13 Jun 2018 | 20:30 UTC — Insight Blog

How much more metallurgical coal can China buy from the US?

By Jeffery Lu

The metallurgical coal market has been abuzz with chatter since reports last week of a $70 billion package proposed by China to narrow its significant trade deficit with the US.

Among the range of energy, agricultural and manufactured products that China may look to significantly increase purchases of, coal is one that has been identified by both sides. However, there is a lot of uncertainty over how much China can further deepen its collaboration with the US in the coal sector.

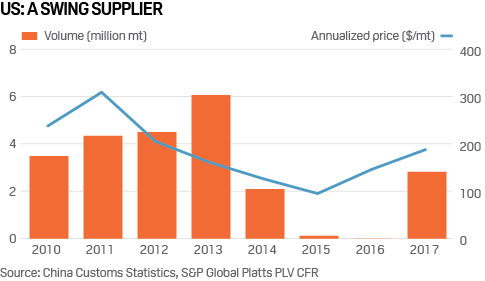

The US is the world's second-largest exporter of seaborne coking coal. However, it is a swing supplier, tending to export only when prices are high.

Looking at US-China coking coal trade flows in the last few years, volumes have demonstrated significant variances, largely led by spot prices (see chart below). Based on Chinese customs data, US met coal exports for HCC and Premium HCC to China were 2.08 million mt in 2014, but plunged to zero in 2016, as annualized S&P Global Platts Premium Low Vol CFR China benchmark spot prices took a dive from $126/mt in 2014 to $95/mt in 2015 before recovering late in 2016.

Volumes hit 2.82 million mt in 2017, when prices averaged a relatively high $188/mt CFR China. In 2018 to date, 1.48 million mt of US spot met coals have been traded to the Chinese market, according to Chinese custom data. Of this, US premium hard coking coal accounted for 32% of the traded volume, with the balance hard coking coal, according to S&P Global Platts data.

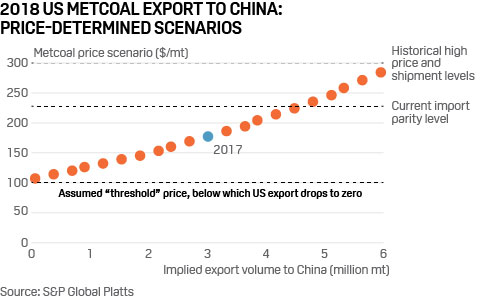

It is in our view that met coal prices and export volumes to China have a positive correlation. The chart below assumes various trade flow scenarios determined by price. It is estimated that for every 5% increase in price, there will be a 10% corresponding increase in met coal shipments from the US to China.

Using 2017 as a benchmark, when China imported a total 2.8 million mt of met coal for an average price for PLV CFR China at $175/mt, this can be translated to two extra, 130,000 mt baby Capesize cargoes for 2018, should prices increase by 5% year on year.

In the best-case price scenario we are looking at a potential export of 6 million mt to China, or 22 more cargoes than in 2017, which was the highest seen in 2013.

To make this happen for 2018, the coal price will need to reach a high of near $300/mt, which seems unlikely given that the import parity was around $230/mt as of June 8, based on the weekly average of the Platts Shanxi Premium Low Vol CFR China equivalent, a domestic premium met coal equivalent marker.

One of the options to lower the bar for the US met coal into China could be relief on import tariffs, which are currently 3% on US coking coal. This compares to duty-free import from Australia, China's largest coal supplier, on top of a much longer voyage time and also higher freight cost.

In the unlikely event of prices tumbling below $100/mt CFR China, we expect a sharp fall in the shipments, possibly to zero, as was the case in 2016. The likelihood of spot prices falling to around or even below $100/mt is fairly low for the near to medium term, however, given the recent supply uncertainties in Australia and Mongolia.

Overall, whether or not the US and China trade flow in met coal does increase remains to be seen. From where we stand today, it seems more political than impactful for two main reasons. First, there are chatters that by potentially boosting Chinese imports of US coal, Beijing is targeting states like Pennsylvania and West Virginia that are key to the US midterm elections.

Second, the impact is estimated to be minor to reduce the overall trade deficit. The US demands to reduce its trade deficit with China by $200 billion, and Beijing’s offer to purchase nearly $70 billion in additional US exports remains short of that target. It is calculated that, at today’s price, our best-case price scenario above of 6 million mt trade of met coal will be translated into an implied value of $1 billion, which appears to be a minor contribution of just 0.5% of the total trade deficit.

Until then, all eyes will be on June 15 when the White House is expected to release the final list of tariffs on $50 billion in imports from China.