05 Mar 2020 | 18:07 UTC — Insight Blog

Europe’s largest gas field is winding down, but market has plenty of alternatives

By Kira Savcenko and Gary Hornby

The Netherlands’ Groningen field is entering its final chapter as a major supplier of natural gas to the continent.

In 2022, eight years earlier than originally planned, output from Europe’s largest field will finally come to a halt. Stepped reductions were introduced from 2013, due to the risk of earthquakes in the region triggered by production drilling.

The move will leave the European gas market 54 Bcm/year shorter compared with 2013.

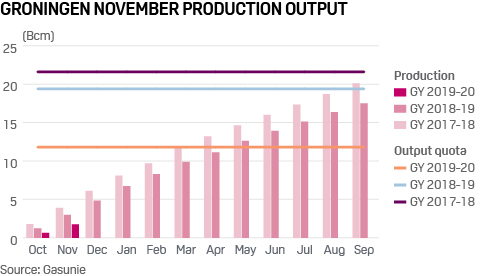

The pace of the phase out has speeded up since the process began. Most recently, the Dutch government announced in late February that for the current gas year (October 1, 2019, to September 30, 2020), production can be lowered to 10 Bcm, from an initial target of 11.8 Bcm.

But this further reduction in output from Groningen will have a limited impact on prices, given that robust LNG imports look set to remain the norm into Europe and increasing Russian production will boost pipeline supplies from the East.

Go deeper: Special report – The future of European gas after Groningen

One reason behind the latest reduction to a 10 Bcm target is the unusually mild winter that Europe has seen, limiting heating demand in the region for the second successive winter season, allowing for huge storage stocks to be carried over into the summer.

“In a market with a bullish sentiment, it would have led to some reaction. But in this very bearish environment, it will provide just a little bit of support,” a Germany-based gas trader said.

Groningen's history

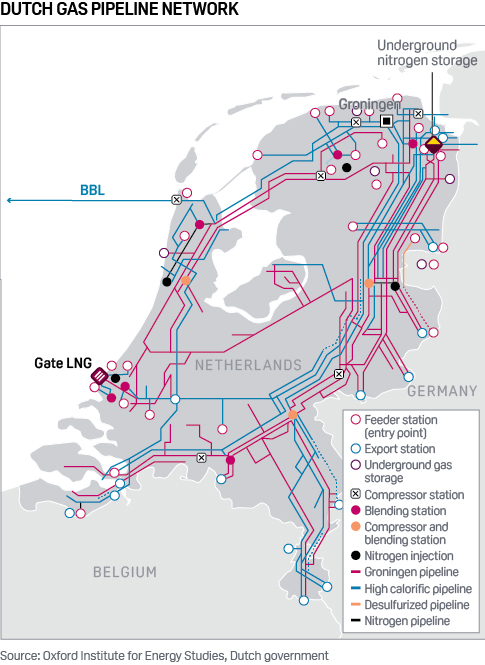

Production at Groningen began in 1963, hitting a record high of 87.7 Bcm 13 years later in 1976. Infrastructure around the field was developed to supply consumers in the Netherlands, Germany, Belgium, and northern France, supported by a combination of large production volumes and low costs.

This reliance on Groningen came despite the fact that, pound for pound, Groningen gas has less energy than gas sources from the likes of Norway and Russia. Groningen’s gas contains a high concentration of nitrogen and is classed as low-calorific gas, unlike alternatives from other sources with lower nitrogen content – high-calorific gas.

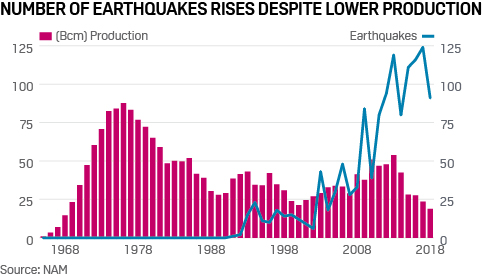

Research into the field’s environmental impact began in 2012 following a 3.6-magnitude earthquake in Huizinge, which also massively swung public opinion surrounding the field, prompting the creation of the State Supervision of Mines.

Production from the Groningen field has declined sharply since 2013

In 2013, the decision was made to cap output from the Groningen gas field, effectively limiting the amount of gas that could be extracted on an annual basis. However, earthquake numbers failed to fall in line with weaker output – extraction fell back to 28.1 Bcm in 2015, and to its lowest in 50 years in 2018 as production stood at a mere 18.83 Bcm.

