18 Apr 2017 | 05:31 UTC — Insight Blog

Container Index Revolution: Should it be embraced by carriers?

It is a fact that the wind of change does not smell the same to everyone. There are clear signs that the container industry is slowly creaking towards using price indexes in contracts, but some of the most important players still hesitate to give it a shot.

Liner carriers so far have been quite skeptical about shaking up the status quo in container pricing. The extra transparency that indexes may bring is often seen as a complication. But is that really so?

In reality, both carriers and end-users could benefit from more clarity and commitment when it comes down to negotiating contracts. The harsh truth is that container lines are caught between a rock and a hard place.

On one side, they have rising expenses that have to be covered. At the same time they have customers who are not thrilled when they get charged more through an often murky pricing mechanism.

Please take part in our Container Freight Markets Survey

When carriers increase their prices in line with their "General Rate Increase and Freight All Kind" notifications, they may well have a chance to meet their operating margins, but at the same time they could potentially lose market share if a competitor manages to throw in a cheaper quote. It is a price arm-wrestling match where no one really wins.

So it is understandable, when the global supply chain is anxious about carriers' survival, that the industry continues to see a stream of articles about who is most likely to go bankrupt next. It sells newspapers.

There needs a change from this pessimistic view to a greater focus on positive industry collaboration, on which subject a lot of constructive discussion was heard at the TPM 2017 conference in Long Beach, California in February.

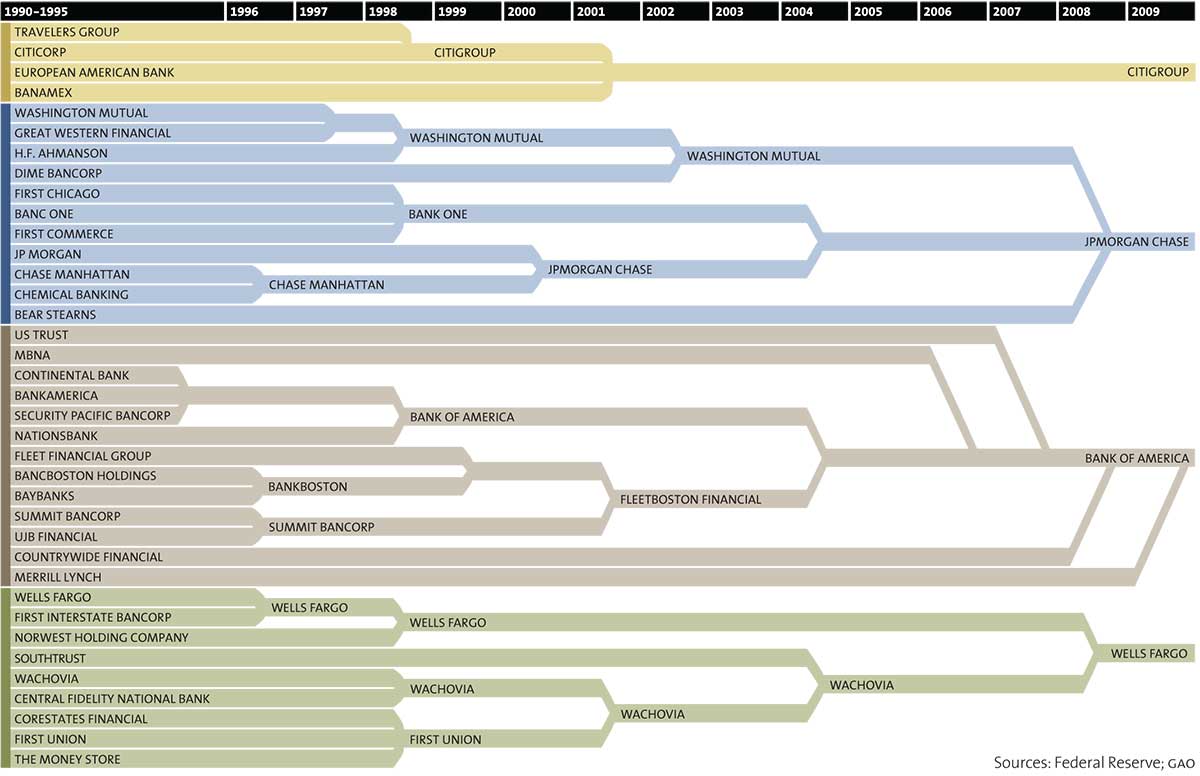

Today's carriers have shown a similar resilience and shape to the American banking industry, shown below. Carriers have survived the market conditions thrown at them through focused implementation of consolidation in two forms: strategic or opportunistic mergers and acquisitions, and operational alliances.

The major end-user and logistics companies really now have three alliances -- 2M, Ocean and THE -- to turn to for delivery of their logistics strategies.

Financial institutions (Sources: Federal Reserve; GAO)

The container industry needs these liners more than ever and should shift focus on to sustainable operating margins, in particular for carriers.

This would allow them to deliver a tailored customer service, building long-term relationships to deliver industry players' unique requirements.

Concentrating on quality and sustainability of service rather than pricing may be a long-term win.

Hapag-Lloyd CEO Rolf Habben Jansen has a profound point of view: "Don't focus on the price, the price will be what it will be."

The pioneering and disruptive FinTech companies entering the container market are providing new pricing mechanisms that could aid carriers' margins along with byproducts that could help resolve other inherent inefficiencies in freight negotiations, for example booking performance.

Habben Jansen said: "Carriers often provided a price and space on their vessels with around 25% fallout rate of shippers not turning up for their bookings."

The reason for such booking failures is simple. There is not enough skin in the game from either party. Shippers are not committed and can easily walk away if the price is no longer right.

Carriers can play this game too through void sailing programs that have implications on the logistics and end-users' supply chains.

One remedy is to bring in penalties to both parties if they renege on their commitment.

New York Shipping Exchange (NYSHEX)[1] has built a platform that brings the industry together digitally and could improve booking performance as there are penalties for both parties if they don't meet their commitment.

Carriers could also reduce their spot market freight negotiation process inefficiencies significantly if they collaboratively embraced this type of concept.

Dynamic pricing brings speed to the market than now, where it can take 30 days to change the rate up or down.

Alongside this it brings certainty on forward freight prices. Carriers place their offer price and if end-users are willing to pay, they accept the offer. It is not an auction tool, though.

However, even with platforms like these, the container industry is still lacking an index provider that is truly independent, regulated or accurate. Why are we not learning lessons from other sectors? Why not adapt the best practices from our closest sector, drybulk?

You have leading exchange groups that would be keen to enter the container Forward Freight Agreements (FFA) market but as Seaintellingence Consulting's Lars Jensen commented in response to Platts’ previous price transparency blog, "I am especially thinking about the carriers' extreme reluctance to allow external stakeholders to take paper positions in the industry, which was one of the major reasons why the freight rate derivatives launched in 2010 didn't make a strong breakthrough."

To achieve this potential representative market rate you need a transparent index that forms part of a holistic price discovery process for all industry players. Someone like Platts can do that.

Will the carriers buy into these types of pricing strategy? They probably should.

The endgame could be a better deal for them if they utilize an index provider because they are not only able to close that gap on freight expectations for contract negotiations but also mitigate shipping price risk.

This will not happen overnight but through consultation and collaboration. It also removes scrutiny from regulatory bodies as the process is fully transparent and cannot be perceived to be influenced.

[1] "Carriers provide shippers, NVOs and forwarders with a range of offers clearly displaying the relevant details of their service like space availability, prices and on-time performance. Shippers, NVOs, and forwarders can immediately accept a carrier's offer on NYSHEX and enter a binding contract."