09 Sep 2019 | 21:14 UTC — Insight Blog

Japan’s nuclear power generation ramps up in 2019 but hurdles lie ahead

By Bruno Brunetti and Andre Lambine

Dynamics in the Japanese power market have been a major bearish force acting on the global LNG market this year. Weak power demand, increasing renewable generation, notably solar, and higher nuclear output have depressed fossil fuel needs, and LNG in particular, as S&P Global Platts Analytics highlighted in a recent report. Ahead of the Platts Analytics Client Seminar in Singapore, Bruno Brunetti and Andre Lambine explore key aspects of the Japanese power market.

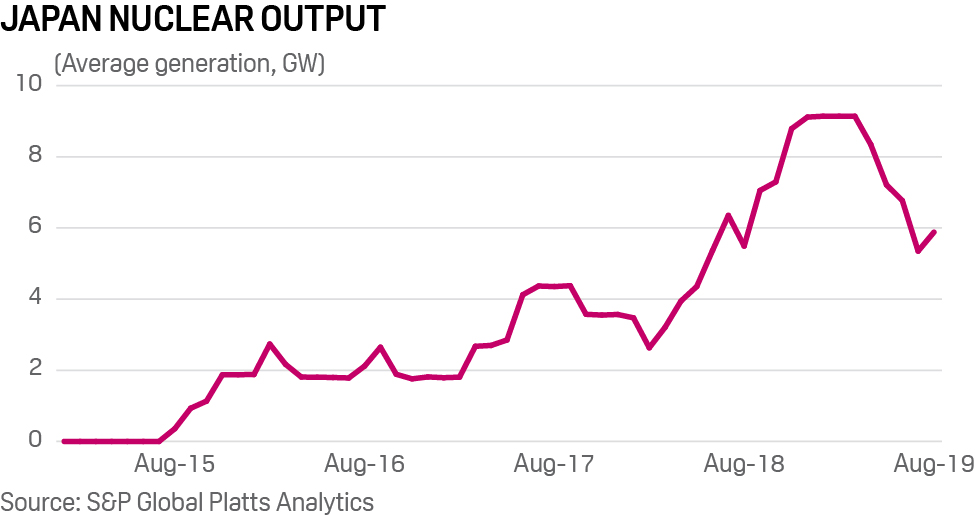

Japan’s nuclear generation in the first half of 2019 was over 8.2 GW on average, against only 3.9 GW in H1 2018, as five reactors were restarted last year.

But routine maintenance and refueling has pushed output lower year on year during July and will continue to undermine output for the balance of the year.

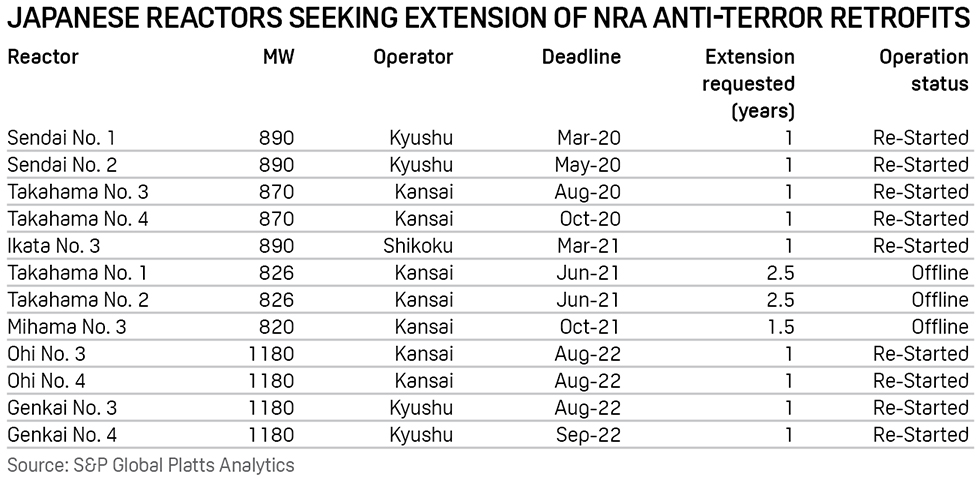

In addition, new uncertainties have emerged concerning nuclear output down the road. The operators of the various nuclear plants have been tasked by the Nuclear Regulation Authority (NRA), to “terror-proof” their facilities, but they have warned that they could miss the deadlines for the completion of the work.

The first deadline is set for March 2020, with four reactors facing a deadline for each of the next three years. In April, the NRA warned that if the utilities miss the deadlines, they will have to shut their nuclear units.

Click to enlarge

Although the NRA reasserted again in a recent order that if the work is not completed one week before the deadline, operation of the reactor could be suspended, the NRA also indicated that the operators would have a chance to explain the situation six weeks before the deadline.

Platts Analytics believes this move could mean the NRA may adopt a somewhat softer stance, especially if the operators of the plants effectively manage to convince the regulator that the delay was tied to reasonable causes.

Solar and coal capacity grow

More broadly, Japan shows a number of changes in its power mix. Remember that Japan has been leading the way in terms of solar PV deployment globally, with over 10-13 GW/year installed in the aftermath of Fukushima, but the progressive reduction in policy support for solar PV has translated into a slowdown in solar capacity additions to about 5 GW/year.

