19 Jan 2017 | 20:26 UTC — Insight Blog

GOP tax reform and what’s at stake for the oil industry

This blog post was written in collaboration with John Kingston, the Director of Global Market Insights for S&P Global.

The U.S. still imports a lot of crude oil. It also now exports crude oil. It’s also the world’s biggest exporter of petroleum products.

So any change in the country’s corporate tax system that has an enormous shift in the tax treatment of imports and exports is going to have the potential to impact oil flows, and by extension, oil markets.

It’s a realization that is starting to spread through the nation’s oil industry as the inauguration of Donald Trump draws closer and the possibility of DBCFT becomes more possible. DBCFT is the abbreviation for Destination Based Cash Flow Tax, and it’s the general term for the type of tax that is at the heart of the Republicans’ corporate tax proposal, spearheaded primarily by Speaker Paul Ryan (R-WI) and Ways and Means chairman Kevin Brady (R-CA).

The analyses of the tax plans are coming out fast and furious in the last few weeks. The short version of what you need to know is this:

- The intellectual basis for the plan actually comes from the left side of the political divide: Alan Auerbach, a professor at the University of California-Berkeley, who released a paper in 2010 under the auspices of the Center for American Progress, which in the Obama years has been the most prominent left-leaning think tank. The DBCFT has been likened to having many of the same fundamental characteristics as a European VAT. As the Ways and Means blueprint on the proposal states: “The focus on business cash flow…(is) a move toward a consumption-based approach to taxation.”

- The US version of the DBCFT would lower the top corporate tax rate to 20%. But its provisions that have gotten the most attention — because they are such a radical departure from current policy — are that companies would not need to count revenue from exports in their tax base, but would not be allowed to deduct the cost of imports.

- The economics 101 analysis of the impact of these changes is that the value of the dollar would increase significantly, offsetting the higher prices for imports (like low-cost apparel to be sold at Walmart), thereby negating price increases for the US buyers of that product. This part of the equation is much in dispute, but it does seem clear that a further strengthening of an already healthy dollar would occur, as imports decrease (putting fewer dollars into global markets) and now tax-favored exports increase (necessitating dollars for the goods’ purchase).

The potential areas of impact to the global oil industry are clear. The US oil industry will be incentivized to export more crude and products, import less of the same, and the always-present correlation between the dollar and the price of oil will be a significantly bearish factor. Just how much of an impact remains a significant question.

Related:Find more content about Trump's administration in our news and analysis feature.

In a report published by the Brattle Group, energy economist Philip Verleger was blunt: “No sector…will be more affected than petroleum.”

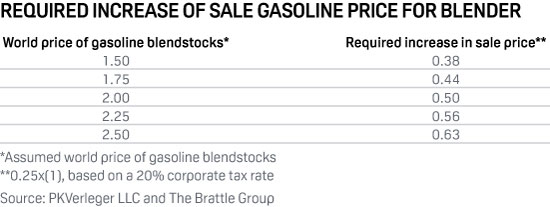

Verleger estimates the policy would drive a 25% wedge between domestic and imported oil prices. For example, if Continental Oil sells Bakken crude to a domestic refiner for $50/b, it will owe $10/b in US taxes. However, it would have no tax liability if it sells the oil to an overseas buyer.

"Obviously Continental would want to sell the oil to foreign buyers for $50 rather than to domestic buyers," Verleger said. "To bid the oil away from the foreign buyers, domestic refiners would have to pay Continental $62.50/b."

Given that the US oil industry is a net importer of all categories of petroleum — importing 9.45 million b/d versus exporting 4.74 million b/d last year — the policy would hurt the sector as a whole assuming crude and product prices don’t fully adjust to compensate for the import tax impact, said Tudor Pickering Holt analyst Chi Chow. PBF Energy is by far the most exposed refiner because its net imports represent 51% of production, with Par Pacific Holding not far behind with 39%.

TPH expects refiners to respond by shifting toward domestic crude sourcing, which could cause WTI, Bakken, LLS, Mars and ANS prices to rise sharply. Higher domestic demand would spur US production, and exports of both crude and products could surge.

Gasoline and diesel prices will rise, along with prices for most consumer goods, an impact that some see would make DBCFT a political nonstarter. Verleger estimates retail gasoline prices would rise 30 cents/gal, or 13%, and diesel would increase 27 cents/gal, or 11%, when Brent is $50/b, based on a step-by-step analysis taking into account the various rates involved.

"The perception that you're going to increase gasoline prices is so politically powerful that it can be very difficult to work backward to the economic currency-adjusted and present-value-adjusted results," said Kevin Book, a managing director of ClearView Energy Partners.

Book said a lot will depend on the legislative text, but he is in the economic camp that the currency effects would offset higher prices. "If I buy the same barrel with a stronger dollar, the impact should be the same," he said.

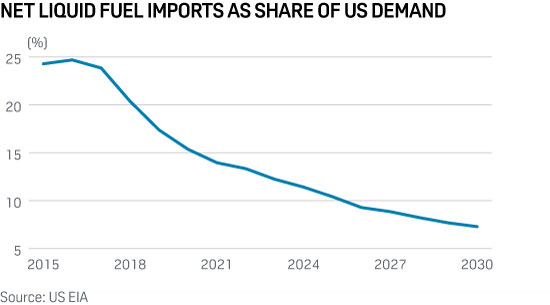

Even with potential blowback from higher gasoline prices, you can’t help but wonder if the US would have even considered a destination-based tax overhaul if its petroleum import dependence was still 50% and higher, compared with 24% projected by Energy Information Administration for this year — and falling.

Gregory Jenner, a partner at Stoel Rives who helped write a 1986 tax reform package signed by President Ronald Reagan, said the GOP’s proposal could have sweeping effects.

"We are talking about a tax system that has been in place for approximately 100 years now, and we have an economy that has grown up around it,” Jenner said. "What this new tax provision would do would be to completely upend that arrangement. That could be for the good, it could be for the bad. We just don't know.

"What we're going to see if this gets enacted is a complete realignment of the economy. It's not just oil and it's not just Nike sneakers. It's everything that is now produced offshore”