21 Aug 2017 | 10:36 UTC — Insight Blog

Contract volatility reins in US land rig day rate growth: Fuel for Thought

By Bob Williams

“Tapping the brakes” is as good a description of what’s happening in US land drilling activity today as any, and it applies to drilling costs as well.

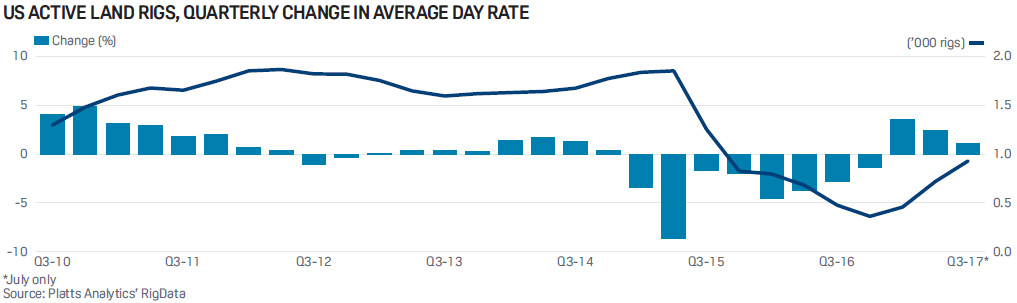

Since the recovery in drilling activity began to really gather steam last December, the US active land rig count, as monitored by Platts RigData’s RADAR report, had added at least 40 rigs to each successive month’s average tally through May.

Correspondingly, there was a comparable run-up in rig day rates (the daily cost to hire a rig with a full crew). The turnaround in day rates began somewhat modestly, if unexpectedly, in December. Even with this monthly improvement, however, it wasn’t enough to lift the average day rate for 4Q 2016 out of negative territory, where it had languished for two years.

But Q1 of this year provided the jaw-dropper: a whopping 3.5% increase in the average day rate—the biggest quarter-to-quarter increase in this metric since 4Q 2010.

The driver for much of this surge was a shift in operator-driller negotiations on rig day rates: As operators scrambled to lock in day rates on the spot market before they could escalate further, drillers shifted from offering discounts for longer-term contracts to asking for premiums for same—especially for the preferred Class D (1,500–1,999 hp) rigs that now account for 70% of all US onshore drilling activity.

However, the rapidly accelerating rig count growth raised concerns that operators were adding more rigs than oil and gas prices warranted and that a correction of sorts was in order. And indeed there was a significant retrenchment, as the rate of additions to the active rig fleet was roughly halved in June and again in July.

Now, with the plateauing of rig demand over the past two months, there is a similar pattern of weakening for day rate gains.

While day rates seesawed in the scope of gains through 1H 2017, generally the average month-to-month increase was well above 0.5%; accordingly, the cumulative net gain of 3.5% in Q1 was followed by some deterioration in Q2, to a new cumulative net appreciation for last quarter of 2.4%—still impressive so early in the recovery.

It’s a whole new ballgame in Q3, however, as the overall average rate of increase in July was only 0.2%—the weakest outcome of the recovery. Data from Platts RigData’s Day Rate Report shows that the preferred rig Class D saw the most deterioration, as many drillers abandoned the term-contract premium.

During the latest boom period that ended in 2014, the costs to hire drilling rigs and to man the rig crews inflated rapidly with demand for rigs—especially the preferred rigs purpose built for efficiently developing the tight oil and gas formations that have upended the global energy picture.

Less than three years ago, contract drilling executives were bemoaning the difficulty of hiring enough quality personnel for the rigs, while operating companies scrambled to mitigate rig cost inflation by locking in day rates for the prized high-spec rigs under long-term contracts of three to five year duration.

The consequent surge in US oil and gas production swamped global markets, and commodity prices plummeted.

But after a partial commodity price recovery—especially for oil—US companies ramped up their rig counts and capital spending anew.

RigData's tally of US active rigs rebounded by 166%, even though oil prices remained below $50/b and gas prices below $4/MMBtu, and we began to caution that the rapid run-up in rigs wasn’t warranted by where oil and gas prices had settled.

After declining monthly for two years, rig day rates spiked in Q1 of this year. Now the questions have arisen anew: Will rig cost inflation be held in check? Will drillers be able to staff up again?

The latest Day Rate Report confirms that day rate increases have settled down to more modest sequential monthly gains (most recently, in July, by 0.2%). Labor costs, after increasing by more than 15% this year compared with the 2015 average, are still 2.5% below 2014 levels.

As operators began to slowly ramp up drilling again early this year, in response to more favorable oil prices, most drilling contractors were still offering discounts to operators. But just four to eight weeks later, a number of drillers marketing top-tier rigs started asking for premiums for longer-term contracts—an unprecedented turnabout. At the same time, the frantic scramble for rig personnel slowed to a crawl.

What does that tell us? It appears that operators and drillers are being more sensitive to vagaries in rig markets than ever before. And that skittishness is magnified by rig demand coalescing increasingly around a single rig model—the aforementioned Class D rig equipped with drilling pad mobility and heavily automated.

As rig demand narrows its scope, the market responds more quickly.

Will the sudden fade in term premiums help revive a slowing rig count anew? That’s doubtful, given that 2017 drilling capex is largely a done deal for operators, and especially since so many Class D rigs are still sidelined.

But the main takeaway here is that there is a new volatility in contract terms for the dominant rig class, and so it’s not likely that operators will be surprised again by a sudden inflation in day rates.