14 Jun 2018 | 17:00 UTC — Insight Blog

Commoditization underpins LNG demand, supply and pricing innovations

By Marc Howson

LNG's increasing flexibilities are facilitated by increasingly transparent market-based pricing, soaring derivatives trade and new Asian hubs emerging. Last month, Cheniere successfully sanctioned its latest supply project by offering market-friendly flexibilities and cost competitiveness, additional drivers underpinning LNG's commoditization.

Certain buyers, sellers, traders and exchanges have therefore already benefited from the new LNG environment, and further opportunities exist. During S&P Global Platts' annual LNG and Natural Gas Markets Asia Conference, held May 31-June 1 in Singapore, market participants demonstrated many innovative approaches for grasping the opportunities offered by LNG's increasing commoditization.

Related blog post:

China hits back at Trump, but LNG stays untouched

1. Emerging Asian hubs providing further LNG demand and liquidity

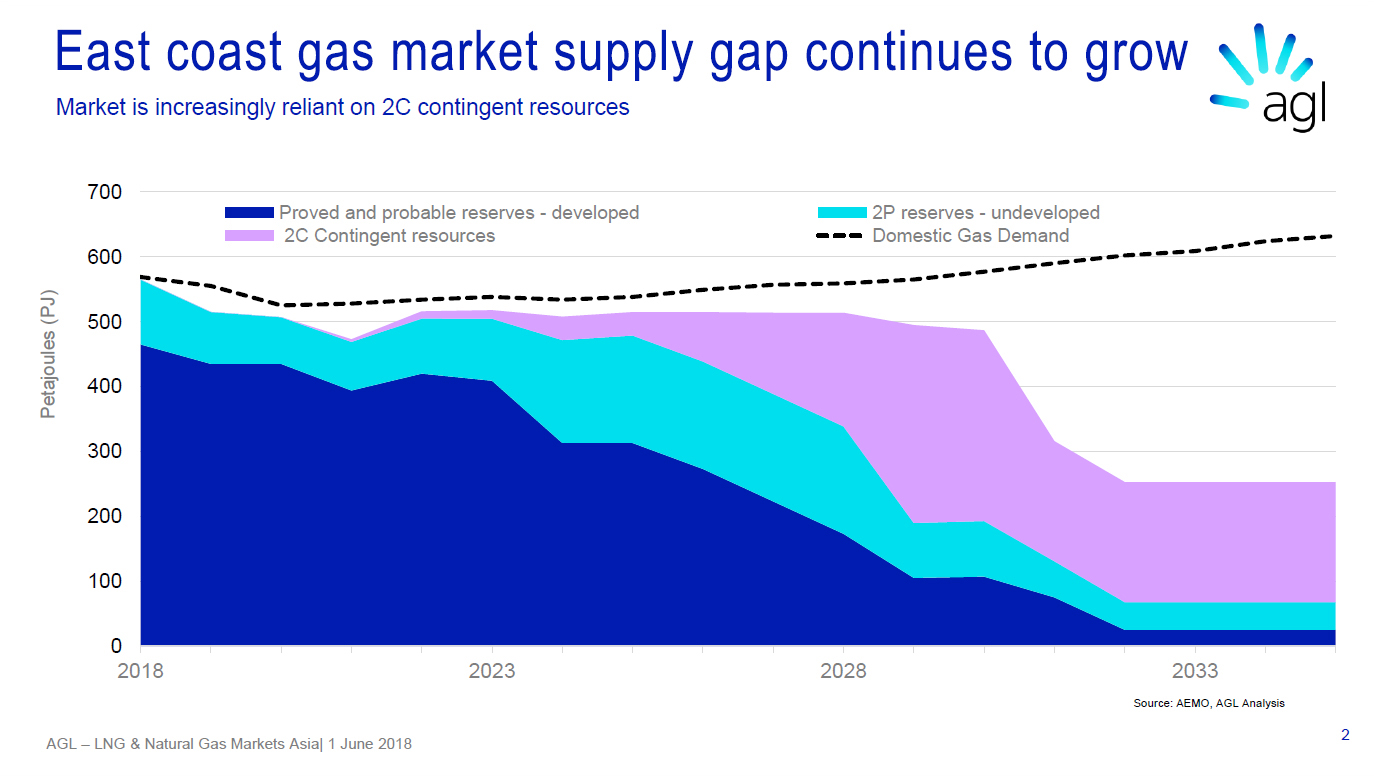

Australia's AGL Energy is targeting a final investment decision (FID) next year on a project to import LNG into Australia by 2021. AGL is currently negotiating with LNG suppliers and FSRU (floating storage and regasification unit) providers for deliveries into Victoria, from where existing pipelines could transport the regasified LNG to domestic markets in South Australia, New South Wales and Tasmania.

