12 Jul 2018 | 20:51 UTC — Insight Blog

Has an Australia-to-Europe iron ore arbitrage opened?

By Ciaran Roe and Jeffery Lu

China has long been the epicenter of the iron ore market. Australian miners’ medium grade iron ore fines are the foundation of China’s sinter feed, with other regions having to compete for space in the mix.

Radical changes in procurement preferences in China this year, though, have pushed down the price of Australia-origin ores compared to Brazil’s, potentially opening up an arbitrage opportunity for Australian material to other regions.

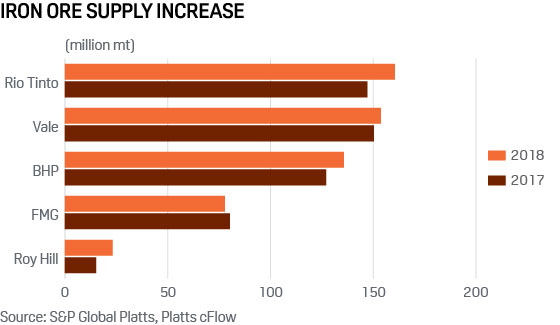

Australia’s supply of higher alumina-content iron ore has increased this year at a time when supply of competing Brazilian (low alumina) ore has eased. This has caused a change in the price steelmakers are placing on alumina content in iron ore.

Compounding this has been a reduction in China-produced iron ore, which typically has low alumina content.

These changes have made Australia-origin medium grade fines appear economic to some European steelmakers, procurement representatives said at a recent industry conference.

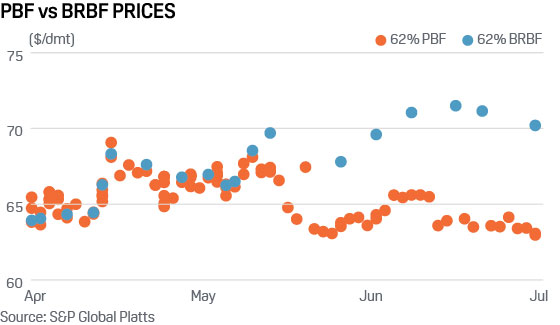

The penalty for higher alumina content, or the premium for lower alumina content ores, has shot upward.

Having started the year at $1.8 per 1% of alumina, Platts’ assessment for this impurity has spiraled upwards, hitting a record high of $8.5 per 1% at the end of Q2.

EUROPEAN PIVOT

In this context, an arbitrage for Australia-origin ores may have opened to Europe.

While occasional spot cargoes of Australia-origin ore have been sold into Europe on an opportunistic basis, a regular flow hasn’t really existed. Europe, due to Brazil’s freight advantages – and historical usage of Brazil-origin ores – has been consistent in its procurement.

However, today’s market conditions could change this.

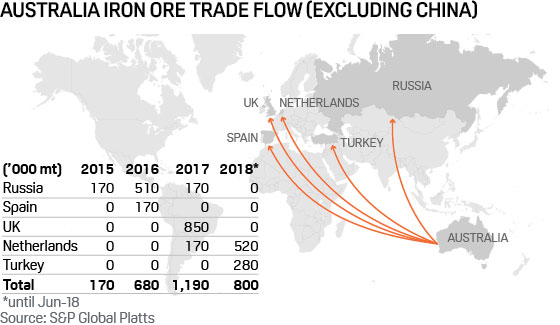

Data from Platts trade flow software cFlow indicates that iron ore shipments from Australia to Europe have increased this year on an annualized basis, albeit from a very low base. Only seven Capesize vessels were seen going from Australia to Europe in 2017, five in 2018 year-to-date.

A structural issue for Australia’s iron ore miners is their higher freight costs to Europe. On an indicative basis, however, this has narrowed to only a $2/wmt disadvantage versus Brazilian competitors now from around $4/wmt at the start of Q2.

And, given that today Vale’s Brazilian Blend Fines (BRBF) is achieving $6/dmt more than Rio Tinto’s Pilbara Blend Fines delivered into China, diverting material to Europe may be attractive.

The barrier may be on the buyers’ side though. Europe’s blast furnace steel mills have typically preferred stable blends of sinter, most of which is procured from Brazil. While Australia-origin fines could be blended with lower-alumina Brazilian ore to achieve a similar mix, Australia’s route in to Europe may be stymied by buyers’ reticence to change.

However, some Europe’s steelmakers are considering purchasing more Australia-origin ore to broaden their supply base. At a recent industry conference in Europe, several local steelmakers stated they were considering increasing their exposure to Australia-origin material.