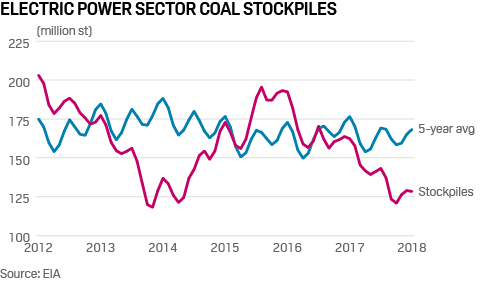

Utility coal stockpiles stood at 128.4 million st at the end of May, according to the most recent US Energy Information Administration data, released last week.

The figure was down 20.9% from the year-ago month, and down 23.7% from the five-year average for the month.

Stockpiles typically build during May, as utilities prepare for summer burn. The five-year average is a build of 3.1 million st; this year, it was a drawdown of 540,000 st.

According to Arlington, Virginia-based energy consultancy Energy Ventures Analysis, utility stockpiles at the end of June stood at 119.2 million st. The EVA total, based on survey responses and modeling, would be 24.4% off the EIA’s year-ago figure for June, and 26.5% below from the five-year average.

It would also be the lowest stockpile figure March 2014, which followed the so-called Polar Vortex of early 2014.

Yet coal prices have shown little reaction. The over-the-counter price for front-month Powder River Basin 8,800 Btu/lb coal was assessed Friday at $12.25/st, the lowest price this year. The price started the year at $12.40/st, peaked at $13/st February 23, then has largely declined in the following weeks.

In the East, the front-month price for Central Appalachia rail (CSX) coal, basis 12,500 Btu/lb, was assessed Friday at $64.75/st, nearly matching its year-to-date high of $65.05/st in early January, but market watchers peg the current rally to overseas prices rather than domestic demand.

“You don’t see people rushing out to buy coal,” said Seth Schwartz, EVA’s president.

Low burn

Part of the reason is due to low burn. Cheap natural gas and increasing wind generation have pushed down coal capacity factors, so days of burn — the amount of time to expend stockpiles at the current rate of consumption — remain relatively high.

According to EIA data released earlier this week, days of burn at bituminous coal plants as of May 31 stood at 75 days, up 2.5% from the five-year average for the month, while days of burn at subbituminous coal plants stood at 78 days, up 14%.

EVA reported days of burn for all plants at the end of June stood at 68 days.

Given utilities typically target a stockpile of roughly 50-60 days, inventories have yet to be a point of concern.

“We haven’t seen any issues yet, and I don’t really anticipate any issues given where we project stockpiles are going,” said Joe Aldina with S&P Global Platts Analytics.

Platts Analytics forecasts national days of burn to end July at 59 days, and average 65 days between August and January 2019.

'Stockpile managers'

Other reasons stockpiles continue to decline is uncertain demand, as well as a reluctance to become “stockpile managers.”

“It costs a lot of money to keep coal on the ground, and it’s happened three times in the last decade,” said Schwartz, pointing to the recession (2008-2009), the year without a winter (2012) and the mild winter/historic low natural gas prices in 2016.

“Utilities generally have pulled back in terms of how much they are committing under contract, because they’ve found burn is not as predictable as it used to be,” said Schwartz. “When running as baseload you know what you were go to burn three years out, but now you’ve had several events where you’ve been over-contracted, and that’s not something anyone wants to do.”

Using EIA data going back to 2004, utility stockpiles bottomed at 97.5 million st in January 2005. Should stockpiles drop below those levels, “people would start to scream,” said Schwartz.

As August nears, the domestic coal market is hardly screaming, save for higher gas.