21 Dec 2020 | 14:01 UTC — Insight Blog

Commodity Tracker: 5 charts to watch in 2021

Where are the bright spots and risk areas for commodities in the coming year? In our final Tracker of 2020, S&P Global Platts editors and analysts round up some of the biggest trends, from oil supply and demand to China's resilient steel sector, as well as the outlook for global LNG and container freight markets.

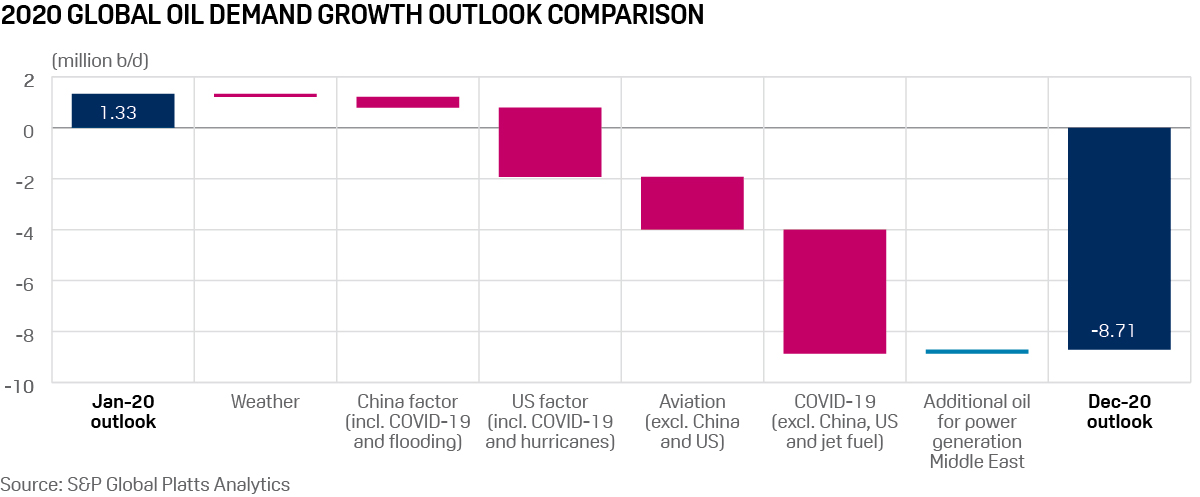

1. Rebounding oil demand in 2021 will still fall short of 2019 levels

What's happening? Looking back at 2020, S&P Global Platts Anlaytics' expectation for oil demand growth swung over 10 million b/d, from growth of 1.3 million b/d pre-coronavirus, to the latest estimate of an 8.7 million b/d decline. On an annual basis, a small portion was attributable to warm winter weather, though during the heart of the heating season the impact was significantly greater. The dominant driver was COVID-19 demand destruction, with declines in the US and from the aviation sector, in particular, taking out large chunks of global demand.

What's next? Current forecasts see warmer than normal winter weather in the US and Europe, but colder in Japan, though the outcome still awaits. Demand growth in 2021 is forecast as 6.3 million b/d, but more importantly, demand will still average 2.4 million b/d below 2019 levels. The biggest portion of that gap will be in jet fuel/kerosene (1.6 million b/d), followed by gasoline (645,000 b/d), and then diesel (484,000 b/d). Other products, including LPG, ethane, and naphtha, will show growth above 2019 levels.

Go deeper: S&P Global Platts Analytics 2021 Energy Outlook

2. OPEC provides mixed picture ahead of January's relaxation of quotas

What's happening? With oil prices in freefall earlier this year, the OPEC+ group in April agreed to its deepest-ever production cuts, initially 9.7 million b/d for May and June 2020. The agreement was largely successful in fostering a recovery in oil prices throughout the summer and fall, but oil demand outlooks have again come under pressure, while questions around member compliance with quotas persist. The group reached a compromise agreement December 3 to slightly relax production quotas and to meet monthly to fine-tune output as conditions warrant.

What's next? The forward view continues to change rapidly. OPEC's own analysts painted a gloomy view of the oil market in 2021 mid-December, revising down demand estimates for the first and second quarters. But they simultaneously suggested room for more aggressive increases in production in the coming months. Meanwhile, the behavior of individual producers will remain a focal point, with Libyan oil volumes having risen rapidly to reach an estimated 1.1 million b/d, while Iraq, in the midst of an economic crisis and heavily dependent on oil revenues, "owes" almost 600,000 b/d in compensation cuts for quota violations since May, according to S&P Global Platts calculations. The OPEC+ alliance will next meet Jan. 4.

Watch S&P Global Platts Market Movers: Asia - Europe

3. China steel output strength could fuel higher exports

What's happening? The strength of Chinese crude steel production in 2020 took everyone by surprise – particularly in a year impacted by the pandemic. At the start of the year, S&P Global Platts expected steel output to grow around 2% on last year but the final tally will be closer to 6%. Looser credit conditions in China incentivized mills to keep output high and helped offset any decline in downstream demand due to the lockdown and lack of export opportunities. China's steel exports were uncompetitive because domestic prices were far higher than in other markets, while demand in other countries collapsed. As such, the country's export will likely be around 54 million mt this year, down from 75 million mt in 2019.

What's next? At this stage, Platts expects China's crude steel production in 2021 to be up around 2% to 1.07 billion mt. China always has the ability to surprise on the upside but tighter credit conditions will likely slow the rate of growth in property construction, while the manufacturing recovery may run out of steam in the second half of the year. Given China's steel capacity expansion in recent years, production will remain strong, so mills will probably need to lift their exports if domestic consumption is softer. Finished steel exports in 2021 are likely to be closer to the levels seen in 2019 rather than in 2020.

4. Global LNG market eyes positive demand signals as Asian imports hold up

What's happening? LNG trade in 2020 has shown resilience, and after Platts JKM hit sub-$2/MMBtu lows in May, the benchmark has not only recovered but rallied. This has been down to an unprecedented supply-side response, with US LNG cancellations starting to rebalance the market through the summer, followed by strong winter buying demand from Asian buyers in the fall and a number of supply-side issues boosting prices.

What's next? The recent highs of $12/MMBtu are likely to prompt emerging Asian buyers to reassess their procurement strategies, and trigger a fresh round of negotiations with producers. Some LNG supply projects that failed to clear FID in 2020 due to the pandemic could finally see the light of day in 2021, while small-scale and bunkering demand for LNG will continue to emerge. Big suppliers like Qatar and the US will intensify efforts to capture the Asian market, where demand growth will be underpinned by India and China, with key policy frameworks taking shape to build downstream markets. Countries like Vietnam, Philippines and Myanmar are expected to make significant moves towards new regasification in 2021 and gas market liberalization over much of Asia Pacific will accelerate.

5. Persistent tightness in container markets to keep prices elevated

What's happening? Container prices in Asia surged to record highs in December 2020 as demand grew with the easing of coronavirus restrictions, while supply kept declining. Carriers are deploying higher capacity on the trans-Pacific route due to lucrative returns, worsening the shortage in other regions, while empty containers are getting stuck on the way back due to challenges in transportation and port operations. The leasing market in China is out of stock, with factories unable to churn out vessels fast enough to match demand.

What's next? Prices may remain elevated, if not at record levels, at least through the first quarter of 2021 as demand is expected to grow till the Chinese New Year. The supply situation may even get worse in the first two months of the year as major shipping liners have suspended their services in China due to a halt in coastal feeder services amid stringent quarantine norms.

Reporting and analysis by Alan Struth, Kang Wu, Herman Wang, Dania Saadi, Paul Bartholomew, Parisha Tyagi, Stuart Elliott