13 Nov 2017 | 09:31 UTC — Insight Blog

Cartel power: China and the Russian-Saudi axis - Fuel for Thought

Ever closer relations between Saudi Arabia and Russia, the world’s two largest oil exporters, look like a nightmare for China, the world’s largest oil importer. However, as the originator of demand in a world where peak oil consumption hovers on the horizon, it is Beijing that ultimately holds the whip hand.

In the short term, China, unlike the US, does not have a thriving shale oil industry to fall back on, which can ride the price coattails of OPEC/non-OPEC output restraint.

Yet US shale takes the heat out of a potentially under-invested oil market. It provides a breathing space—of uncertain duration—in which China can address its fundamental problem, which is not the re-emergence of cartel power in the oil market, but its own dependence on imported oil.

Despite differences over Middle Eastern policies, Moscow and Riyadh have found common ground as the principal architects of the OPEC/non-OPEC deal to curb production and rebalance supply and demand in the oil market.

Russia delivers the non-OPEC producers, while OPEC would not act cohesively without the knowledge that Saudi Arabia will bear the lion’s share of OPEC’s commitment. Between them, Moscow and Riyadh are committed to 40% of the total reductions.

While Russia is no stranger to military ventures abroad, active Russian-Saudi cooperation is a major departure. It is the product of Riyadh’s former market share strategy. Saudi Arabia’s refusal to be the world’s swing producer between November 2014 and November 2016 saw crude prices plummet and a gaping hole emerge in the Russian budget.

There were only two ways out: continuation to the bottom in which only the lowest-cost producers survived, or the re-creation of cartel power. Russia’s overwhelming dependence on oil revenues proved its Achilles Heel, but it coupled this capitulation with a show of strength in Syria, bringing together two countries which together in September were supplying 28.7% of China’s oil imports.

Competitive market

US shale has upended expectations in more ways than were imagined. Pre-shale, the world was going to be a fierce competitive battle for scarce resources, principally hydrocarbons, and principally between China and the US. Post-shale, it is China that is left looking vulnerable as Moscow and Riyadh cozy up, but only from an oil-centric world view.

Beijing has gradually been extending its influence through Southeast Asia and Africa using soft power instead of military might in pursuit of both access to natural resources and markets for the products of its heavy industry. This, Beijing hopes, will secure its energy supplies and temper the slowdown in its domestic economy.

The emergence of cooperation and competition for Chinese oil demand between Russia and Saudi Arabia comes as China embarks on a ‘new era’ outlined by President Xi Jinping at the Chinese Communist Party’s 19th five-yearly Congress, in which his doctrine was enshrined in the country’s constitution.

But while Xi Jinpeng’s doctrine sees China becoming a global military power, the near-term emphasis is on economic strength and prosperity. China’s army will only complete ‘modernization’ by 2035, and Xi Jinping’s speech was more directly supportive of open trade and the international order than his predecessor Hu Jintao. Beijing looks more likely to exert its power through the existing structures of global governance as it has benefitted hugely in economic terms from the existing world order.

As a result, China’s position vis-à-vis a Moscow-Riyadh axis is one of strength.

While they may cooperate, Russia and Saudi Arabia must also compete to secure Chinese market share.

China, for its part, can use the window of opportunity provided by US shale to leverage its own market power as a consumer, both to exert control over international oil supply chains through cooperation, and to address the real weakness in its relations with oil producers – its dependence on imported oil.

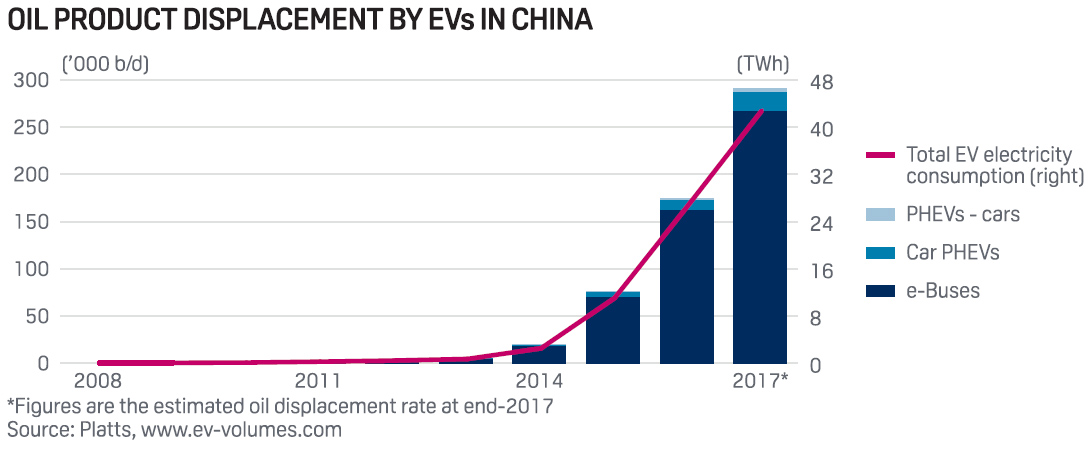

In his speech to Congress, Xi Jinping said that China had become a driving force in the fight against climate change, and it has. China has more electric vehicles on the road than any other country in the world and produces more solar panels.

It must address both domestic air pollution and maintain its manufactured exports, while increasing domestic demand. It can leverage its huge manufacturing capacities to achieve these goals at the same time that transport electrification reduces its dependence on imported oil. Green technologies are first about innovation, but then about producing widgets, which is what China does best.

It is a strategy based on economic and cultural interaction rather than the projection of military power; and one that is likely to get the better of any oil cartel, whose members will continually be divided by the potential benefits of cooperation versus competition.