08 Jul 2019 | 11:33 UTC — Insight Blog

Commodity Tracker: 5 charts to watch this week

S&P Global Platts editors’ pick of unfolding commodities trends. This week, record iron ore prices are crushing Chinese steelmakers' margins and Germany's coal-fired generation is under intense pressure from gas and renewables, while in European wholesale gas markets, Gazprom is registering ever-higher sales through its auction platform. Finally, OPEC is targeting a thorough rebalancing of the oil market, and we take a look at the latest moves in coffee prices.

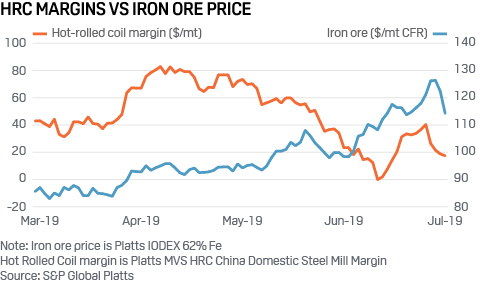

1. Record iron ore prices could force Chinese mills to trim output

What’s happening? Spot iron ore prices reached their highest level since early 2014, hitting $126.35/mt CFR China for 62% Fe iron ore fines on July 3, before easing slightly. This is largely due to the supply outage in Brazil following Vale’s accident in January, and slower exports from Rio Tinto. S&P Global Market Intelligence has forecast a seaborne deficit of 36 million mt this year. Chinese producers of hot-rolled coil have struggled to pass these costs through to finished steel prices because of weak end-user segments, notably manufacturing. As a result, margins have been severely eroded with steelmakers at times producing below cost.

What’s next? With the iron ore shortage set to prevail this year and spot prices likely to remain high, much depends on the underlying strength of China’s economy to support domestic steel demand. Iron ore prices could become even more stratospheric, putting steel margins under intense pressure, and potentially resulting in Chinese mills trimming some output.

2. Cheap gas squeezes coal to new lows in Germany

What’s happening? German coal- and lignite-fired power generation fell 22% on year in H1 2019, as rising carbon prices and cheap gas helped trigger significant coal-to-gas switching. Plant closures and lignite mining restrictions as well as record wind and solar added further pressure. The trend is set to accelerate in Q3 with S&P Global Platts Analytics forecasting hard-coal generation to decline by over 60%, while gas generation is set to double compared with Q3 2018.

What’s next? Lignite, Germany’s single biggest power source, is now facing headwinds too. Utility EnBW has already taken a 900 MW unit offline in June, citing economic reasons. Lignite generation has proved much more resilient than coal in recent years, so the closure could be a sign of a new inflection point. Further out, year-ahead generation margins show modern coal plant again ahead of gas plants, with EUA carbon price and global gas price developments key for future profitability. Germany plans to phase out coal by 2038 at the latest with a first wave of hard-coal plant closures to be determined by auction.

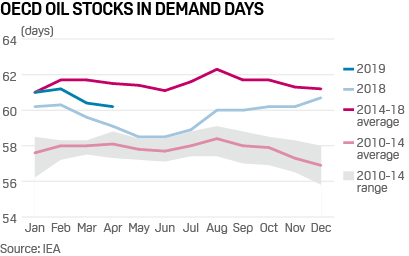

3. OPEC targets oil stocks as it seeks to rebalance market

What’s happening? OPEC is dusting off plans for a new metric to measure the success of its ongoing 1.2 million b/d output cuts, but the main option on the table -- targeting lower stocks -- means the group would need much deeper and longer curbs to rebalance the global oil market. The group is now keen to adjust its target to take account of the creep in global oil stock capacity over recent years. It would focus on the five-year average for 2010-2014 rather than the current rolling five-year average.

What’s next? OPEC and its allies’ monitoring committee will meet in September to assess crude inventory levels and whether the new barometer is effective. Compared to the five-year average from 2014-2018, the 2010-2014 OECD oil stock average is 214 million barrels lower, or some 7.5% of the total 2.89 trillion barrels stock levels, IEA data show. The IEA report this week could give more clues on the market balancing narrative.

4. Gas sales soar on Gazprom’s European auction platform

What’s happening? Sales of Russian gas via the Electronic Sales Platform (ESP) have surged over the last months and are keeping momentum at the start of July. Last Thursday alone, Gazprom sold 229 million cu m, an all-time high. Gazprom uses the platform to market volumes that its long-term buyers turn down, within limits permitted by their take-or-pay contracts. Some ESP sales are also directed to new customers. The rising sales suggest Gazprom’s willingness to prioritize market share over value.

What’s next? Gazprom said it is “comfortable” with its current gas export strategy, and plunging hub prices in Europe should keep buyers interested in the ESP sales. However, planned maintenance on the Nord Stream pipeline in the second half of July will reduce Gazprom’s transport capacity by 150 million cu m/day, or 30%, and this could negatively impact volumes offered on the platform.

Bonus chart: Coffee prices stage rebound on new crop concerns

What's happening? After years of constant declines, global coffee prices made a minor comeback this week on growing concerns over cold weather hitting crops yield in top-grower Brazil. The benchmark September ICE futures contract for Arabia coffee rose to a seven-month high Friday at up to $1.15/pound, the highest since November 2018, amid fears of frost damage in some of Brazil's top coffee growing states. The price rally came two days after the International Coffee Organization trimmed its estimates for global coffee surplus this year. Strength in the Brazilian real against the dollar, which can discourages export sales by Brazilian producers, also supported prices.

What's next? Traders will be keeping an eye on weather conditions as the Brazilian harvest progresses. The current cold front’s impact could be limited given forecasts of a global production surplus for the current coffee year (October-September), even as the ICO projects global demand for the commodity to rise by 2%, to 164.6 million bags.

Reporting by Paul Bartholomew, Andreas Franke, Paul Hickin, Fabio Reale, Robert Perkins and Marco Perkins. Edited by Emma Slawinski.

(Corrects chart: "HRC margin vs iron ore price")