Combined with AGL's Australian gas storage facilities, this could underpin the emergence of a liquid Victoria gas/LNG hub.

This trend towards greater Australian gas/LNG flexibility is also evident in Queensland, where Gladstone LNG is already a portfolio player, optimizing gas deliveries between domestic and export markets, depending on eastern Australian gas economics and politics.

Elsewhere in Asia, Thailand is another emerging hub, with state-owned PTT planning to harness its Map Ta Phut regas terminal to offer LNG bunkering and small-scale distribution to its existing truck loading facilities.

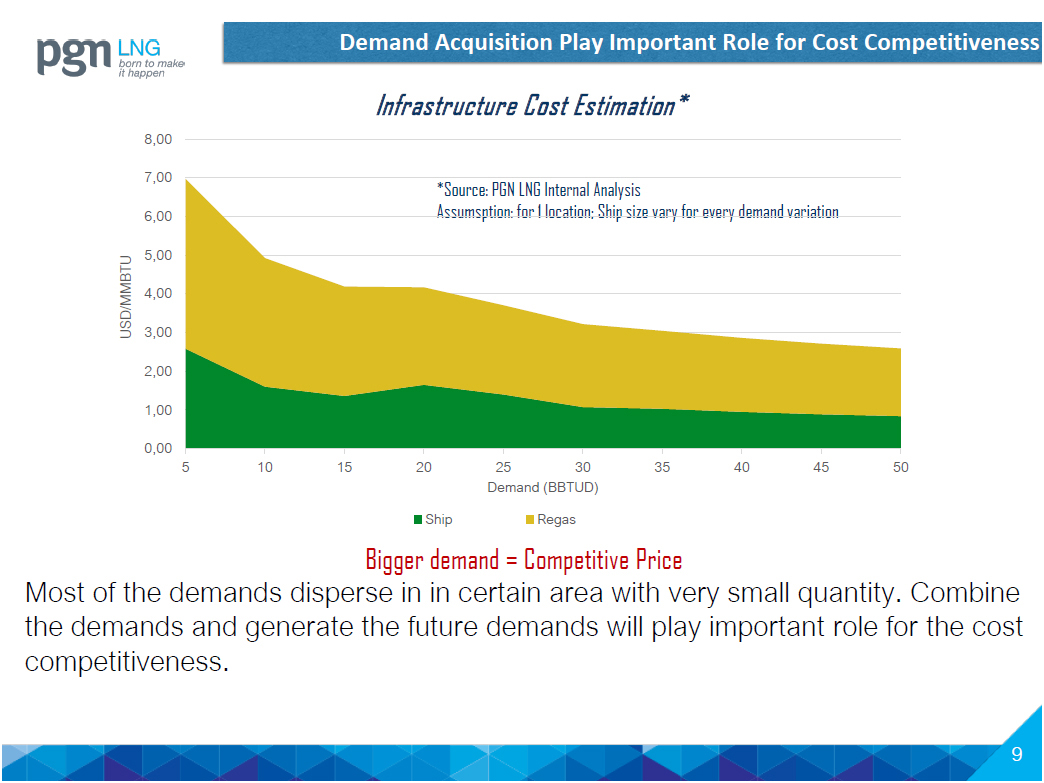

While strong recent northeast Asian LNG buying has been well documented, new tranches of Asian demand could also ramp up. This includes over 40 potential small-scale LNG demand locations across Indonesia, starting at around 30 billion Btu/day (about 200,000 mt/year of LNG), supplied by the country's production hubs, according to PGN LNG. Realizing this potential primarily hinges on competitive LNG pricing, as the required small-scale LNG ships and receiving terminals, to supply 30 billion Btu/d, add over US$3/MMBtu to Indonesian FOB LNG prices.

2. Increasingly transparent, market-based, LNG pricing harnessed

Malaysian state-owned Petronas outlined its intentional allocation of some uncontracted LNG for innovative optimization and for the purpose of enhancing LNG price discovery. As part of this initiative, the company successfully sold its first LNG cargo through the online trading platform GLX last month.

Both Pakistan LNG and Sui Southern Gas Company highlighted Pakistan's transparent LNG procurement processes, which are facilitating the country's rapidly growing LNG imports. This includes competitive bidding for Pakistani spot/short-term purchases as well as long-term supplies from Gunvor, Eni and Trafigura, with the LNG-to-Brent pricing slope publicly available.