The Groningen field is currently slated to end gas extraction in 2022, a decision announced in September 2019. However, it will still be needed on hand for a few years, for security of supply in case of extremely cold winters.

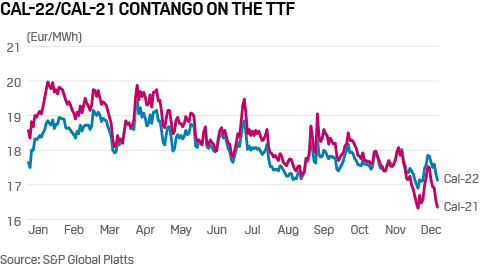

Market contango

In general, the Groningen phase out might have a moderate bullish impact on gas prices, as the market will be less flexible and more dependent on pipeline imports and LNG. This trend can be seen in the 2022/2021 contango on the pivotal Dutch TTF trading hub with 2022 prices almost Eur2/MWh above the 2021 price during 2019.

Similarly, in 2020 so far, the premium of TTF’s 2022 prices over the 2021 averaged Eur1.32/MWh, S&P Global Platts pricing data showed. The premium climbed to its highest level of Eur1.70/MWh late February.

At the same time, liquidity on the TTF is expected to continue rising, with the upcoming single trading hub in Germany unlikely to become a serious rival. TTF liquidity stood at a whopping 38,037 TWh in 2019, an annual increase of some 40%, compared to physical throughput of 581 TWh, bringing an effective annual churn rate of 65 last year, Gasunie data showed.

For comparison, during the 54 Bcm production 2013 year, TTF liquidity came in at 8,286 TWh with a churn rate of 19.

Russian gas

By 2025, Northwest Europe will need to replace about 45 Bcm of gas given the phase-out of Groningen and other declines in regional gas output, according to Platts Analytics. This shortage is likely to covered by an increase in

Russian supplyof about 20 Bcm/year with the rest being covered by LNG imports.

Currently, Russian gas enters Europe through three main points. Imports via Nord Stream 1 through the German Greifswald entry point are around 55 Bcm/year, while Poland’s Kondratki flows reach around 32 Bcm/year. Under the new five-year agreement reached late 2019, Ukraine will transit 65 Bcm of Russian gas to Europe in 2020 and at least 40 Bcm/year in 2021-24.

In addition, Nord Stream 2 – which will double the capacity of the gas corridor via the Baltic Sea to Germany to 110 Bcm/year – might start flowing gas in late 2020 or early 2021.

Gazprom aims to invest in around 250 Bcm/year of new production capacity to come online by 2025, which would be enough to compensate for the decline in production of the Soviet legacy fields in the Nadym-Pur-Taz region. Most of these new production capacities will feed into the export system to Europe.

Russian pipeline flows are also seeing a boost from spot sales on Gazprom Export’s electronic sales platform, with more volumes being delivered to Central and Eastern Europe.

Since September 2018, an increasing proportion of Russian gas is sold on Gazprom Export’s Electronic Sales Platform (ESP), with daily auctions set to be a permanent part of the company’s overall sales. Cumulative sales on the ESP now total 23.29 Bcm since the first sale took place.

Strong LNG regas

Regasification of LNG across main European markets began to show signs of increasing in October 2018 and has continued to rise. Higher production from the likes of the US, Australia, and Russia, has found a home in the European gas grid.

Total LNG sendout volumes in UK, Belgium, France, Netherlands, Italy and Spain were about 36% higher on the year February to date at over 270 million cu m/day, data from S&P Global Platts Analytics showed.

The dynamics of increasing imports to Europe, along with a surge of further new production coming online in the US Gulf Coast, Qatar, and Australia indicates that LNG will be one of the main sources to replace missing gas from the Dutch giant Groningen field.

During 2019, the LNG glut became one of the main bearish price drivers on the European gas hubs, however, looking ahead, market participants think that further pressure may be limited.

The European gas community does not seem to be worried by the Groningen’s phase-out, especially given that it comes during the time of robust supply. With sufficient LNG and Russian imports, along with a renewable energy eating into gas share of the power mix, Groningen’s volumes can be easily replaced, limiting any potential price impact on the European hubs.