07 Mar 2016 | 22:51 UTC — Insight Blog

Ferrous supply chain reeling amid unprecedented hike in steel, iron ore prices

The ferrous supply chain reeled March 7 amid a precipitous and unprecedented climb in steel and iron ore prices.

Platts 62% Fe IODEX jumped a whopping $10.70/dry mt (or 20%), its largest daily hike ever, to reach $64.20/mt.

Myriad factors were cited as upward drivers of the iron ore market – from pre-construction season restocking, to a flower show in Beijing; to government stimulus (or potential stimulus) after the National People’s Congress, where a gross domestic product target of 6.5-7% was tabled.

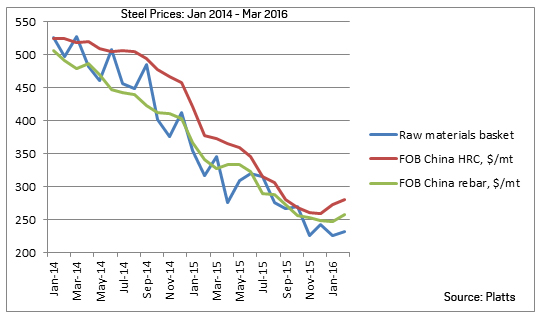

One obvious driver of iron ore was the steel market. Steel price gains have been hugely outstripping iron ore of late.

And steel continued its incredibly bullish rush over the weekend. Fundamentally, it is unlikely much changed in China between March 4 and March 7, but spot prices of square billet had surged over $50/mt by March 7 – yes, $50/mt.

Spot rebar prices moved up $19/mt over the same period, to $305/mt FOB on an actual weight basis, while FOB hot rolled coil prices charged up $17.50/mt from March 4 to reach $330/mt.

In my time with Platts (I joined midway through 2008) I have never seen such daily gains. The European and US steelmakers that bemoan China’s economic slowdown and subsequent exports must be bewildered, while also celebrating the uptick.

Prices do not rise like this in a normal steel market. And the macroeconomic backdrop to all of this makes the latest increases even more peculiar.

At the People’s Congress in Beijing over the weekend, Xu Shaoshi, head of China’s powerful National Development & Reform Commission, downplayed talk of China’s economic issues.

"I can reassure everyone that China will definitely not be having a ‘hard landing’. Such predictions are just hollow talk," Shaoshi said.

Perhaps this alleviated fears to an extent. But as the rally subsides and time passes, however, I think it may be seen as akin to the vote of confidence the football manager teetering on the edge of unemployment gets from his board.

Capital outflows lessened in February, which perhaps alleviated some fears over the world’s second largest economy and the strength of its currency. But capital controls stemmed the tide, rather than any upturn in sentiment.

While steel market sentiment appears hugely strong, levels of Chinese provincial and corporate debt remain massively elevated and growth cannot continue to be predicated on credit. Right?