01 Mar 2022 | 20:23 UTC

Oil futures: Crude, fuel prices surge as Ukraine conflict pushes NYMEX WTI well past $100/b

By Jordan Blum

Highlights

Russian barrels considered more toxic

Russian gasoil supplies drive up ULSD

IEA to release 60 mil barrels, 30 mil from the US

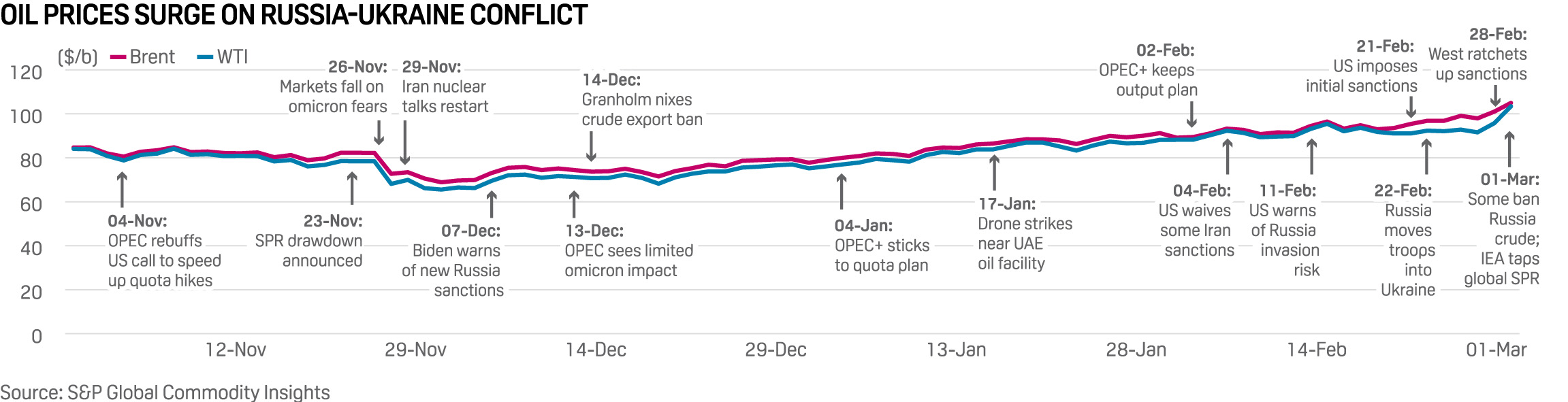

Crude oil and refined products prices skyrocketed March 1 as front-month NYMEX WTI surged way past the $100/b threshold, with Russia oil barrels increasingly considered toxic amid the country's military invasion of Ukraine.

NYMEX April WTI shot up $7.69 to settle at $103.41/b -- after trading as high as $106.78/b during the day -- moving to the highest pricing levels since July 2014. ICE May Brent jumped $7 to settle at $104.97/b. Prices pared a bit after the International Energy Agency announced a global coordinated release of crude reserves.

The super-backwardation pricing environment, for instance, shows NYMEX December WTI settled at $83.68 -- nearly $20/b cheaper than front-month pricing.

NYMEX April RBOB was 15.62 cents higher at $3.0877/gal and NYMEX April ULSD added 21.98 cents to $3.1511/gal.

The situation remains highly unpredictable and prices could continue rising, according to S&P Global Commodity Insights' Shin Kim, head of oil supply and production analysis. And all of this was occurring March 1 as Russia escalated its attacks on Kyiv and Kharkiv.

"Oil price differentials are reflecting a clear unwillingness to take Russian crude, and there continues to be [a] risk of more sanctions that could indirectly or directly impact oil purchases or supplies," Kim said.

In the case of a major loss of Russian supply, the combination of US and IEA strategic reserve releases and higher Saudi Arabian and UAE crude production could at most make up for 2 million-3 million b/d over the next couple of months, Kim said. That number quickly falls to just 1 million-1.5 million b/d in the third month, although the assumed full return of the Iran nuclear deal could add another 1 million b/d of supply by August.

However, this does not nearly make up for total Russian oil exports of around 7 million b/d, of which 4.5 million b/d is crude.

"Bottom line, these potential sources of incremental supply in coming months are not enough [to] offset a prolonged substantial loss of Russian oil," Kim said.

More countries are beginning to ban Russian oil imports. Canada was the first to implement a ban, and the UK agreed to bar Russian oil tankers from its ports. Sweden also said it ceased importing Russian crude. In the US, Senator Joe Manchin, a West Virginia Democrat, and others called on President Joe Biden to ban Russian crude.

The IEA said March 1 it would release 60 million barrels of oil in a coordinated response effort, including 30 million barrels from the US Strategic Petroleum Reserve. The IEA said an "initial" release of 60 million barrels is equivalent to 2 million b/d for 30 days or 4% of the IEA members' current oil stockpiles. The IEA also plans to release on March 3 a 10-point plan on how Europe can reduce its dependence on Russian gas in time for next winter.

"We are prepared to use every tool available to us to limit disruption to global energy supply as a result of President Putin's actions," White House Press Secretary Jen Psaki said in a statement. "We will also continue our efforts to accelerate diversification of energy supplies away from Russia and to secure the world from Moscow's weaponization of oil and gas."

Meanwhile, OPEC+ has revised down its forecast for the 2022 oil market surplus by about 200,000 b/d to just 1.1 million b/d. The OPEC+ group meets March 2, but thus far has refused to expedite the unwinding of its production quotas and, in fact, continues to underperform against those quotas.

Sanctions, cutbacks

If sanctions against Russia do hit oil and gas harder, then Brent crude could easily move toward $120/b, said Edward Moya, senior market analyst for OANDA.

"If this trajectory in oil prices continues, economic growth prospects will take a big hit and that could lead to a significant deterioration with the medium-term crude demand outlook," Moya said.

Over the weekend, the US, the EU and Japan surprised the markets by dramatically increasing sanctions against Russia, targeting its Central Bank, and planning to kick many Russian banks out of the SWIFT financial messaging system. Even if oil and gas are excluded from the sanctions, the SWIFT moves still would affect crude barrels to some extent.

"Cutting Russian bank access to SWIFT is another way of cutting Russian exports of crude oil," said Robert Yawger, director of energy futures at Mizuho Securities, in a Feb. 28 note. "Buyers shy away from the grade because of the sanctions threat and fear they will have to scramble to pay for barrels if they are locked out of the SWIFT system."

The sanctions also pose a risk to Russian gasoil exports, which helped drive gasoil and ULSD prices higher. Distillate inventories are tight. In the US, for instance, stocks at 119.7 million barrels the week ended Feb. 18 were roughly 18% below the five-year average, US Energy Information Administration data showed. Russia exports about 2 million mt/d of ULSD to Europe.

Russia's medium sour Urals crude is taking on huge discounts, with markets hesitant to take on the barrels -- even though the sanctions have energy carve-outs for now.

Also, two of the world's biggest container shipping companies, Maersk and the Mediterranean Shipping Co., said they are halting most cargo bookings to and from Russia.

This comes after BP and Shell said they would divest their Russian energy holdings. TotalEnergies said March 1 it would stop new spending on Russian projects, but the French energy company stopped short of divesting its current stakes.

Rystad Energy said the Ukrainian conflict also will make oil and gas drilling more expensive because of potential shortages of oil country tubular goods steel and piping for wells. Both Russia and Ukraine are globally significant OCTG producers with supplies particularly important for the Middle East and US markets, Rystad noted.