19 Aug 2020 | 15:13 UTC — Insight Blog

New waves in freight, part II: shifting oil product flows call for new UKC-WAF tanker benchmark

By Chris To

In the second of a two-part series on evolving tanker markets either side of the Atlantic, Chris To makes the case for a different approach to valuing an emerging route that is being fuelled by rising refined product imports to Africa.

In the global trade of refined oil products, the transatlantic route travelled by gasoline cargoes from Europe to the US has for decades been the bellwether for the west of Suez clean tanker market.

The most traded clean tanker trading route west of Suez, the UK/Continent -US Atlantic Coast benchmark for 37,000 mt Medium Range tankers remains the most prominent, but the rise in shipments to another key basin – in West Africa – is now laying a claim that the derivatives market for MRs needs to evolve and produce an alternative.

As a prospective hedging tool to both explore and exploit, the time has now come for a UKC-WAF 37kt benchmark to take shape in clean tankers.

Another option for MR owners

When looking at a transatlantic cargo to fix, MR owners typically factor round trip economics into their decision by analyzing their prospects on the backhaul market – which is a US Gulf Coast – UKC shipment for MRs. If the intention of the shipowner is to reposition in the continent, this dynamic, and its earning potential, is known in the market as the transatlantic triangulation.

The most liquid benchmarks on the MR west of Suez market therefore manifest as these transatlantic contracts – a front haul derivatives number for UKC-USAC, and a backhaul for USG-UKC.

Go deeper: New waves in freight, part I: USGC-Brazil emerges as barometer for tanker market

But shouldn’t the market have the option to hedge on positions taken when they decide to embark on this triangulation? This is where a WAF benchmark comes in – giving the market a chance to take a position for the long journey down south against the transatlantic voyage.

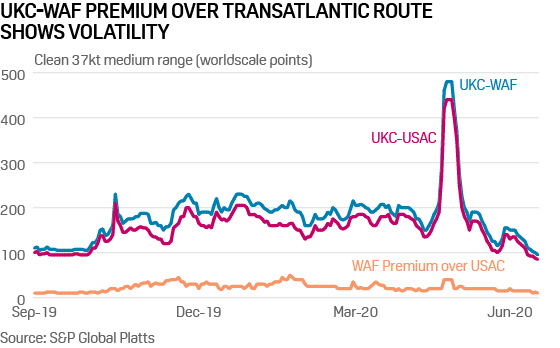

What most of the market will say is that the WAF market is commonly and easily identified as a Worldscale premium against transatlantic runs. This is true – it is fairly easy to determine WAF market rates if USAC runs are also known.

But the premium is subject to change, and sometimes quite volatile, showing that the WAF market warrants a life of its own on the derivatives stage.

Throughout the fourth quarter 2019 and early in Q1 2020, WAF premiums against UKC-USAC rates rose as high as 50 Worldscale points – a change that pushed some market participants to state that MR markets were at times “WAF driven”.

A typical scenario is when the transatlantic triangulation grows strong on temporary bursts of tightness amid high cargo availability. This is particularly frequent in the USG.

Shipowners act swiftly to lock in a healthy number for transatlantic shipments for both front haul and back haul, processing strong earnings as a result. As a result, shipowners typically would be able to command a higher premium for any prospective WAF shipment, knowing they’re taking their vessel out of the market for a number of weeks.

The life-force of the WAF market soon emerges as rates show differing correlations in moving markets.

With a derivatives number to trade forwards contracts on, market participants can act and take a position. Its primary purpose would then be as a tool to hedge against the idiosyncratic uncertainties of transatlantic trips, such as a sudden lack of cargo availability for back haul contributing to overall poorer round trip economics. This possibility presents itself as the main driver of interest in this benchmark.

The trading route has demonstrated reliable liquidity, and there is every reason to believe this will continue, providing an incentive to look deeper.

Emergence of WAF

The rise of shipments of gasoline to West Africa in the last few years now entrenches this market as a primary alternative for MR owners who look for options when they open in the continent. Growing interest of cargoes to the region has drawn most if not all major names among oil traders to invest there, and shipowners have followed suit to pursue further business.

The WAF gasoline market is not going away any time soon. With market economies projected to grow, once the impact of the coronavirus pandemic eases, gasoline imports are expected to continue jumping.

The chart below provides an illustration of oil product import growth into WAF combined over the past years. Growing economies in the West Africa region continue to drive up demand for gasoline, which cannot be met by local refineries. In the region, refinery facilities do not have sufficient fluid catalytic cracking units (FCCs) to allow efficient conversion into gasoline products – they simply aren’t equipped to satisfy local consumption.

The wider implication is that the heavy reliance on gasoline imports into the region will continue for years, with the UK Continent likely to remain the primary supplier.

But what about the existing transatlantic trade flow for gasoline from UKC-USAC – what volumes will we be seeing on this route in the years to come?

Here there is little agreement. Some claim that the development of sweet crude capacity in the US will in the longer term make the country self-sufficient in gasoline supply, while others expect the trade flow to have more longevity.

But universally, there is recognition that volumes are likely to stay steady, while incremental rises in WAF appetite could shift tanker focus to the opportunities on display in the south.

Paradigm Shift

Ultimately, a WAF benchmark would not only provide a hedging tool for the market to explore, but would open the door for an extra stream of revenue and income.

Paper trading for MRs west of Suez has rightly been focused on the transatlantic triangulation, but with shifting trading dynamics to come, the case for a new paper market vehicle will continue to strength.

With major oil traders continuing to invest in West Africa, the potential can no longer be ignored.