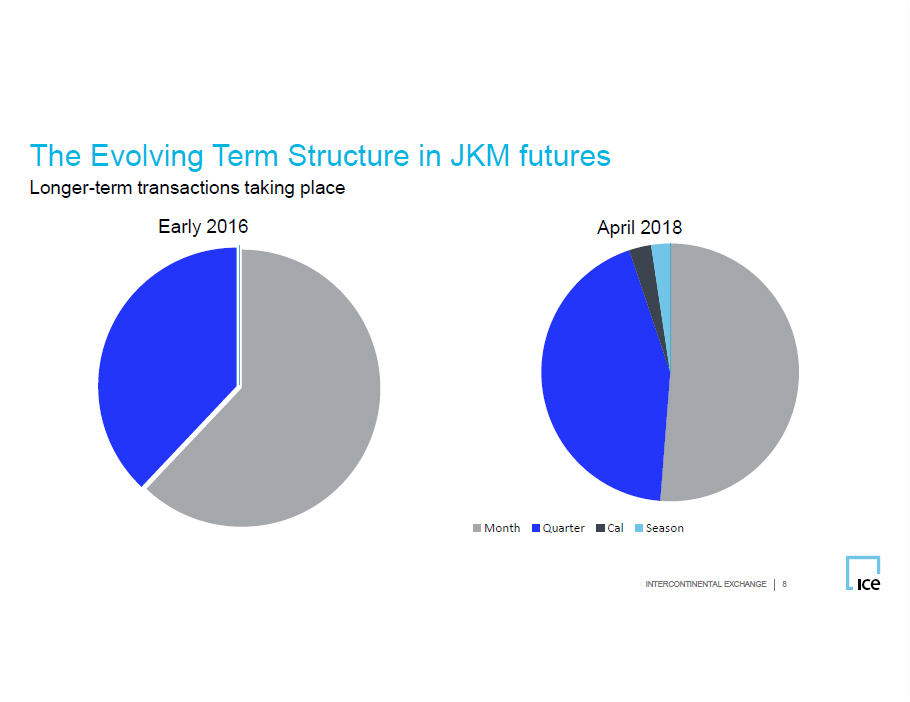

RWE said that, given LNG pricing's increasing complexity, the Platts JKM market represents an effective risk-management tool for LNG spot pricing and is also an effective tool for LNG price formation, supporting price transparency and price awareness.

Intercontinental Exchange (ICE), the largest clearer of JKM derivatives, shared details on the rapid growth in traded volumes as well as tenure length. In May 2018, 3.5 million mt of JKM derivatives cleared on ICE and CME, representing more than fourfold year-on-year growth, in addition to OTC volumes.

