03 Apr 2017 | 13:30 UTC — Insight Blog

Bunker industry headwinds continue ahead of 2020

By Jack Jordan

With the first quarter of 2017 over, the slew of problems facing the bunker industry shows no sign of diminishing. Consolidation among both shipowners and fuel suppliers, tightening credit conditions and shifting demand are all adding to the threat posed by tougher environmental regulations due to be introduced in the years ahead.

More emissions regulation to follow IMO sulfur cap

The biggest shock for the industry to absorb is the decision by the International Maritime Organization in October to cut the global marine fuel sulfur content limit to 0.5% from the start of 2020 from 3.5%. While the decision itself was not a surprise to most, the problem is the lack of clarity about what happens next.

The lower sulfur limit will force shipowners to fit emissions-cleaning scrubbers to their vessels, to ignore the regulations entirely or -- likely the most popular option at first -- to switch to burning a fuel with a lower sulfur content.

But the availability of these fuels remains in question. Europe's net shortage of middle distillates will mean many ports there will struggle to find enough product to accommodate demand from shipowners shifting away from using fuel oil, and the resulting higher prices may cause some buyers to refuel more often in Middle Eastern and Asian ports instead.

If shipowners do rush to fit scrubbers in the next few years to carry on using fuel oil, there's no guarantee about how much of that product will be available for them either. Refineries across the world have been pushing on with upgrades since the IMO decision to try to minimize their fuel oil production.

Adding to uncertainty on these issues is the likelihood of further emissions regulation down the line. The industry is already resigned to new limits on nitrogen and particulate matter emissions before long, and now it seems likely carbon emissions will be regulated too.

The European Parliament wants to include shipping in its emissions trading scheme and plans to push for this in its negotiations with EU national governments on reforms to the scheme after 2020. If the IMO does not have a comparable system operating by 2021, the European Parliament wants to include shipping in the scheme from 2023 onwards.

Uncertainty follows Hanjin collapse

A more unexpected setback hit the bunker industry late last year with the bankruptcy of South Korean container line Hanjin Shipping, adding to jitters about the creditworthiness of shipowners. Banks are increasingly reviewing their exposure to the shipping industry, leaving them less willing to back bunker traders extending generous credit lines to the industry.

Hanjin's collapse also underlined the trend of consolidation within shipping, particularly in the container and dry bulk segments. As the bunker industry's bigger buyers consolidate, their buying strategies are likely to become more sophisticated and marine fuel trading margins will come under further pressure.

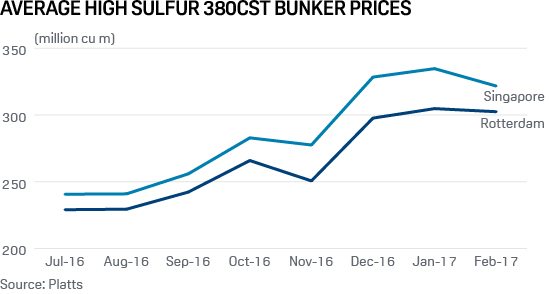

In Singapore, trading margins for some traders have fallen from $1-$2/mt to as little as 50-60 cents/mt as capital and financing costs increased.

The bunker industry itself is also still in consolidation, riding the wave that started in 2014 when the crude price collapse led to the bankruptcy of OW Bunker. Global supplier Bomin warned of a "new era for bunkering" last year and announced office closures in Rio de Janeiro, Tallinn, Madrid, London and Athens.

That 'new era' so far has been a mixed bag -- sales in Singapore continue to smash through record highs, while at Rotterdam bunker consumption hit its lowest in at least a decade last year. But the industry looks likely to face further troubles for a while yet until more companies shrink their operations, the outlook for shipping becomes healthier and the regulatory environment clearer.