12 Aug 2019 | 11:00 UTC — Insight Blog

Commodity Tracker: 5 charts to watch this week

Economic indicators spell potential trouble for oil demand, while US gas producers and exporters are feeling the pressure from oversupply on both the domestic and global markets, S&P Global Platts editors explain in our weekly selection of big commodities trends to watch.

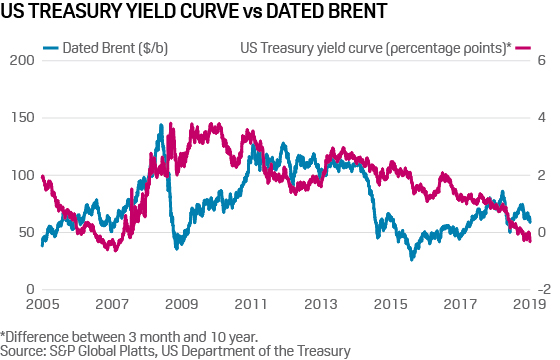

1. US treasury yield curve a warning sign for oil demand

What’s happening? The difference between long-term and short-term interest rates, or the slope of the yield curve, has borne a consistent negative relationship with subsequent real economic activity in the US, with a lead time of about four to six quarters. The last time the yield curve was this low was just before the financial crisis in 2007 when concerns still existed over peak oil supply. Fast forward to 2019 and the pattern between yields and oil prices is similar.

What’s next? The differences between 2007 and 2019 include the fact that the US now exports its crude, and shale has seen overall production head toward 12 million b/d. Indeed, the debate is now around peak demand for oil, while OPEC is struggling to provide a floor to oil prices even with its new found alliance with Russia. With demand weakness and US supply continuing, OPEC has its work cut out.

2. Global LNG oversupply pressures US export economics…

What’s happening? The oversupplied global LNG market has caused prices at premium international hubs in Europe and Asia to weaken considerably in 2019 compared with last year. That has crimped netbacks to export terminals along the Gulf Coast.

What’s next? The trend for low netbacks is expected to continue in the near term as additional US liquefaction trains are brought online. Freeport LNG is preparing to begin production on its first train, while Cheniere is building a third train at its Texas terminal and a sixth train at its Louisiana terminal. Heading into the winter, price spreads suggest US exporters could see a rebound in netbacks, though the trade war with China is still seen as a headwind.

3. … and domestic US gas prices hit new multi-year lows

What’s happening? US daily gas production surpassed the 90 Bcf milestone over the past week, propelled by output gains in the Haynesville and Appalachian shale basins, with a smaller contribution coming from the Permian of West Texas. In the Haynesville, production is up about 300 MMcf/d from July to an average 11.9 Bcf/d this month, data compiled by S&P Global Platts Analytics show.

What’s next? The production gains are weighing on benchmark cash and futures prices, with both indexes falling to fresh multiyear lows last week. On August 5, spot prices at the Henry Hub fell to just $2.025/MMBtu, or their lowest in over 32 months, while the NYMEX prompt-month settlement price also hit a fresh 38-month low for the contract. As gas output continues to rise, prices could come under increasing pressure in the coming weeks as maintenance and commissioning activity pushes back on feedgas demand from LNG exporters, and continued delay of the Sur de Texas-Tuxpan pipeline keeps US exports to Mexico lower than previously anticipated.

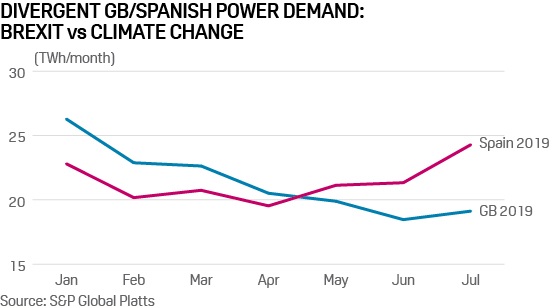

4. Spain’s electricity demand set to overtake UK

What’s happening? Annual power demand in Spain is on track to exceed that in the UK for the first time ever. UK demand has been in steady, structural decline in recent years and 2019 is no exception with demand down over 5 TWh on year. Households and businesses are using less – a combination of more efficient processes and industrial decline not helped by three years of political uncertainty. Spanish demand has been in recovery mode since the 2007 banking crisis, growing 12 TWh/year since 2014 versus a 26 TWh/year decline in the UK, buoyed by summer air conditioning demand as European temperature records tumble.

What’s next? With YTD Spanish demand inching ahead of the UK, it now seems inevitable that Spain will displace the UK as NW Europe’s fourth-largest power market by demand, behind Germany, France and Italy. This has implications for Spain’s brave zero-subsidy renewables drive, which has every chance of thriving given buoyant national demand. And the UK’s interconnection program could see more cheap offshore wind-driven exports to the continent, as UK demand slackens further.

5. Agriculture markets second-guess USDA corn, soybean outlook

What’s happening? The US Department of Agriculture’s World Agricultural Supply and Demand Estimates report is due out August 12, and is eagerly awaited by market participants. The USDA surprised markets in July by hiking the total US corn planted area from June estimates, to 91.7 million acres for the 2019-20 marketing year (September-August), despite expectations the USDA would lower the acreage number due to difficult weather conditions that delayed planting in the US corn belt.

What’s next? Traders, analysts, producers and exporters will be eyeing the US corn and soybean outlook, as delayed planting of corn and soybeans could eventually weigh on production and supply. The US is the world’s largest corn producer and exporter, and second-largest soybean producer and exporter. The most active soybean and corn contracts trading on the Chicago Board of Trade rallied by 3-4% in the last three days before the WASDE report release on expectations of lower soybean and corn yields versus the USDA’s July estimates. A bullish corn and soybean outlook could also give a boost to short covering in Chicago and Kansas wheat futures.

Reporting by Jack Jordan, Paul Hickin, Rohan Somwanshi, Harry Weber, J Robinson and Henry Edwardes-Evans