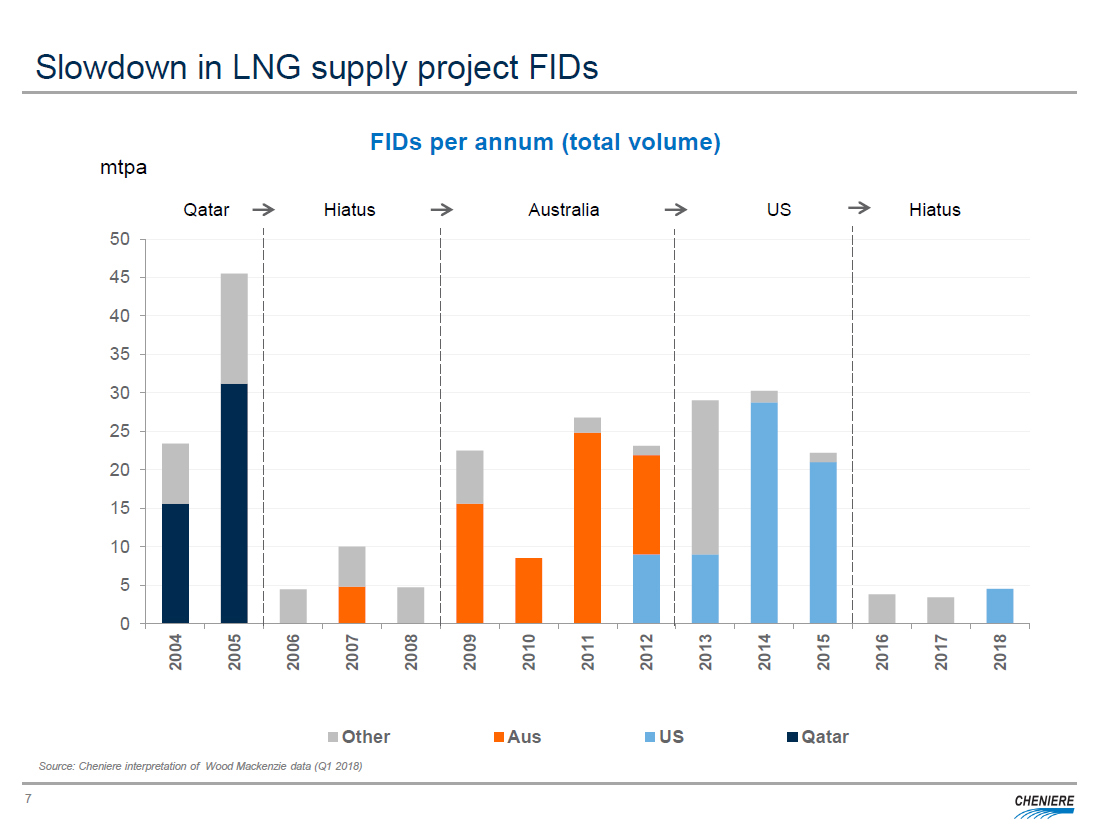

3. Liquefaction FIDs depend on sponsors/financiers successfully evolving with LNG’s commoditization

Since 2016, suppliers and financiers have struggled to adjust to LNG’s increasing flexibility, leading to a dropoff in liquefaction project FIDs. This hiatus was eased by Cheniere’s sanction of Corpus Christi train three, in May. To facilitate their sanction, US liquefaction trains typically offer destination flexibilities, LNG pricing diversification and cost competitiveness, all important facilitators of LNG’s commoditization.

Source: Presentation by Cheniere’s Douglas Wharton at Platts LNG & Natural Gas Markets Asia Conference, Singapore, June 1 2018.

