21 Aug 2019 | 19:35 UTC — Insight Blog

New US oil pipelines cause shift in regional price dynamics

The second new crude pipeline in as many weeks has started moving oil from West Texas to the US Gulf Coast, adding to the pool of available light sweet in the region and squeezing the price spread between the two locations.

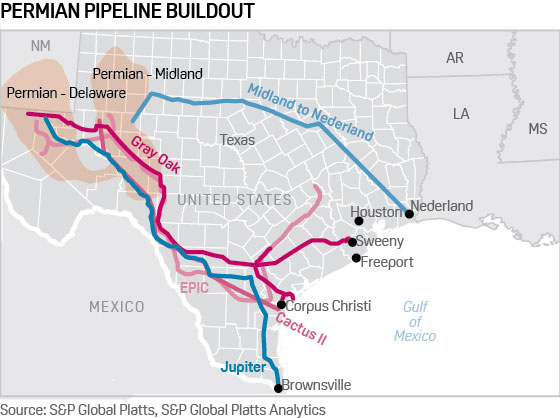

EPIC Crude Holdings said August 19 that its 24-inch-diameter EPIC interim crude line has begun delivering crude from the Permian Basin to various terminals in Corpus Christi and Ingleside, Texas. The line has the capacity to deliver up to 400,000 b/d and is expected to gradually ramp up to that nameplate capacity over time.

At the same time, construction of EPIC's 30-inch-diameter permanent crude line is about half-way complete and is expected to start up in January 2020. The permanent crude oil pipeline will have an initial capacity of 600,000 b/d, with throughput anticipated to begin ramping up during the first quarter of 2020.

EPIC joins Cactus II on the list of newly-opened pipelines that are bringing more West Texas crude to the Coast. Cactus II, which began flowing the week of August 12, has the capacity to move up to 670,000 b/d to the Corpus Christi area. Additionally, the 900,000 b/d Gray Oak pipeline is expected to start up by the end of 2019, adding to greatly expanded takeaway capacity out of the Permian.

Given the added pipelines, the Permian will have sufficient takeaway capacity through 2020, according S&P Global Platts Analytics. The new wave of crude is helping alleviate a year-long bottleneck in the Permian Basin, where prices are mostly strengthening. However, the debottlenecking is adding to the supply on the Gulf Coast and adding downward pressure to pricing there.

Spreads tighten

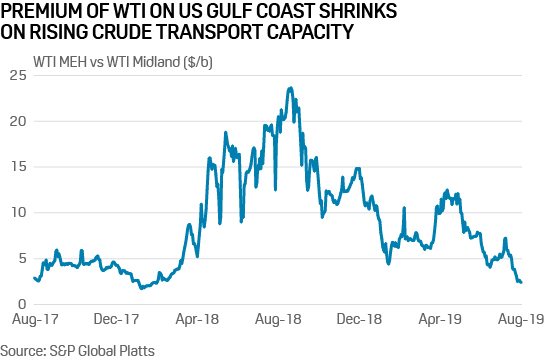

WTI at the Magellan East Houston terminal has been particularly weak during August, with the average differential to date at WTI plus $3.28/b. That is about $2.60/b lower than the year-to-date average for the grade at WTI plus $5.91/b, according to S&P Global Platts data. Prices of WTI-based crude have felt the pressure as the spread between global benchmarks Brent and WTI has dropped, falling under $4/b, after peaking at over $11/b in late May.

The weakness of WTI on the Gulf Coast has created a significantly tighter spread between WTI crude in Houston and WTI in Midland, Texas. Currently, the $2.40/b spread between Midland and MEH is the narrowest since February 15, 2018, when the spread was at $2.30/b. Moreover, the average spread for August 2019, which is $3.43/b, is less than half the year-to-date average of $7.43/b, and nearly six times less than the August 2018 average of $19.89/b, according to Platts data.

Prices for WTI crude in Midland were heard trading weaker on the day August 19 after trading steadily at a premium to WTI cash the previous week. WTI in Midland was heard trading at a 5 cents/b premium to WTI cash in Cushing the morning of August 19. That was weaker than where it was last heard trading the previous session, at WTI plus 40 cents/b. Sources were not sure what was contributing to the weakness on the same day that EPIC announced that it was flowing. One trader said initial flows off the line likely were not as strong as expected.

Go deeper - WTI: What's in a name?

As for WTI MEH, the grade continued to weaken Monday and was heard trading in the afternoon at WTI plus $2.50, 30 cents/b lower than where it was assessed Friday.

The added takeaway capacity in the Permian likely will be welcomed by many West Texas producers that have seen their storage levels balloon as US production has climbed.

In the last year, West Texas inventory levels have shot up by over 6 million barrels, from just over 14.3 million barrels in the four-week moving average for the week of August 13, 2018, to nearly 20.5 million barrels in the four-week moving average for the week of August 12 2019, according to inventory data from Kpler, a data intelligence firm. As production growth begins to slow and takeaway capacity is expanded, it is expect that inventory levels will be alleviated.

The new pipelines are also expected to cause West Texas crude shipments to Cushing, Oklahoma, to fall while greatly increasing flows to the USGC. Platts Analytics forecasts flows between the Permian and the USGC to increase by around 1.75 million b/d between 2H 2019 and the end of 2020.

During the same period, shipments to Cushing are slated to decrease by nearly 350,000 b/d. This increase of flows to the Gulf could have the effect of tightening the spread not only between Midland and the Gulf, but between Cushing and the Gulf as well.