10 Apr 2019 | 17:27 UTC — Insight Blog

Insight from Shanghai: China's shift in language signals private sector in the ascendant

In March, China’s elite gathered in Beijing for the annual “two sessions” meeting of China’s legislative bodies, the National People’s Congress (NPC) and the People’s Political Consultative Conference.

While much of what happens at the two sessions is at best marginalia for all but the most dedicated of China watchers, the key themes of the meeting and the government Work Report that outlines policy, priorities and targets for the coming the year, are worthy of attention.

As expected, the overall direction follows the 13th Five Year Plan released back in 2016: coordinated “innovation-driven development”, environmental protection and plenty more “opening up”. But as always with Chinese policy documents, the devil is in the detail.

Slower growth over more debt

That economic growth will continue to slow is hardly a surprise. But this year’s target of 6 - 6.5% offers more leeway than last year’s target of around "6.5%". This is recognition of the uncertainties facing the economy in 2019, from domestic risks in the financial sector and excessive local government debt to uncertainty around the global outlook and trade tensions with the US. The government does not want short-term growth if that means a buildup of debt that could pose a risk to long term financial stability. Those hoping for a cheap hit of stimulus to boost demand for everything from steel to diesel should growth start sagging will likely be disappointed in 2019.

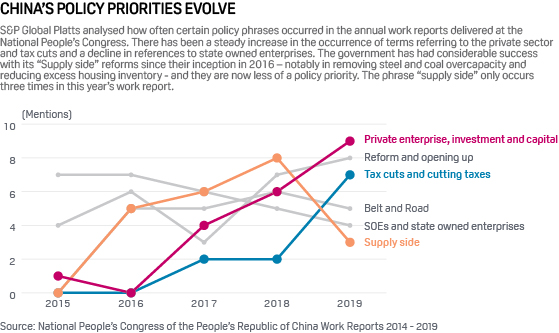

Tax cuts

The focus has moved instead to supporting growth and employment by reducing costs for manufacturers and small businesses. VAT has been cut across a range of sectors and the amount of social insurance that companies need to pay to employ workers has been reduced. The China Iron and Steel Association (CISA) estimates that the VAT cut will reduce the tax liability of CISA member mills by around Yuan 22 billion ($3 billion). But the main effect will be felt by consumers with lower prices supporting domestic consumption – albeit at a cost. The tax cuts will put pressure on government budgets at all levels. Local governments will be able to access special bonds to help balance their books, but overall, governments will have to tighten their belts in 2019 by reducing spending or finding new ways of raising money.

A greater role for the private sector

There has always been tension at the heart of the Chinese economic model between the role of government and the private sector in the economy. This year the private sector appears to be in the ascendant with no less than nine mentions of private enterprise, investment and capital in the government Work Report, up 50% on last year. This should mean a more favorable environment for private business and startups as well as increased lending to small and private businesses, which have historically found it hard to obtain finance.

Markets and reform of SOEs

At the same time, the government will continue to reform the SOEs. This won’t necessarily mean rolling back the state. But it should lead to a better managed, more profitable state sector with fewer unprofitable companies that are a drag on the economy and a drain on government budgets.

Market reforms will continue in the energy sector with further development of electricity spot markets building on the pilot power trading schemes already underway in some regions. Creating more competitive electricity markets will help address the problem of idle renewable capacity as well as reduce the role of coal. Ultimately, it could help lower the cost of electricity for industry.

Where power leads, so oil and gas will follow. The government has experimented with setting up gas pricing hubs, but the dominance of the “three barrels of oil”, as Chinese the oil and gas majors are often called, has impeded the development of competitive markets. In order to lay the groundwork for these the government will create a new national oil and gas pipeline company from the transmission assets currently in the hands of the integrated SOEs. Separating distribution from sales of oil and gas is just the first step in allowing oil and gas markets to develop in China. The government also envisages opening up upstream oil and gas exploration to non-state capital. But without further detail, it’s hard to judge how transformative introducing more competition into the upstream sector might be.

There is no letup in the battle against pollution as we move into the second year of the “three critical battles” (the others are guarding against financial risk and poverty alleviation). Structural adjustments and “supply side reform” will also continue, but the language is around strengthening and upgrading industry rather than removing overcapacity. Expect emissions reductions by upgrading steel plants and promoting the use of cleaner coal, rather than another round of coal and steel capacity cuts. Meanwhile, increasing utilization of solar, wind and hydro capacity and increasing the use cleaner fuels in heating in northern China will constrain the growth of coal.

If the government Work Report is anything to go by we may have reached peak “Belt and Road”. The term is referenced just five times throughout the report, down from six mentions last year. Instead the talk is of defending economic globalization, free trade, and win-win development.