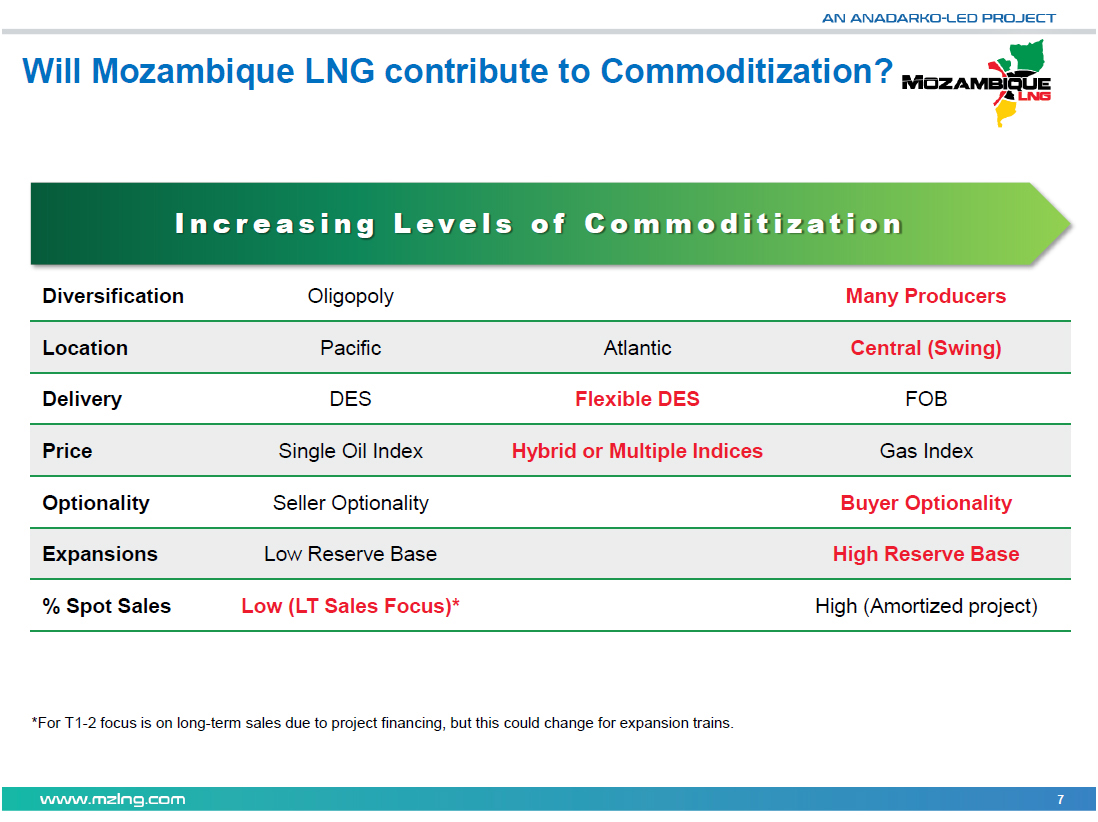

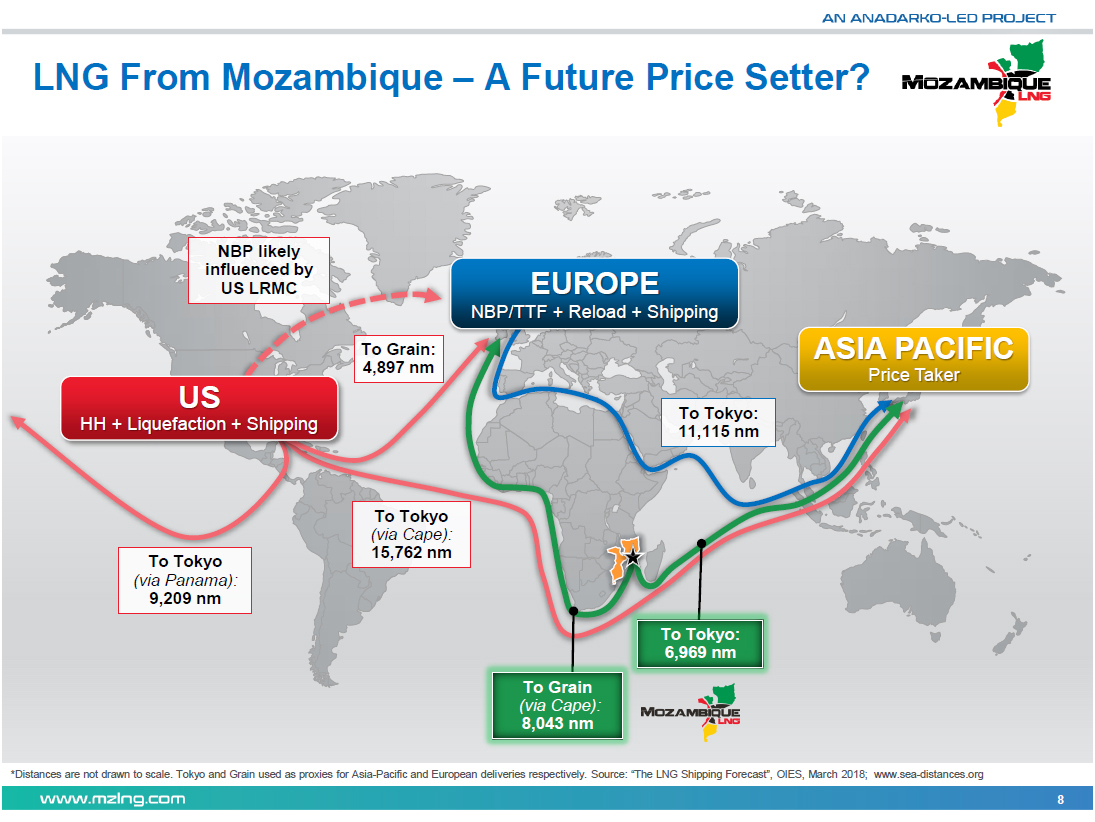

A non-US greenfield proposal, Mozambique LNG, is contributing to LNG's commoditization by offering a combination of flexible DES (delivered ex-ship) contracts, buyer optionality as well as hybrid and multiple LNG pricing indexes.

Mozambique LNG's strategic location also brings opportunities to become a future LNG price setter, by flexibly delivering cargoes to either West of Suez or East of Suez markets.

Many players have already benefited from LNG’s commoditization and opportunities abound

A number of companies – including, as outlined above, Cheniere, ICE, Petronas and Pakistani players - are successfully evolving to grasp opportunities from LNG's increasing commoditization. Additional LNG hubs could emerge in Thailand, Australia and, for small-scale deliveries, Indonesia.

Meanwhile, Pakistan, a fast-growing importer, as well as exchanges and traders, have already benefited from increasingly transparent LNG pricing. Cheniere last month proved the most recent adaptable supplier with its sanction of train 3.

It remains to be seen which will be the next LNG suppliers, buyers and financiers to successfully offer market-friendly flexibilities and cost competitiveness, facilitating their project FIDs, in 2018.