27 Jul 2017 | 10:31 UTC — Insight Blog

US propylene market faces long H2 as new capacity comes online

By Nida Qureshi

The US propylene market is looking bearish for the second half of 2017 as a major capacity addition in the US Gulf Coast is expected to further lengthen supply and lead to more exports, which have already been on the rise.

From January to April, the most recent month for which data is available, the US exported 143,324 mt of propylene, a 15% increase over the same period last year, according to the US International Trade Commission.

Startup of Enterprise Product Partners' 750,000 mt/year propylene-capacity unit in Mont Belvieu, Texas is expected sometime during Q3.

Completion of the propane dehydrogenation unit, only the third of its kind in North America, has suffered repeated delays. It was originally scheduled for completion in Q3 2015.

In fact, some trader sources pointed to these delays earlier in the year to explain, at least in part, why spot and contract pricing shot up on tightness resulting from planned and unplanned outages in the US Gulf Coast region during Q1.

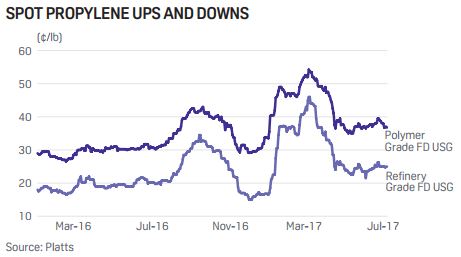

Spot refinery-grade propylene rose nearly 180% from January to a 27-month high of 46 cents/lb ($1,014.11/mt) on a delivered basis in early March; polymer-grade propylene, a higher-purity grade that typically commands a 10-12 cent/lb premium over RGP, jumped nearly 61% for the period to a near 27-month high of 54.25 cents/lb, also on a delivered basis, according to S&P Global Platts data.

Contract pricing, which is driven by spot, followed suit, with March's 52 cents/lb settlement the highest since December 2014, when contracts were assessed at 61.50 cents/lb.

The gains were short-lived, however, with the market falling steeply in April as turnaround season in the US Gulf Coast region wrapped up before stabilizing in May and June.

Propylene markets have seen little support from crude oil pricing, which struggled amid persistent oversupply.

Spot RGP averaged 30.66 cents/lb during H1 2017, closing the period at 25 cents/lb. Spot PGP averaged 43.18 cents/lb, ending June at 38 cents/lb.

The relative strength during H1 versus the year-ago period — spot RGP's average was nearly 60% higher than H1 2016 while spot PGP's was 43% higher — caught some in the market by surprise.

This is because US propylene markets have switched from tight to long over the past couple of years amid strong refinery output and more on-purpose production. Heading into the new year, some expected the bearish sentiment to prevail for much of the year.

The startup of Dow Chemical's 750,000 mt/year PDH unit in Freeport, Texas in late 2015 was a significant capacity addition, even though its production is meant for captive use.

Strong refinery utilization rates in recent years have increased output and also pressured prices lower, sources said. Refinery run rates averaged 90.41% through mid-June this year, according to US Energy Information Administration data, even as Q1 production weakened when compared to Q1 2016.

Total US propylene production in Q1 — including chemical sources and refinery sources — decreased nearly 6%, totaling 7.882 million lb against 8.381 million lb in Q1 2016, data from the American Fuel and Petrochemical Manufacturers showed.

The lower production levels during Q1 came amid planned and unplanned steam cracker and refinery outages in the US. Eight steam crackers, one PDH unit, and two splitter outages in Q1 contributed to lower output.

Spot PGP fell 19.25 cents from March 7 to May 12, hitting a four-month low at 35 cents/lb FD USG, Platts data showed.

Spot RGP also fell to a three-month low on June 6 at 21.5 cents/lb FD USG, having shed 24.5 cents from March 8.

Downstream demand, mainly from polypropylene and acrylonitrile markets, started weak in 2017 as the propylene prices shot up, but quickly picked back up once monomer began its descent.

In the polypropylene market, the biggest demand pull for propylene, domestic business was affected by a long dry spell with some producers heard having reduced rates to match the lack of demand.

But as monomer pricing began to fall, PP business began to pick up, with orders for May and June being sold out quickly. PP buyers wanted to buy their contract volumes plus 20%-50% more on top, sources said.

Even with demand from the resin side strong, no major expansions are scheduled online for at least the next two years to absorb the recent and upcoming additions on the propylene side, further feeding the bearish outlook, sources said.