19 Jan 2017 | 16:00 UTC — Insight Blog

The Middle East comes into its own as a LNG demand center

When you think of LNG in the Middle East you generally think of largescale exports from Qatar, the world’s largest exporter of the super-chilled fuel. Over the past two years, however, the region has grown into a recognized demand center because of increasing imports from both traditional buyers and new market entrants.

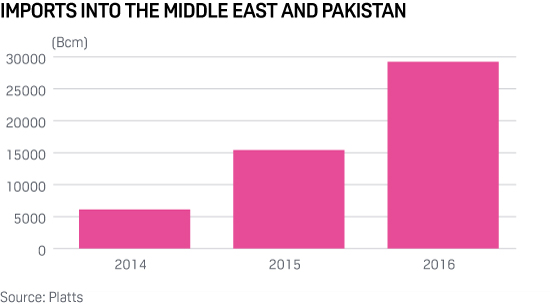

In 2014, the three countries in the region importing LNG – Kuwait, Israel and the UAE – received of 6.1 Bcm of gas equivalent.

In 2016, imports into the region reached 24.5 Bcm, due to increasing deliveries to traditional importers and new importers like Egypt and Jordan. This figure rises to 29.2 Bcm, when Pakistan – another new importer – is also considered.

To put that in a global context, the region has moved from being responsible for less than 2% of total LNG imports in 2014 to accounting for more than 8% in 2016.

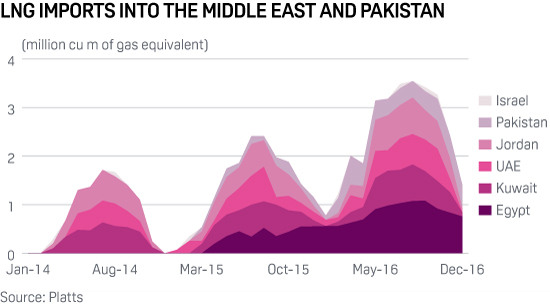

Most of the rise in regional imports has come from these new market entrants, who accounted for 66% of deliveries in 2016.

Egypt, Jordan, and Pakistan have made such a big impact because of their use of Floating Storage and Regasification Units (FSRUs), which are a quicker and cheaper option than building onshore regasification facilities.

These FSRU’s have allowed the new entrants to access the LNG market quickly and capitalize on rapidly declining LNG spot prices in recent years.

All three of the new importing countries set up their FSRUs in 2015, a year when LNG spot prices dropped to around half of what they were over the previous two years.

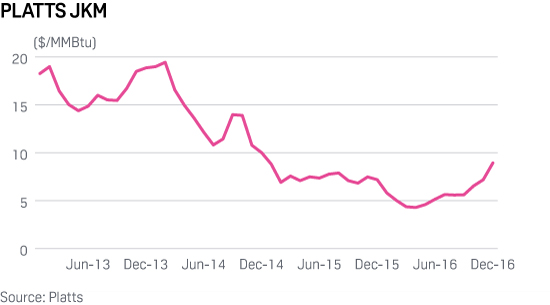

This is seen in the Platts JKM, which is a reflection of the value of a spot cargo delivered into the traditionally premium market of Northeast Asia. The average value of the Platts JKM for 2015 was $7.458/MMBtu, well below the $13.878/MMBtu in 2014, and $16.37/MMBtu 2013.

In 2016, JKM prices have remained low, averaging $5.72/MMBtu over the year.

Platts JKM

This lower price environment has been driving further adoption of LNG as a fuel source in the region. Egypt, for example, managed to secure the delivery of a second FSRU in the same year that it received its first. Meanwhile, plans for the chartering of a third FSRU, which began in 2016, have been put on hold pending the assessment of prospects for increasing domestic gas production.

The UAE, which has an existing import terminal in Dubai, recently secured a second FSRU-based import terminal in Abu Dhabi in August 2016 which has been operational since September.

Bahrain is also set to enter the LNG market in coming years, though it has opted to use a Floating Storage Unit and an onshore regasification terminal rather than an FSRU. Construction of the terminal is scheduled to being in January 2017 and to be completed by 2019.

Just outside the Middle East, companies in Pakistan have arranged for the installation of two additional FSRU-based import terminals over the next two years. The first for the two has been chartered from BW Group, and is expected to begin operation by mid-2017. Preparation for the installation of the second FSRU, charted from Hoegh LNG, is set to begin in early 2017, with the start of the project set for 2018.

Given the latent demand for LNG in Pakistan, which suffers from electricity and gas shortages, and the additional regasification capacity from two FSRUs, Pakistan could become a major import destination.

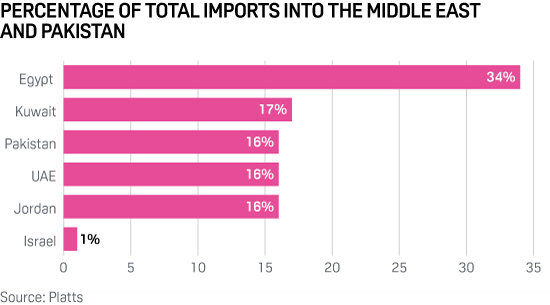

For the time being, however, Egypt remains by far the largest importer in the region, accounting for over one-third of deliveries in 2016, more than twice that of any other importer.

S&P Global Platts launches LNG assessment for Middle East

https://www.youtube.com/watch?v=s9XcRmo18Cs

Our editors discuss S&P Global Platts new Middle East Marker (MEM) price assessment, which reflects the growing importance of the Middle East as an LNG import destination rather than just exporter of cargoes. For more information on the assessment, visit Platts.com