16 Jan 2019 | 18:41 UTC — Insight Blog

Less volatile gas prices give newest US LNG plant smoother start-up

Featuring Jason Lord

US LNG export projects, whether brownfield or greenfield, are multi-year, billion dollar projects. While construction timelines dictate their commissioning schedule, there can be inconvenient and convenient times in the unpredictable natural gas market to begin this testing.

The two most recent additions to the US fleet of natural gas liquefaction and export facilities - Cove Point LNG and Corpus Christi LNG - demonstrate this. They began operations about one year apart during the winter months, when gas prices are typically elevated, but disparate conditions over the two winters meant vastly different feedgas costs in the critical ramp-up phase.

Corpus Christi, located in Texas, is the latest facility to begin commissioning. It has been making progress toward commercial operation at Train 1 following that train’s first cargo export onboard the Maria Energy, December 11. Meanwhile, its second train recently received Federal Energy Regulatory Commission approval for fuel gas introduction.

Corpus Christi facility has enjoyed unusually low 2018-2019 winter gas prices in the Southeast and East Texas. Henry Hub’s cash settlement on Thursday January 3, 2019 priced at $2.685/MMBtu, its lowest price back to May 4, 2018, when it was trading at the same price. Prices since then have climbed back above $3/MMBtu, trading at $3.36/MMBtu on January 14, a three week high.

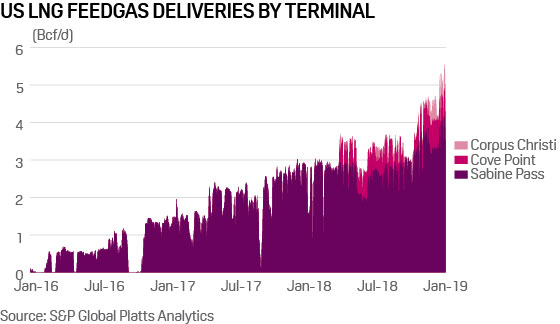

S&P Global Platts Analytics data shows that flows for the January 4 and 5 gas days were record-setting, with total US LNG feedgas demand reaching 5.5 Bcf/d, including feedgas demand pull from Sabine Pass, Cove Point and Corpus Christi.

One year ago, the US gas market dealt quite a different hand to Maryland’s Cove Point facility during its commissioning period.

On January 3, 2018 Henry Hub’s cash price spiked to $6.875/MMBtu, its highest cash price of 2018.

Cove Point ended up being delayed with its lone Train 1 commissioning. Data from Platts Analytics showed LNG feedgas demand pull didn’t kick in substantially until January 31, 2018 when 206 MMcf/d of feed gas flowed to the facility. On that date, Transco Zone 5 priced at $4.58/MMBtu and Transco Zone 6 non-NY was $4.62/MMBtu.

Dominion, the owner of the Cove Point facility, blamed the delays on “typical start-up issues.”

This start-up delay occurred at a time in January when there were also record cold temperatures in early 2018 that led to cash prices above $100/MMBtu. Transco Zone 5 and Transco Zone 6 non-New York on January 4, 2018, spiked to $127.00/MMBtu and $124.735/MMBtu, respectively, the two locations' highest cash prices ever. Cove Point's first cargo ultimately was shipped in March 2018.

Cash natural gas prices are certainly not the only factor affecting for terminal start-up schedules, but LNG facility commissioning timelines could be impacted by the volatile prices of the winter natural gas market.

Platts Analytics data shows that Cove Point had the longest duration in days, of any recent US lower 48 liquefaction train, between FERC fuel and feedgas approvals to first significant (100 MMcf/d) flows at 299 days from their fuel gas approval and 153 days from their feedgas approval.

In comparison, Cheniere’s Corpus Christi Train 1 had 139 days between its fuel gas approval and significant flows above 100 MMcf/d. Even shorter, at 55 days was its feedgas approval timeline to significant flows, Platts Analytics data shows.

While Cove Point only has one train at its facility, Corpus Christi’s continuing progression in the commissioning of its second train may be helped by historically low natural gas prices that have returned to Texas and the Southeast this winter and at the start of 2019.