28 Feb 2018 | 15:30 UTC — Insight Blog

LNG's structural evolution quickens in February

By Marc Howson

The LNG industry is currently in a cycle of unprecedented supply growth, and market developments in February re-emphasized the ongoing structural evolution.

LNG is moving towards a more advanced market structure, characterized by growing market-based pricing and hedging as well as increased buyer confidence in spot or short-term buying. Three developments in February highlighted this.

1. KOGAS-NWS: HIGH-PROFILE ASIAN LNG PRICING ARBITRATION HIGHLIGHTS GROWING NEED FOR MORE MARKET-BASED LNG PRICING

In February, Kogas announced it has entered into arbitration with North West Shelf Gas. The arbitration was probably related to the oil-linked pricing of a term LNG contract.

According to Macquarie's December Global LNG report, "feedback from legal groups identified almost 80 LNG disputes, with more half since 2010. Interestingly, in the vast majority of these disputes, one or more parties eventually resorted to filing arbitration or litigation to resolve their disagreement … Pricing has been the most frequent subject of the disputes."

Over the duration of a term contract, using market-based LNG pricing can reduce incentives for one of the counterparties to re-negotiate/dispute/arbitrate the contract's pricing terms.

LNG price benchmark Platts JKM is increasingly used in spot and term LNG transactions as counterparties seek a pricing basis that reflects market fundamentals.

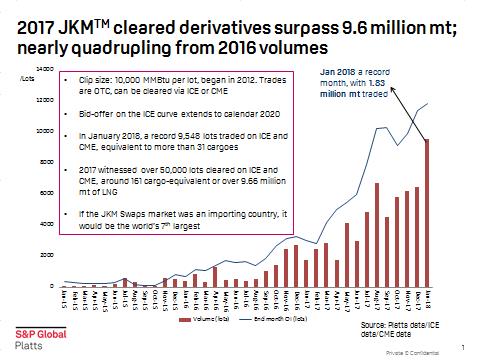

2. RECORD EARLY-2018 LNG DERIVATIVES TRADE: UNDERPINNED BY INCREASING HEDGING OF MARKET-BASED LNG PRICING

As counterparties' exposure to JKM rises, market participants increasingly manage their physical pricing exposure in the financial markets.

As a result, JKM derivatives trade, cleared on both ICE and CME, quadrupled year on year in 2017.

January traded volumes hit a new record, equivalent of over 31 standard-sized cargoes, an almost 50% month-on-month increase, data released in early February showed.

More than 30 participants were active in the JKM derivatives market in January.

3. CHENIERE AND MOZAMBIQUE LNG LONG-TERM LNG CONTRACTS AGREED FOR SMALLER VOLUMES: BUYERS INCREASINGLY CONFIDENT WITH SPOT/SHORT-TERM LNG PROCUREMENT

In February, both Cheniere and Mozambique LNG announced long-term 1.2 million mt/year LNG supply contracts with CNPC and EDF.

This followed Cheniere's 1 million mt/year term contract with Trafigura, announced in January, and Mozambique LNG's 280,000 mt/year December term agreement with Tohoku Electric Co.

The volumes are significantly less than the average of 2 million mt/year seen in 2010, indicating increasing buyer confidence in the spot/short-term market.

Suppliers responded by proposing smaller-scale liquefaction trains to match these evolving buyer requirements, most notably Woodside's Pluto expansion in Australia and Sempra’s Costa Azul in western Mexico.

4. INCREASED FLEXIBILITY AND EFFICIENCY CAN ENHANCE LONG-TERM LNG RELATIONSHIPS WHILE OFFERING SUPPLIERS/FINANCIERS FIRST-MOVER ADVANTAGE

LNG's increasing flexibility can enhance the industry's vital long-term relationships and investments through more market-based and efficient transactions.

Other commodities, particularly iron ore since 2010, have exhibited similar progression towards a more advanced market.

LNG sellers and financiers are likely to gain valuable first-mover advantage, potentially including breaking through the current hiatus on liquefaction project FIDs if this trend is embraced, instead of being resisted.