17 Sep 2019 | 12:38 UTC — Insight Blog

LNG sector transformation underway as long-term contracts dwindle

By Chinmayee Atre and Eric Yep

Global LNG procurement trends are undoubtedly shifting toward shorter contracts with smaller volumes and increasingly flexible commercial terms.

With many long-term supply contracts set to roll off in the coming years, renewals are likely to be for shorter timeframes.

The traditional 15-20 year agreements that underpin LNG projects will be much harder to come by, and only long-term contracts by large core suppliers such as Qatar will continue to form the backbone of global LNG supply.

The contours of long-term contracting activity will also change, with sellers capitulating on most major contractual conditions like destination flexibility, resale rights, price indexation, take-or-pay clauses, and volume flexibility.

On the supply side, new liquefaction capacity and offtake is also shifting towards portfolio players with deep pockets, including oil majors and trading houses, which means that a large number of project sponsors no longer need long-term contracts to obtain project finance.

For buyers, a supply-driven market will further reduce appetite for long-term contracting, at a time when demand projections are constrained by market uncertainties, the emergence of competitive fuel sources and geopolitics.

With the primary drivers behind long-term LNG contracts eliminated – financing for projects and security of supply for consumers – the need for long-term contracting in the future is significantly diminished.

The future LNG market “will be a mix of short-term/spot contracts, 5-10 year deals with a few 20-year contracts, along with portfolio player projects with no contracts aside from the equity partners themselves,” said Jonathan Stern, Distinguished Research Fellow and founder of the Natural Gas Research Program at the Oxford Institute for Energy Studies.

Stern said it would be difficult to find contracts that are not volume-flexible with market-related prices. Producers, he said, would need to adapt to market requirements and find ways to trade price differentials between markets, while the relevance of intermediaries will depend on their ability to create value by taking risks.

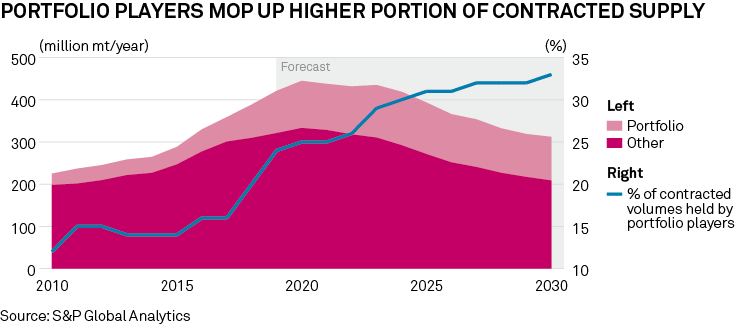

Portfolio players and project equity holders are expected to control more volumes than consumers, with their share growing to 31% in 2025 from 24% in 2019, according to S&P Global Platts Analytics.

Post-2020 will see more LNG production capacity fall under the control of portfolio players and oil majors, but any increase in bargaining power will be offset by the sheer volume of competitive supply that becomes available.

The decline of long-term contracting can also be interpreted as a step toward the commoditization of LNG, as project sponsors invest in liquefaction with the confidence that LNG demand will evolve sufficiently to absorb incremental production.

Contract expiry

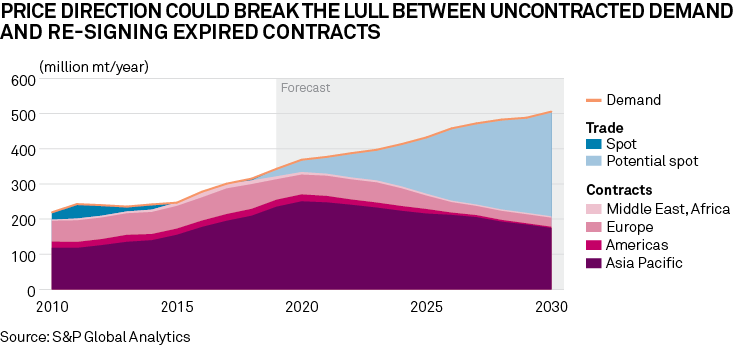

Apart from new LNG demand, significant volumes of old long-term contracts are expiring in the coming years. These are likely to be renewed as smaller deals. In Japan, the single-largest LNG importer with over 26% of total global LNG trade in 2018, utilities expect around 7 million mt/year of contracts with Qatar to expire by December 2021, making it the single biggest tranche of contract renewals coming up.

But Japanese utilities are unsure about maintaining long-term contracts because of uncertainties in LNG supply and demand.

The utilities have expressed a preference for shorter terms, lower volume and better procurement terms including some short-term and spot contracts to manage demand fluctuation.

For example, JERA secured a three-year, 2.5 million mt/year contract with Malaysia’s Petronas from 2018, when its 15-year 4.8 million mt/year contract was renewed. It also replaced a 25-year, 4.3 million mt/year contract with the UAE’s ADNOC with a three-year deal for 0.5 million mt/year from 2019.

China, the world’s second-biggest LNG importer, accounted for the bulk of Asian LNG import growth in 2018 by adding 15.8 million mt of new imports, 41% higher than 2017 and almost entirely from the spot and short-term market. Nearly 40% of existing Chinese demand remains uncontracted, and this is growing every year. The main drivers are low spot prices, the pending startup of the Power of Siberia pipeline from Russia in December 2019 and the trade dispute with Washington that limits its long-term procurement from the US.

Even new LNG importers in south Asia – Pakistan and Bangladesh – have grown increasingly cautious of their oil-linked long-term purchase strategies, given uncertain demand, the high relative cost of LNG as a fuel source, and the growing risks associated with pricing LNG against oil.

There are concerns about projections of a tighter market in the 2020-2023 timeframe, but even that does not necessitate a long 20-year supply deal.

Until structural uncertainties in Asia’s LNG demand are resolved, and as long as buyers take comfort in a supply driven market, the pace of long-term contracting will remain constrained well into the 2020s.

This article appeared in the S&P Global Platts special report on LNG markets, "New Sustainable1". Read the full report.