19 Jun 2019 | 16:44 UTC — Insight Blog

Insight Conversation: Mark Gyetvay, Novatek

By Lucie Roux

Mark Gyetvay, CFO and deputy chairman of the management board at Novatek, visited S&P Global Platts for an interview with senior writer for LNG, Lucie Roux. Novatek is a Russian independent gas producer known for its Yamal LNG terminal, launched in 2017, and now for its Arctic LNG projects.

Last may at the Flame conference you said Novatek aims to increase production to 70 million metric tons/ year by 2030. Where is the market going to be for those volumes? Are you still seeing Asia as your main market?

Yes, the plan is to increase shipments to the Asian pacific market. That essentially gives us the opportunity, given the demand growth we see in in Asia, to increase our output from roughly about 57 million mt/year to approximately 70 million mt/year by the year 2030.

Are the current low LNG price and low JKM-TTF spread causing issues for your existing buyers?

Not necessarily. I would say that if we look at pricing today, it actually benefits companies like Novatek who are a low cost producer. What we see in a low price environment is actually an opportunity to increase demand in certain geographical regions that are extremely price sensitive.

For example, one of the areas where we hope to see substantial growth in the next decade, through the transition of coal to natural gas, is India. India is highly sensitive to the gas price.

So it really doesn’t create a huge problem today, but obviously if you’re making a financial investment decision in a particular project, your price is going to be a concern today.

Go deeper: Listen to the full interview with Mark Gyatvay

Last winter almost all your cargoes went to Europe and some reports are pointing to an overlap of LNG with natural gas, or to put it another way, they point to competition between Gazprom and Novatek, do you agree with that?

I agree with the first part of your statement that a significant portion of our LNG over the winter months went to Europe. That was largely due to the fact that with our early start of volumes, our sales were essentially spot sales. Once we rolled into the long-term contracts, they’re basically geared more to the Asian Pacific market.

And I don’t look at [it as] a direct competition to Gazprom. Some of our volumes actually went to delivery points that are not part of the pipeline structure. For example, we sold a cargo to Spain, to Gas Natural. Gazprom does not deliver natural gas to that particular market, and we sold the first cargo of Russian gas to Spain.

So I wouldn’t say it’s a direct competition, but obviously as the volumes increase we’ll have some overlap.

