06 May 2016 | 10:31 UTC — Insight Blog

The multifaceted metamorphosis ahead for Mexico's energy markets

The Mexico energy market has been a hot topic ever since late 2013 when the government decided to liberalize the energy sector, opening it up to foreign investment.

The reform provides an unprecedented opportunity for international companies to participate in development of the nation’s vast oil resources as PEMEX unwinds its current monopoly. Multiple other opportunities exist in the power sector, in renewables development and in the natural gas pipeline sector.

The energy reforms were largely a result of the steep decline of the country’s oil production, inadequate financial resources to turn production around and an inability of PEMEX to keep pace with the technological change taking place in the industry.

Mexico ranks sixth in the world for non-conventional oil and gas resources, right behind Canada and Algeria, but lacks the financial resources to develop its reserves. It would take US$20 billion to extract the country’s reserves over a 210-year period and $87 billion to do it in 50 years. It also would not be possible to do this with one state-owned exploration and production monopoly — this is why the reforms were necessary.

However, private investment cannot come quickly enough. Active drilling rigs in Mexico fell to 43 in February, down 43% from a year prior. Developmental rigs fell to 35 in February, down 44% from February 2015. The biggest year-on-year declines came from the Southern Region (down 15.7 rigs; 52%) and the Southwestern Marine Region (down 12.4 rigs; 56%).

In March, Pemex’s announced a $5.5 billion budget cut, and active rigs plummeted another 43%, while developmental rigs dropped to only 21. The Southern region again was hit hardest, with developmental rigs falling to seven during the month, down 55% from January.

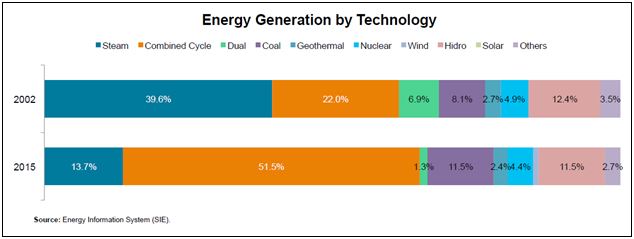

Petroleum production is a major concern for the country, but renewables also are an important focus of the reforms. On top of having significantly large oil and gas resources, Mexico also has significant resources for renewable energy such as geothermal, wind and solar. It is estimated that current renewables generation, plus proven additional renewable resources in the country, could boost generation from renewables from 3.9% of the country’s total power generation to 9.89%.

Adding possible renewable resources to the mix could satisfy the country’s total generation needs, according to Mario Gabriel Budebo, director general of the EXI Fund: Energy and Infrastructure and former independent director of gas and basic petrochemicals at PEMEX. Budebo, who was the keynote speaker at the Platts Global Power Conference in Las Vegas in early April, also noted that significant infrastructure would need to be built to support such a major turn to renewables, highlighting the significant need for private investment to support the renewables efforts. He also gave a firsthand account of the Mexican energy landscape and the other investment opportunities the reform provides for international companies.

Investment in pipeline infrastructure also is a major need throughout the country. Just a few years ago, only 10 states had natural gas pipelines, but today 22 states have them. The Ministry of Energy estimates US$10.1 billion needs to be invested in pipeline infrastructure between 2015 and 2019 to build 3,205 miles of new pipeline, which would increase the total pipeline network to 11,081 miles.

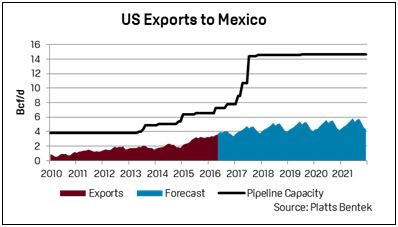

Platts Analytics expects that US natural gas exports to Mexico could break above 4 Bcf/d by early summer as demand picks up and domestic supply continues to decline due to a lack of drilling activity.

Power demand is expected to increase as the country transitions to greater reliance on gas-fired generation and retires as much as 2.1 GW of fuel oil-generation plants over the next year.

However, lingering gas pipeline transportation constraints on both the north-to-south corridors (Los Ramones Phase II South) and the east-to-west corridors (El Enino – Topolobampo), may hinder exports this summer if planned pipeline expansions miss their expected in-service dates, in which case Mexico would likely increase reliance on LNG imports.

Mexico’s energy infrastructure development is behind other emerging economies, creating significant investment opportunities for both domestic and foreign companies.