21 Oct 2015 | 09:31 UTC — Insight Blog

The bears are back in town: Takeaways from London Metal Exchange week

By Henry Van

A “subdued” tone, “the most uninspired week I can remember,” and a poll suggesting only 3% of people believe that Chinese growth rates are what we are told — there was no doubt that the toreros of metal markets had left their bulls at home when they came to London for the annual meeting of traders, brokers, consumers and end-users of metal at this year’s London Metal Exchange week.

At first glance, the fanfare around LME week was said to be similar to years gone by. Conferences in lavish hotels by day and company sponsored receptions by night, but layered with a more solemn mood among the guests. “The food is not as good as it used to be” and “every year there are fewer events” were oft repeated lines among those attending. Considering the state of metals markets, it is no surprise that policies of cost cutting would deter investment in corporate functions.

On top of weak market fundamentals across the metals complex, the number of LME ring-dealing members fell to nine after JP Morgan’s September announcement that it would leave. Compounded with the recent rise of the Shanghai Futures Exchange, having released a nickel contract in March this year which now trades 90% of LME volumes, sentiment was uneasy and questions remained unanswered on what the shape of futures markets would be looking forward.

China doesn’t pander to oversupply

Comparing fundamentals to 12 months ago, it’s not hard to understand the depressed sentiment. In broad strokes, China had not consumed metal at a fast enough rate to keep up with global mine capacity. Comparing the first seven months of 2015 to the same period in 2014 provides some context. According to the World Bureau of Metal Statistics, global mine production of copper grew by 3.42%, yet global refined copper consumption grew by a meager 0.26%, with Chinese growth coming in at 0.69%. Furthermore, China produced and imported less copper over the same period, inferring a draw-down in previously imported warehouse stocks.

This story is well documented and conference halls of London last week converged into an echo chamber resonating with the words “China’s new normal,” indicating that the market must adapt to a slowdown in growth or be swamped in supply. Consciously or not, the market has adapted with vast production cuts. According to Citi Research, 1.6 million mt of copper have been removed from supply this year, with Glencore leading the pack following the suspension of two African copper mines, Katanga in the DRC and Mopani in Zambia, back in early September. More recently, Glencore further lowered their output following the sale of Australian and Chilean copper mines.

Between the first production cuts and LME week, the International Copper Study Group made considerable revisions to their outlook. The new forecast predicted that the market would move into supply deficit in 2016, citing production cuts as the driver of change. Other institutions followed and further cuts were made across the LME metal complex, with Glencore announcing a 33% reduction in zinc production and aluminum major Chinalco shutting 12.5% of its smelting capacity.

Physical prices turn their back to the futures

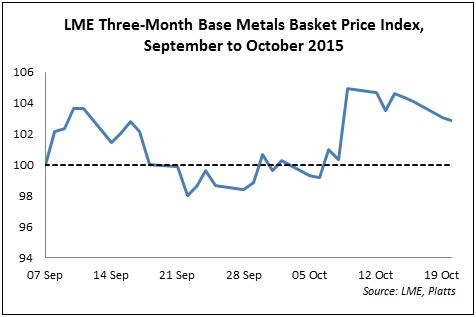

Production cuts leading up to LME week changed the 2016 outlook of many analysts, with expectations filtering into futures prices. The chart below tracks the prices of a basket of six LME metals through September and October, indexed on Sept. 7, 2015, the day Glencore announced the first production cutbacks.

While the index traded higher during LME week, several traders argued that the cause of higher price levels was a result of an isolated event on Oct. 9: the Glencore announcement that it would reduce zinc production by approximately a third. This caused zinc prices to rally 9.78% in one day, with prices moving to $1,851/mt. Subsequently, the first conferences of LME week on Monday, October 12, were packed with upward adjustments to zinc prices in 2016. Macquarie Research’s punt was that zinc would reach $3,000/mt by October 2016 with the audience widely agreeing, voting it the most preferred long metal on a 12-month view.

As the week went on, the euphoric sentiment surrounding zinc started to dissipate. Attendees at company receptions noted that zinc concentrate had been in surplus for several years now. Every year, LME week provided some upside sentiment, they said, and every year the wait for a tighter market continued. However, several traders noted that treatment and refining charges (TC/RCs) had dropped in the last few months, indicative of lower demand to refine zinc concentrate and a tighter market. For zinc, many hope that this year will be the payoff of several years of pain.

Aluminum: The biggest bear in the room

Aluminum was regarded as biggest victim of oversupply, with fewer production cuts and soaring Chinese semi exports throughout 2015, which amounted to 350,000 mt in September according to Investec, up 2.8% from August. However, there was skepticism surrounding whether the policy of increasing exports is sustainable looking forward.

“There is no real demand for these exports,” one trader commented. “The only reason that exports are still up is to keep up appearances. A lot of this exported material is just sitting in a warehouse in Mexico.”

Copper physicals turn their back on the futures

Event speakers tagged onto this LME “mini-rally” as a reason that production cuts would lead to more balance in the copper market. However, outside the conference hall there was less optimism on whether this would translate to physical momentum. Notably, the release of Codelco’s 2016 European term contract for copper cathode of $92/mt, 18% lower than 2015.

On top of this, there was talk that Codelco would reduce its premiums for material to China to as low $100/mt, representing a 24.81% drop from 2015. Even if the official premium is higher than this, it is indicative of a mood that the fundamental issues facing the market today will not soon go away.

The Chinese takeaway: transparency and oversupply

There was no uniform answer to why fundamentals looked so bleak next year. Some pointed to announcements from other major producers, Rio Tinto and BHP Billiton, to cut the production required to further balance the market. Others mentioned skepticism towards whether China was able to execute a more consolidated infrastructure spending plan, particularly relating to power grid expenditure.

The most novel answer was one of transparency. Following on from the Qingdao port scandal in mid-2014, many metal financing agreements in bonded warehouses became untenable. This led to more metal stock being pushed into LME warehouses on warrant, explaining the ballooning of copper stocks earlier this year. The narrative goes that the unwinding of financing deals provided more transparency this year for the level of global copper stocks, making it harder to hide oversupply and contributing to a bulging surplus unless lower production or higher infrastructure spending is undertaken.

Whatever the reasoning, the unifying trend was that few thought these fundamental issues had quick fix solutions. For the moment, adapting to a “new normal” way to do business looks imperative to succeed in the metals industry.