Coal capacity has also been increasing. On June 1, Kyushu Electric started trials at its newest coal plant, Matsuura unit 2 with 1 GW capacity, and plans to reach commercial operations by the end of the year. In addition, a 600 MW block at Noshiro has started trial operation on August 1, with additional 1.8 GW of coal capacity also expected to come online in 2020. Gas capacity is also increasing, but to a lesser extent than coal, as only 1.2 GW is due online by 2020.

Meanwhile, power demand has been fairly weak. Demand in 2018 was down 5 TWh year on year, and data so far this year shows a worsening picture, with a 3.6% decrease in 2019 to date versus 2018, and declines will continue further into 2020. Consequently, the country’s thermal gap is shrinking.

Long-term contracts limit switching

The weakness in Japan’s fossil fuel needs this year has also contributed to lower LNG prices. Spot LNG prices have declined and become more competitive with coal, moving closer to the contracted price for coal negotiated between Tohoku Electric and Glencore for the fiscal year starting in April.

This price functions as an accepted rate also for the majority of the other Japanese utilities. The price is effectively set for six months at a time, and has not benefited from the decline in spot coal prices over the last few months. However, Japanese power utilities traditionally purchase the majority of their coal and gas requirements on a long-term basis, with spot transactions accounting for around 20%, effectively limiting the flexibility to switch large amounts of fuel.

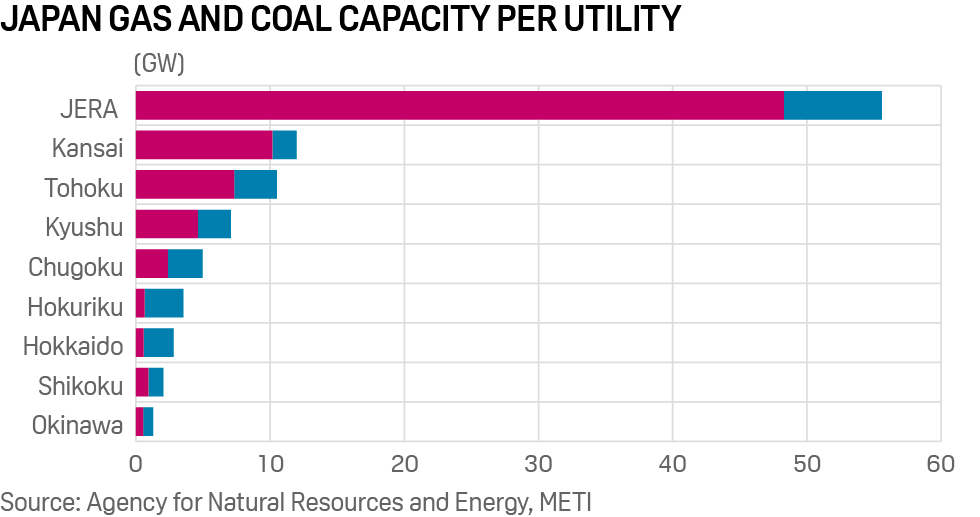

Nine large utility companies dominate the power sector in Japan. Platts Analytics has looked at the available capacities of all the power generators and found that only JERA and Kansai Electric may be able to facilitate a switch across the entire year. Both firms have gas-fired power capacity that they do not use – JERA: 22 GW, Kansai Electric: 4.4 GW – so from a pure capacity point of view, they could turn down their coal-fired capacity, and use their gas plants instead.

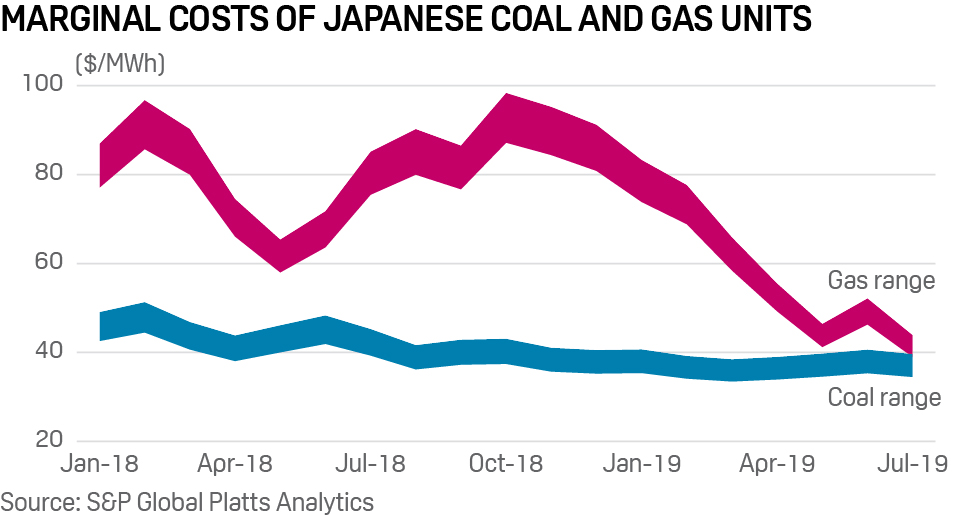

However, our analysis shows that the spare gas capacity has efficiency of 40% and lower, making it more difficult to switch, from an economic perspective. Overall, even if spot prices and available capacity could allow for switching, inflexible coal and gas contracts that tend to be long-term in nature have been limiting coal-to-gas switching opportunities in the near future, and therefore the power generators’ ability to capitalize on low-priced LNG spot cargos.