01 Jul 2019 | 17:04 UTC — Insight Blog

Commodity Tracker: 4 charts to watch this week

S&P Global Platts editors' pick of unfolding commodities trends. This week, oil markets await updates on OPEC supply in the second half of the year, while LNG flows could shift on diverging regional prices. Gold is in the spotlight following a spike in late June, and European carbon prices are nearing winter fuel-switching levels.

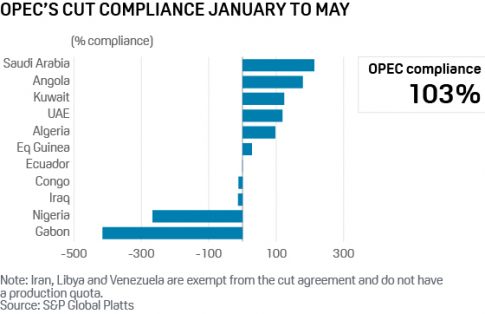

1. Will OPEC and allies extend supply cut agreement?

What’s happening? OPEC and its allies are gearing up to extend their 1.2 million b/d in production cuts beyond the first half of the year. The oil market has been caught between global economic growth concerns and likely increased US supply on one hand, and sharp falls in Iranian and Venezuelan production and continued Saudi supply restraint on the other. Heightened geopolitical risks around trade disputes, sanctions, and tensions around the key chokepoint of Strait of Hormuz have complicated the matter as OPEC and Russia look for clarity in their market rebalancing efforts.

What’s next? The oil market – with Brent crude hovering between $60 and $70 a barrel – will be looking for clear signals on how OPEC and its allies plan to manage the market in the second half of the year, when the producer coalition meets July 1-2 in Vienna.

2. Asia could pull in more LNG as JKM-TTF spread widens

What’s happening? The JKM-TTF spread is widening, as Asia prices firm while those in Europe plunge. The spread is an indicator of the margin traders can achieve by arbitraging LNG cargoes between regions. At the moment the spread is $0.5/MMBtu above what is required to make Asia a better destination than Europe for Atlantic spot LNG cargoes.

What’s next? If the JKM-TTF spread widens by another $0.4/MMBtu to $1.7 it could re-open the arbitrage for re-load of LNG cargoes from Northwest Europe to Asia. This would mean an even bigger drop in LNG imports into Europe and could put a brake to the slide of European prices.

3. Gold takes a breather but market keeps eyes on Fed

What’s happening? The gold price has leveled out around $1,400/oz following a strong run higher. Tension in the Middle East, a gloomy outlook for the global economy and the possibility of a US Federal Reserve rate cut later in 2019 have all supported gold’s role as a safe haven for investors. Now the market is taking a breather as global equities regain steam on renewed fiscal stimulus hopes, but the price remains well supported.

What’s next? US interest rate cuts would support gold, as they could indicate higher inflation in the US, weakening confidence in the US dollar. And when the dollar weakens, gold rises.

4. EU carbon price edges nearer winter fuel switch level

What’s happening? In Q2 2019, EU carbon prices have moved higher towards the implied winter fuel switching price. This is the price of carbon at which coal and gas become equally profitable. Natural gas prices fell so far this year that the capacity for coal-to-gas fuel switching may be exhausted for this summer, according to S&P Global Platts Analytics.

What’s next? There may be little room for power sector EUA demand to fall over the next few months, even with lower gas prices. Instead, EUA prices have maintained a relationship with implied carbon prices this winter, supported by relatively higher winter gas prices. This is helping to make coal-fired electricity competitive against gas, boosting utility hedging demand for EUAs. However, this could change if winter gas prices start to fall as a clearer picture of winter gas storage levels develops.

Reporting by Herman Wang, Paul Hickin, Frank Watson, Fabio Reale, Diana Kinch and Ben Kilbey. Edited by Emma Slawinski.