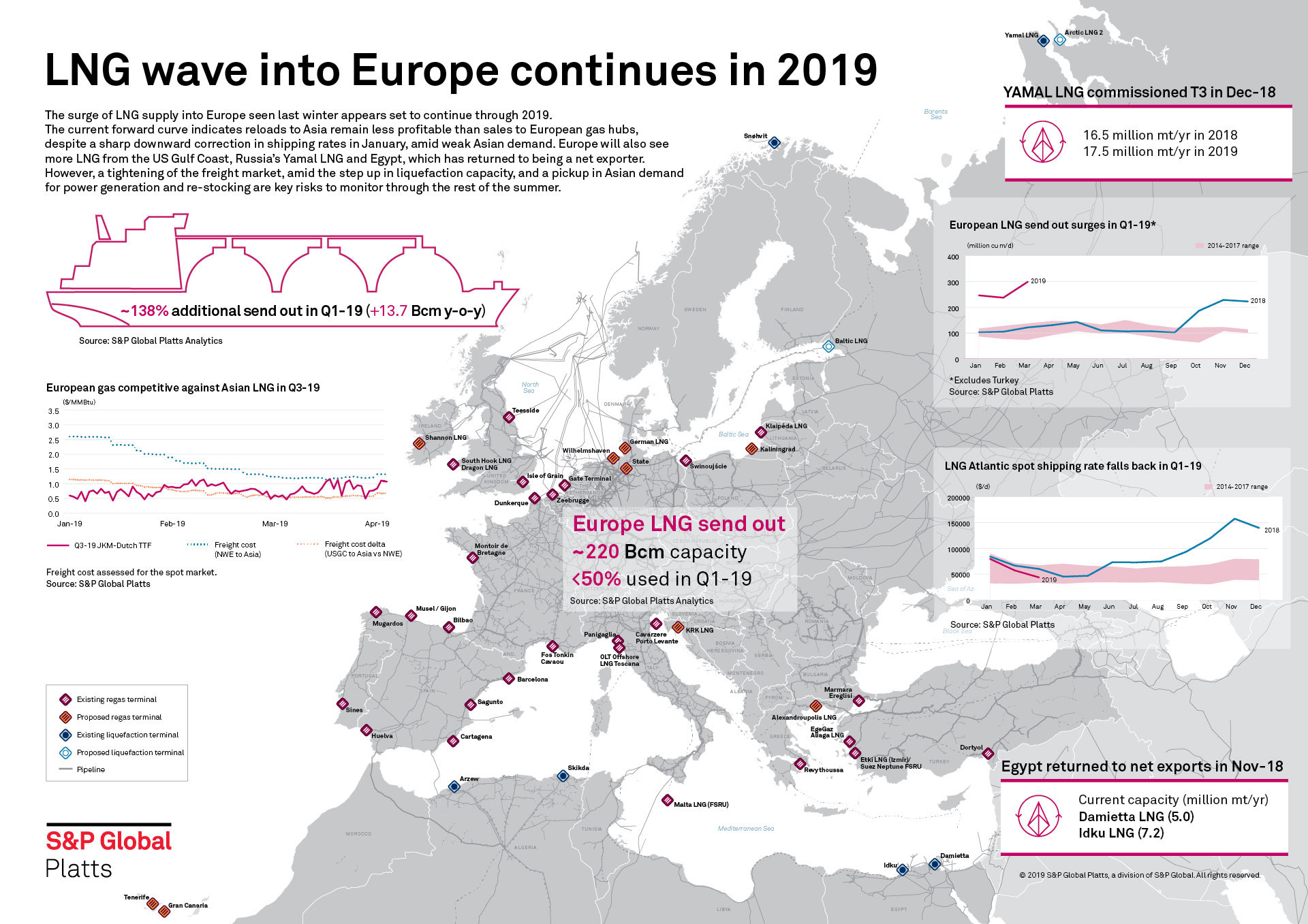

Click for full-size infographic

Looking more specifically at the Arctic LNG 2, what do you expect the volume of spot versus contracted sales to be?

We initially estimated a 50/50 split: 50% long-term contracts, 50% spot. And I think that is where we are headed to right now when we look at the primary sales and the markets we are talking to. But it doesn’t preclude us, if somebody wants a higher proportion to the long-term contracts, we’ll be willing to do more long term than spot. A lot also depends on the evolution of the market itself. As we see an increase of liquidity in the LNG market, we’re expecting more and more volumes will be sold on a spot basis.

So if more is sold on a spot basis, how will price and volume risks be managed for spot LNG?

Again, that is another area that is evolving. When we look at the current LNG trade, we’ are seeing the traditional linkage to oil declining, and more of a hybrid index price in particular regions where we’re selling. So I think in terms of longer-term spot I think we will see that evolution towards a hybrid local-based pricing. We might even just see more regional pricing rather than global markers, such as Platts JKM emerging, TTF in Europe.

I think we are seeing now people are moving away from the Henry Hub-based linkage, but there will still be partly oil linkage, partly gas hub linkage, and probably over the long-term more hybrid price products.

Turning to geopolitics, can we discuss how US government sanctions affect Novatek? How difficult it is to work under sanctions? Are there some limitations on trades, swaps, technology, in new investments, or other concerns?

We were actually quite surprised when Novatek was actually named as part of the sanctions. It’s a subset called the sectorial sanctions, which essentially limited Novatek’s ability to raise new US dollar denominated debts by US persons, greater than 90 days. That happened in July 2014. Subsequently they tightened a little bit making it 60 days. It really didn’t have a dramatic impact on technology, swaps, commercial operations, nor did it have any impact on existing shares and debt traded in the market place.

We had to rearrange the finance and structure, move away from US dollars. We moved away from the traditional project financing structures, and we received more financing directly from the Russian Federation, and Russian banks, as well as Chinese banks. So I don’t really see it as an impediment. But I think by and large, we’d really like to move the geopolitical question outside and focus on delivering natural gas. We just don’t see that sanctions play a role in an environment where the world needs affordable natural gas.

Everybody is watching the current trade tensions between the US and China. What does this trade issue mean for your business and do you see any opportunity for Novatek?

It has clearly impacted the delivery of US LNG into the Chinese market. I’ve read recently that in 2019 to date, only three cargoes of US LNG have actually landed inside of China. And cargoes that have already been contracted are now been swapped out outside of the Chinese market. Most of the US-based LNG projects, particularly what we call the second-wave projects, are particularly predicated on future growth demand in the Chinese market, and as a result what we’ve seen already, the immediate impact, is more shipments going into the European market, essentially flooding the European market with natural gas.

So I think long term, clearly it has a benefit to us if Chinese companies are refusing offtake of US LNG, but really I think the main question today is how long will this trade war be maintained. Is it a structural shift, short term, long term, medium term? I believe you can’t make a business decision on trade with so many uncertainties. However in the medium term, yes it does have a positive impact, because Chinese companies have now signed off on the Arctic 2 project.

To close on a lighter note, the US has decided to call its gas “freedom gas”. What is your reaction to that and can Russia also have a name for its gas?

Well if I remember properly, we’ve also changed French fries to “freedom fries”. And so now we have “freedom gas”. I think it’s the same question that you’ve asked earlier about the geopolitics. It’s best to leave politics out of the equation because our goal today is to deliver the most cost-competitive LNG into the market place.

What we’re trying to do is to transition the world from coal to natural gas, that’s what we need to do in terms of climate change initiative and so the politics of the world. I think if I was trying to look at a word that is opposite of freedom, I guess you can use “oppressive” gas? But that would be totally silly to make that point – from my perspective I think we just look at it as natural gas and focus on what we do best and that is delivering cost-competitive LNG to the market place.