29 Nov 2016 | 19:11 UTC — Insight Blog

Oil demand and electric cars: A disjointed dilemma

With the automotive industry tipped as ripe for disruption and a growing imperative to rein in climate change, the recent rise of electric cars has sparked both excitement and angst of late within the global energy industry.

Tougher emissions regulations, falling battery costs, and breakneck advances in networked technology means affordable alternative to conventional vehicles are on the verge of a mainstream breakthrough.

Once a critical tipping point is reached -- so the narrative goes -- mass market adoption of electric transport will trigger an abrupt and painful end to the hydrocarbon age, taking with it the fortunes of oil producers.

In reality, the future of electric cars and their impact on oil demand remains far from clear. Forecasts of their market penetration vary widely and require substantial guesses on oil prices, further efficiency in existing motors, and government policies.

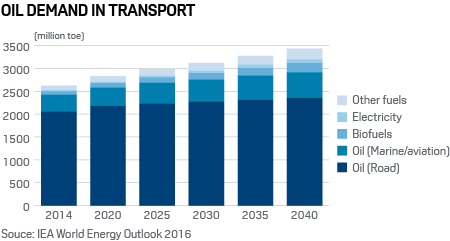

One thing that is clear is the potential scale of the disruption for the oil industry. More than 90% of the world’s road transport fleet continues to run on oil products and the sector accounts for over 40% of total oil demand.

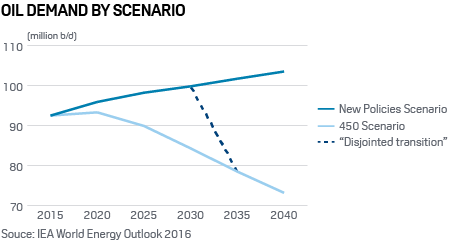

So how painful could a radical, faster than expected transition away from oil be for the industry? Last week the International Energy Agency took a stab at answering that question for the first time.

According to a "disjointed transition" scenario in its industry touchstone World Energy Outlook, the answer is potentially "massive".

Oil demand could collapse by 16.4 million b/d and producers would face "major losses" with $380 billion of above-ground investment written off, the IEA believes, if the oil industry is caught off guard by a surge in green energy use from 2030.

The 'disjointed' scenario assumes that, prior to 2030, operators invest on the assumption that prices and demand will continue to rise under its central scenario. But, given the sharply diverging outlooks for oil demand in its central and low-carbon scenarios, the IEA warns that risks to the industry are even greater the longer it waits to readjust to a lower carbon world.

Predictably, oil producers themselves are more sanguine over their long-term business prospects. They note, correctly, that oil and gas will still play a major role in the global energy mix for decades to come. Pressed on the future potential for large-scale stranded assets that may become too costly or dirty to produce, they point to average industry reserve life ratios of little more than a decade and the fact that more reserves are needed to replace output from mature fields. Indeed, at current rates, the world is losing 5 million b/d a year of oil supply from fields in decline.

It may be a back-of-the-envelope guesstimate but the very fact that the IEA has modelled such a traumatic oil demand scenario is a telling sign. At the very least it is a nod of recognition that concerns over the potential for major oil industry upheaval due to falling demand in transport are taking root.

Overall, however, the IEA is more conservative than most on the likely and potential impact of electric cars on global oil demand. Its central energy scenario assumes an additional 1 million b/d of oil demand is displaced by electric cars in 2040 up from 300,000 b/d last year. That figure rises to 6 million b/d under its lower carbon demand scenario but that is less than half of the more alarming 13 million b/d prediction by Bloomberg New Energy Finance which grabbed headlines earlier this year.

Much of the difference comes down to judgment calls on the future costs of storing electric power.

EV battery prices have not only plummeted by more 65% since 2010 but the fall has consistently outpaced most previous projections. This progress on bringing down costs and improving capacity -- so the logic goes -- and will continue to surprise to the upside.

The IEA is more cautious here also. It believes the math over when EVs become competitive with conventional cars based on their battery costs is too simplistic.

Even if EV battery costs more than halve by 2040, and conventional cars continue to become more fuel efficient, the higher cost of EV's and home charging equipment will negate their cost advantage, it claims. As a result, payback times for the extra outlay on EV cars are still "well above the two-to-three-years that a consumer would typically tolerate" even by 2040.

Oil prices are also a key factor influencing the adoption of EVs over internal combustion engines. A lower price outlook shifts the cost competitiveness advantage towards conventional oil-fueled engines, which continue to improve on fuel efficiency.

As such, the current "lower for longer" industry mantra on future oil prices may prove a silver lining for oil companies staring into an increasingly blurry crystal ball on demand for their oil.