09 Mar 2020 | 19:19 UTC — Insight Blog

Commodity Tracker: 4 charts to watch this week

As oil markets and the wider commodities complex digest the breakdown of the OPEC+ alliance, they are also assessing the demand-side damage wreaked by coronavirus. In the European power sector, it’s the weather that is holding markets in thrall: wind generation continues to smash records as March proves almost as stormy as February.

1. No reprieve for oil markets as OPEC talks flounder

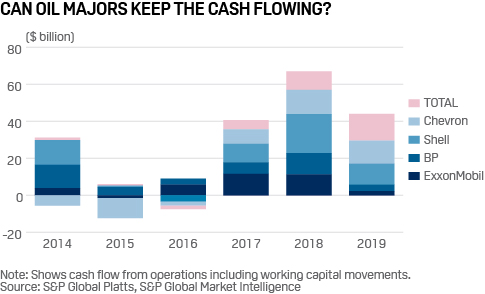

What’s happening? Oil majors will be hoping the carnage on the oil markets doesn’t last too long after the alliance between OPEC and Russia fell apart. The tone is set for increased supply from all oil producers and in particular Saudi Arabia amid coronavirus-led demand weakness. While analysts believe Big Oil will keep investment plans intact in the coming months, this really depends on whether oil prices stay well below $50/b for a sustained length of time, with US shale being particularly exposed.

What’s next? S&P Global Platts Analytics believes Saudi Arabia, Russia and the Gulf producers could add up to 2 million b/d in the coming months, and with an ongoing worsening in the coronavirus epidemic, there is a risk that Brent oil prices will drop below $30/b. The question is whether the price fall incentivizes OPEC and Russia to mend their fences and agree a new production cut deal.

2. Dr. Copper rings warning bell for economic health

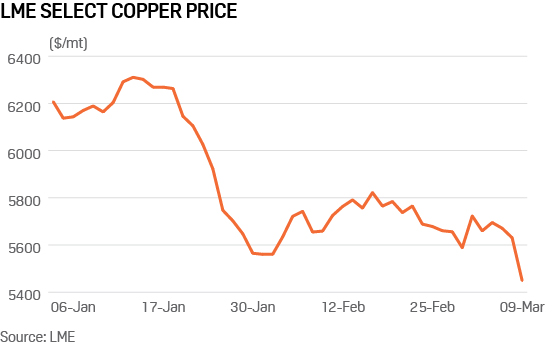

What’s happening? Copper, often seen as a bellwether for the global economy had already been hammered by the coronavirus outbreak. The metal took another pummeling at the start of the week after OPEC and Russia failed to reach an agreement on production cuts. With oil prices down by around 30% on Monday, the tone was set for the wider commodities and equities markets, not least copper.

What’s next? Little is certain now other than increased volatility. London Metal Exchange three-month copper started 2020 at $6,188.5/mt, buoyed by an increasingly bullish fiscal outlook. The metal hit an intraday low of $5,433/mt Monday. COVID-19 quickly demolished any sense of hope, and the OPEC news fanned the flames of price destruction. Many are now suggesting that recession is inevitable, however, the surprise news over the weekend and the resulting chaos prove that forecasting can be a very tricky game.

3. Korean transport sector sees rising toll of coronavirus outbreak

What’s happening? Seoul's ongoing battle to contain the spread of COVID-19 is hitting automakers and road traffic volumes hard. According to state-run Korea Expressway Corp., auto traffic on the country's highways dropped 25%-29% over the weekend of February 29-March 1 from a year earlier, while passengers of KTX bullet trains plunged over 84%. On top of that, South Korean auto manufacturers posted sharp declines in new vehicle sales in February. Combined sales in both domestic and overseas markets fell 10.7% year on year to 505,212 units in February, led by a 13% drop in sales by the country's biggest automaker, Hyundai Motor. In particular, new vehicle sales in the domestic market dropped 21.7% year on year to 81,722 units in February, the lowest since January 2009, when the country was hit by the global financial crisis.

What’s next? The sharp declines in vehicle sales and road traffic suggest a tepid gasoline and gasoil consumption outlook for the rest of the first quarter. Based on an S&P Global Platts survey of traders and fuel marketing sources at major South Korean refiners SK Innovation, S-Oil Corp., GS Caltex and Hyundai Oilbank, diesel fuel and gasoline consumption tumble to around 45 million barrels in Q1, down around 29% from the same period a year earlier.

4. Europe’s wind generation blows away competition in February

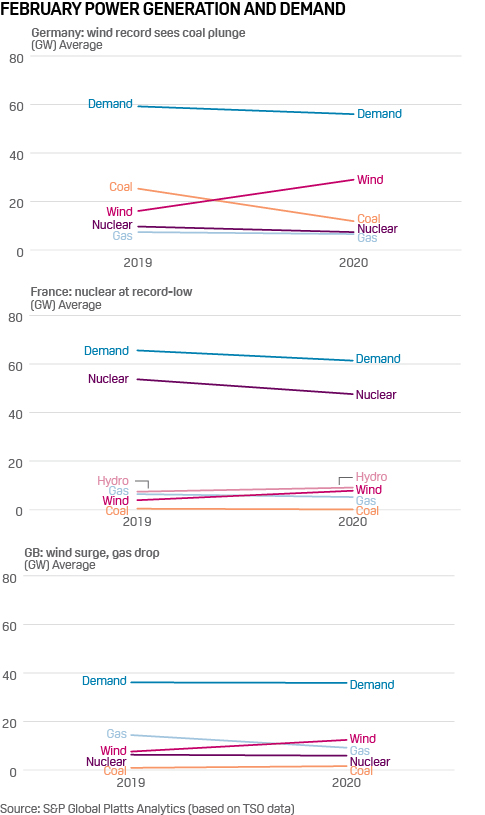

What’s happening? Wind power generation soared across Northern Europe in February, pushing German coal, UK gas and at times even French nuclear power plants off the grid. In Germany, wind met 46% of national demand through the month, double on year, with lignite and hard-coal generation collapsing 52%. In Great Britain, wind topped the monthly power mix ahead of gas, another first. French wind also more than doubled on year. Negative prices during offpeak weekend hours became more commonplace across European markets hitherto unused to this phenomenon.

What’s next? A lull in wind generation in the first week of March changed this dynamic with UK imbalance system prices spiking over GBP2,200/MWh during the teatime peak March 4. Wind is forecast to rise sharply across Northern Europe in week 11, however, which may also see the first significant solar spikes of the year as days lengthen. Responding appropriately to the new volatility in electricity markets remains a key challenge for policymakers. Flexibility and speed of response are the watchwords, with battery storage, peaking plant and demand response service providers well placed to benefit.

Reporting by Paul Hickin, Ben Kilbey, Philip Vahn, Clarice Chiam, Charles Lee, Mark Tan, Andreas Franke and Henry Edwardes-Evans