11 Apr 2019 | 14:24 UTC — Insight Blog

Several US regions face hurdles in race to build summer gas stocks

Featuring Brandon Evans

With the withdrawal season officially over, US gas storage fields stand at their second-lowest level in 16 years. Several regions face obstacles as they look to climb out of deep deficits and re-stock before the next heating season begins.

In particular, grid constraints on moving Permian gas, along with a new major export route to Mexico to be commissioned in April and incremental demand from LNG terminals, will make Texas and the Southeast a focal point this summer.

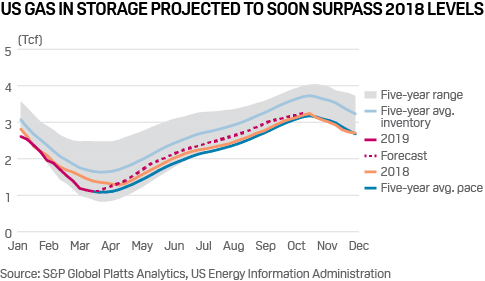

Total US storage inventories tumbled to a low of 1.11 Tcf this year before the first net injection occurred during the last week of March. Outside of winter 2013/14, which featured the frigid polar vortex, the injection season has not started at a lower level since 2003, according to data from the US Energy Information Administration.

Despite starting the season at one of the lowest levels seen in the 21st century, a forecast by S&P Global Platts Analytics projects US inventories reaching volumes on par with 2018 by the end of October. The month is expected to end at 3.25 Tcf, 12% below the five-year average. The current deficit is 31% behind the five-year average.

The forecast represents additions of 2.126 Tcf over the injection season. This is slightly more than usual as fields injected an average of 2.07 Tcf during the season over the past five years. It requires 300 MMcf/d more injected through the summer.

Given the forecast 2.1 Tcf build is close to the five-year average net build, the current deficit will not be eliminated, and as a result, underlying fundamentals should support a summer price closer to $3/MMBtu as opposed to the more recent NYMEX levels of approximately $2.75/MMBtu, according to Platts Analytics. However, multiple regions face hurdles to replenish stocks at or above average.

Pacific region

For example, the Pacific region is currently 44% below the five-year average, and will find trouble rebuilding back to normal without gas curtailments this summer. Total California storage inventories entered the summer injection season at a 10-year low, according to Platts Analytics. The Pacific Gas & Electric system trails the five-year average by 75 Bcf while Southern California Gas Company’s inventories are 10 Bcf behind the three-year average.

Although strong injections late in March helped to narrow the overall deficit, PG&E must nearly double last year’s daily injection average this summer just to reach last year’s record-low summer exit level of 145 Bcf. SoCal Gas must also strengthen injections by 33% year on year to an average of 211 MMcf/d in order to bring inventories back to the system’s already limited storage capacity of 84 Bcf.

With total pipeline receipts likely to remain limited to 2.4 Bcf/d this summer, based on the average system demand the past three years, only 60 MMcf/d of additional volumes will be available for storage. SoCal Gas will likely require operational flow orders and voluntary or mandatory curtailments to keep a lid on demand.

Texas and Southeast regions

Back in the Southeast and Texas storage inventories are poised to exit this summer and enter next winter’s withdrawal season at their lowest mark in the past ten years, according to Platts Analytics. The combination of rising demand from LNG and exports to Mexico, constraints moving Permian gas east on the Texas intrastate grid, and competition with Midwest markets for slowing Northeast production will leave the Southeast and Texas region short in its bid to refill this coming summer, thereby driving stronger price premiums across the Gulf Coast, including at Henry Hub.

While injections in early April have been strong, evidence suggests the refill this summer will be more challenging. Demand in the Southeast and Texas is forecasts to grow 3.4 Bcf/d summer over summer, according to Platts Analytics. Texas exports to Mexico will account for 1.1 Bcf/d of that growth, driven by the massive 2.6 Bcf/d Sur de Texas pipeline, which is set to begin service this month.

Also, incremental LNG feedgas demand from Sabine Pass Train 5, Corpus Christi Trains 1 and 2, Elba Island Trains 1-10, Freeport Train 1 and Cameron Train 1 are expected to add as much as 2.2 Bcf/d of demand summer-over-summer, though risk remains to the downside amid possible construction delays and tightening netbacks to Europe and Asia.

Southeast and Texas inventories currently sit at 381 Bcf, 148 Bcf less than 2018’s mark and 195 Bcf less than the five-year average. Platts forecasts the combined regions will inject 240 Bcf over the course of the summer and fill to roughly 620 Bcf by the end of October, the lowest mark since 2005.

East region

The East region is the best-supplied of all the EIA’s storage regions, relatively speaking, at 22.5% below the five-year average. Despite holding a head start in the refill race over other regions, pricing issues might slow the process, especially in the Northeast.

The summer forward curve for Dominion has become so strong it is trading only 5 cents below the winter 2019/20 strip, according to Platts Analytics. This creates little incentive for people to put gas in storage now and withdraw it later after accounting for cycling costs and the time it spends sitting there. At this time last year, the winter spread was 20 cents higher than the summer spread, creating a greater incentive to store gas over the summer.

Additional reporting by Eric Brooks, Kent Berthoud and Jack Winters, S&P Global Platts Analytics

Register for free to continue reading

Gain access to exclusive research, events and more

Already have an account?Log in here