16 Nov 2018 | 21:33 UTC — Insight Blog

Spread between CAPP coal, ARA coal tightest in nearly four years

By Tyler Godwin

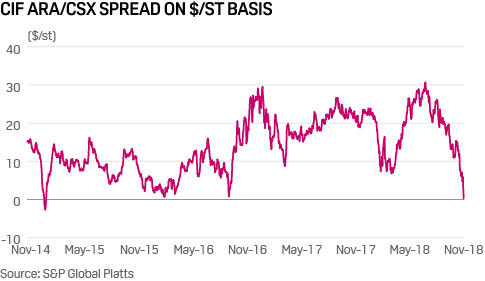

After being at a six-year high in July, the spread between Central Appalachia (CAPP) thermal coal and thermal coal delivered into Northern Europe fell to its lowest level in nearly four years Wednesday.

CIF ARA 6,000 kcal/kg coal, for delivery in the next 15 to 60 days to Amsterdam, Rotterdam or Antwerp, was assessed Wednesday by S&P Global Platts at a six-month low of $85.95/mt, while rail-delivered (CSX) CAPP coal for December delivery was assessed at $77.75/st.

The spread between the two grades of coal Wednesday was at 22 cents on a short-ton adjusted basis, the lowest since January 2015.

CAPP rail (CSX) coal, which is roughly 6,700 kcal/kg, has long been valued by Europe for its relatively high heat content and low sulfur. But because of the significant transportation costs to ship CAPP rail coal from mines in southern West Virginia and eastern Kentucky to ports in Virginia’s Hampton Roads region and then across the ocean, the export window for CAPP rail coal can frequently swing shut.

For instance, in July, CIF ARA peaked at $103.70/mt, its highest level since January 2012, and CAPP rail coal was assessed at $63.40/st, a spread of $30.67 on a short ton-adjusted basis, the highest since April 9, 2012.

The wide spread this summer likely led to an increase in booking for CAPP coal, but that additional demand has also pushed up pricing for CAPP coal through the fall, as the region’s production remains constrained as thermal producers hold back on adding new capacity out of fear that the recent market rally is not sustainable.

Production in Central Appalachia was at 19.48 million st in Q3, down 6.9% from Q2 but up 3.3% from 18.85 million st produced in the year-ago quarter, according to preliminary data from the US Mine Safety and Health Administration.

The CAPP region is also home to the US’ metallurgical coal sector, where demand has also shot higher this year due to high seaborne prices. Arguably, much of the additional production last quarter was met coal rather than thermal.

Since July, prompt prices for CAPP rail thermal coal have climbed from a near-term low of $56.50/st on May 11 to a high of $78/st on November 2.

While short supply has helped push up CAPP rail pricing, CIF ARA prices have dropped by 16% in the last month on concerns northern Europe is now oversupplied.

History tells us that when the CIF ARA price declines, so does the CAPP rail price.

The last two times CIF ARA had big declines, of 29.4% between late December 2016 and late March 2017, and 21.7% between early January and late March 2018, CAPP rail coal fell 22.9% and 12.7%, respectively.

CAPP rail coal prices have so far held steady, though the spread between the two coals will be watched more closely if the CIF ARA price continues to drop, as one would have to go back to Fall 2008 for the last time the CIF ARA price dropped below the CAPP rail price.