19 May 2016 | 05:31 UTC — Insight Blog

Asia's polymer producers add value for higher margins

Polymer producers in Asia, most of whom are integrated to naphtha, have been in a celebratory mood in recent months. The plunge in oil and naphtha prices has resulted in a significant reduction in their feedstock costs and caused their margins to improve beyond their wildest dreams. Margins for polyethylene over naphtha are around $300/metric ton currently, while those for polypropylene are at $150/mt, a direct result of the 58% plunge in oil prices since June 2014.

However, some of the more prescient producers realize that there are plenty of headwinds ahead, which may cause the happy situation to reverse, and are already pursuing strategies which will help them keep afloat should that happen.

One of the key strategies in these producers’ survival kit is value addition. This assumes added importance as China, the largest polymer guzzler in the world, marches towards self-sufficiency in commodity polymers. China’s imports of polyethylene and polypropylene have been steadily falling, thanks to the increase in local coal-based production, which has been focusing on commodity grades. PE imports into China have fallen 3% year on year in the first quarter of 2016 to 2.4 million mt. PP imports are down 23% in the same period to 1 million mt, according to China Customs.

This is in line with the priorities outlined by the Chinese government in the 13th Five Year Plan which was launched this year. The government is quite clear about encouraging local production and building feedstock security by tapping into its immense coal resources. Imports will therefore be increasingly confined to value-added grades which China does not produce in adequate volumes. Hence the shift of focus by polymer exporters to China to high-end grades such as metallocene linear low PE and copolymer PP.

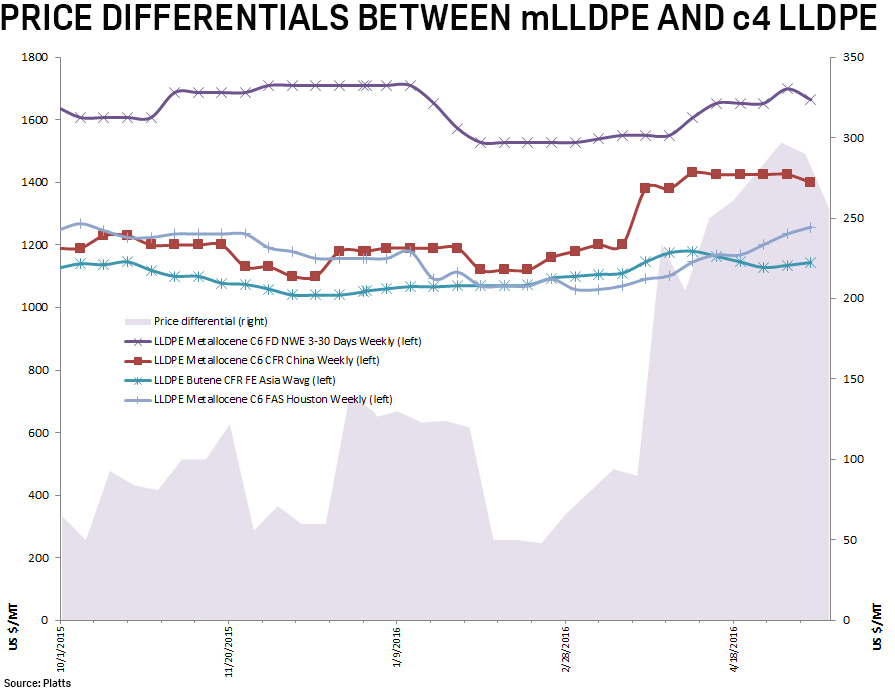

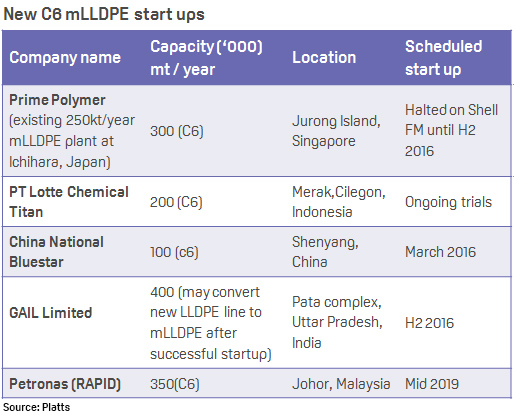

China only started up its first mLLDPE plant in March 2016 — China National Bluestar’s 100,000 mt/year plant in Shenyang. However, this is far from sufficient to meet the country’s growing appetite for this grade. End-users are willing to pay a premium for this grade over the commoditized C4 grade LLDPE. As recently as May 11, 2016, the premium of C6 mLLDPE over the commodity C4 grade imported into China was as high as $256/mt, according to Platts data. This is a huge increase from the low of $50/mt seen in October 2015, highlighting the increasing preference in China for this high-end grade in flexible packaging applications, thanks to its superior tear resistance, down-gauging and hot-stamping (high-speed printing).

In a bid to capitalize on this opportunity to improve their margins, two more mLLDPE plants are set to go onstream in Asia in the second half of 2016 – PT Lotte Titan Chemical’s 200,000 mt/year plant in Merak, Indonesia and Gail India’s 400,000 mt/year unit in Pata, Uttar Pradesh. Prime Evolue, a joint venture between Japan’s Prime Polymer and Mitsui Chemicals, started up a new 300,000 metallocene polyethylene plant on Singapore’s Jurong Island in 2015, but this is currently shut because of a force majeure at Shell Chemical’s complex located in Singapore.

"Metallocene is probably one of the best [in demand] growth in the PE portfolio; that's why we are supporting our customers by investing in our Nexlene technology in [South] Korea and introducing it to our customers in China," Sabic’s Executive Vice President of Polymers Abdulrahman Al-Fageeh told Platts PP editor Yi-Jeng Huang on the sidelines of the Chinaplas exhibition in Shanghai in late April 2016.

Incentivized by the prospect of garnering better margins, China-based traders told Platts senior editor for PE Heng Hui at the same ChinaPlas event that they are also changing the way they do business, opting more and more for specialized polymer grades.

A similar trend can be witnessed in PP, where producers are diversifying increasingly into higher-end grades. For instance, IRPC of Thailand is looking into producing high rubber PP for the automotive sector using Japan’s JPP technology at their plant in Rayong. The unit is expected to be up and running by end-2017. Another Middle East producer, Borouge, has begun producing PP composite reinforced with carbon fiber for automotive applications. NatPet is also exploring new technology options for its compounding joint venture with Schulman at Yanbu, Saudi Arabia, aimed mainly at the automotive sector.

In short, it’s a win-win situation for both — producers looking to lock in their margins in a volatile market, and customers aspiring to improve their lifestyle options.

Hear Platts editors and analysts present on these and other emerging trends in petrochemicals at the Asia Petrochemical Industry Conference (APIC) being held in Singapore on May 19-20, 2016.