13 Jul 2016 | 10:31 UTC — Insight Blog

Brexit implications on the cost of UK polymer imports

By Kristen Hays

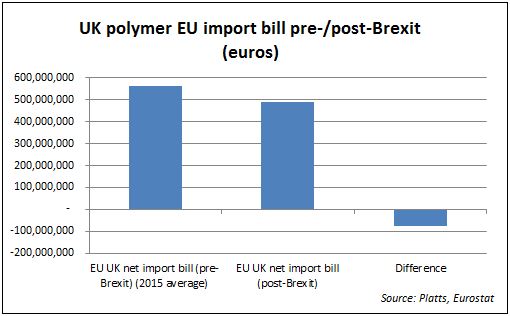

The British pound’s sharp slide to 31-year lows versus the US dollar in the volatile aftermath of last month’s Brexit vote could potentially hike the United Kingdom’s polymer import costs by $100 million, a 13% increase in the overall net import bill for polymers (polyethylene and polypropylene).

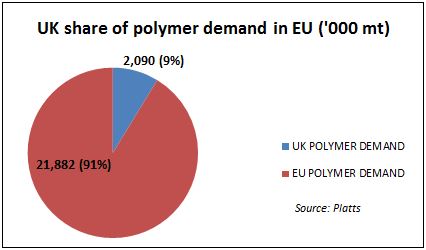

As a result of this potential hike, British pound could lose the equivalent of 3% on import value as a percentage of the overall domestic market. The UK’s net import bill accounts for 20% of its market value in terms of demand and as a result of the post Brexit currency volatility, this could increase to a quarter of the value of the market.

All the analysis throughout this post is based on 2015 annual polyethylene and polypropylene trade figures and the net import bill is based on 2015 average exchange rates and rates in the aftermath of Brexit.

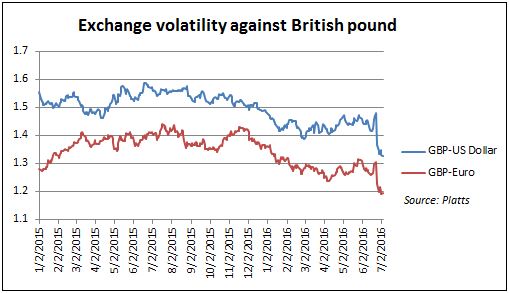

The morning of the June 23 Brexit vote, the US dollar was at $1.47 against the British pound and average 2015 levels were at $1.525. By July 8 it had fallen more than 12% to $1.29, levels not seen since 1985 when Mikhail Gorbachev took the helm of what was then the Soviet Union and star-studded Live Aid concerts raised millions for Ethiopia famine relief. On Tuesday it had rebounded to $1.31, down nearly 11% from pre-vote levels.

The British pound's value versus the euro has been similarly bruised and battered. The UK, a net importer of polymer and in terms of market size (demand terms) accounts for just 10% of the European Union market, relies on the EU for 80% of its imports. On July 8 the euro was 1.17 to the pound, down 10% from 1.30 on the morning of the Brexit vote and average in 2015 of 1.378.

This could push up costs of EU imports by Eur75 million, if the UK import the same level of material as recorded in 2015 at these post-Brexit exchange rate levels. By Tuesday the Euro was 1.18 to the pound, down 9.2% from pre-vote levels.

Companies quickly saw those costs show up

Barry Twigg, chief executive of National Flexible, the UK’s largest distributor of polypropylene, laminates and special films, said that several European suppliers have hiked prices to compensate for higher export costs. Those include a 7% price increase from a European manufacturer of orientated polypropylene, the packaging film known as OPP commonly used in cookie packaging. In addition, suppliers in Turkey and the Middle East withdrew or suspended price lists with plans to charge more, and an Indian company is seeking higher prices.

“In each case we have asked them to rethink their approach, and as yet have had no response,” Twigg said.

He noted that the UK flexibles market is a major customer for European film suppliers who want to maintain their UK-bound volumes. He said film manufacturing capacity is currently oversupplied in Europe, with more planned in the Middle East, so Twigg anticipates no major supply issues in the near future. Last year Chinese suppliers quickly filled a brief film supply shortfall, he said.

In March Twigg said a Brexit could hike import costs of bulk films from Europe and reduce sales volumes from some food producers if their exports declined. However, he said competitors elsewhere could replace European suppliers and National Flexible’s packed food exports would continue.

Last week Belfast media reported that Greiner Packaging executive Jarek Zasadzinski said during the opening of a new plastic pot manufacturing facility in Dungannon, Northern Ireland, that he wanted to ask former London Mayor and pro-Brexit campaigner Boris Johnson for a check to cover the Austrian plastic packaging manufacturer’s increased costs to import into the UK.

He told reporters that Greiner could be forced to hike prices for customers to compensate for the exchange rate moves. He also said the company would not leave Dungannon, but was preparing contingency plans and hoped currency fluctuations would stabilize.

The UK is the fourth-largest EU polymer importer with an 8% share behind Belgium, Germany and France, Platts Analytics and Eurostat show. It also is sixth in terms of exports to the rest to the rest of the EU, with a 5% share.

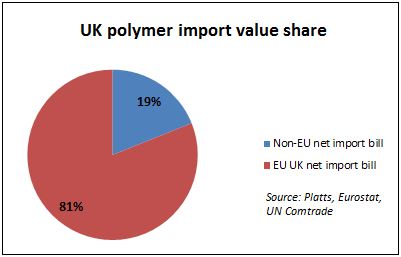

While 80% of the UK’s polymer trade is with other EU partners, the rest is largely with Saudi Arabia, Israel and Brazil, in that order. The US is the UK’s fourth-largest non-EU importer.

UK polymer exports outside the EU total 18,900 mt while the region imports 140,000 mt from non-EU members, according to UN Comtrade data.

Two years ago the EU hiked tariffs for Middle East polymer coming into the region by 3.5% to 6.5%. EU converters have lobbied to reverse that hike over the last year or so. Post-Brexit, the UK could negotiate its own trade terms with the Middle East, as most material comes from that region or is re-exported from the EU.

In addition, South Korea has a free trade agreement with the EU that the UK could maintain while exploring trade with other non-EU countries, particularly in Asia. Even with small polymer export trade to countries outside of the EU, having full control of tariff controls on imports could encourage growing exports through a host of favorable trade deals. New agreements could be struck with the likes of India, Russia and parts of Africa.

While debating these possible options as a result of Brexit, the industry, in line with the wider economic, social and political landscape is braced for a period of uncertainty as post-Brexit measures are yet to be discussed.

Nick Mockett, head of packaging mergers and acquisitions for London-based Moorgate Capital, said some UK plastics companies put hedges in place ahead of the Brexit vote, “which will give breathing space for a period.”

National Flexible’s Twigg said he understood film suppliers’ rush to hike prices post-Brexit with the current oversupply in Europe. He noted that currency fluctuations are an inherent feature of the business, and the British pound/euro rate had fallen as low as 1.10 before.

Twigg anticipates that the pound will recover to a trading level of 1.20 to 1.25 versus the euro, which should not be a major problem for the UK flexibles market. Plus, lead times on many films stretch up to six weeks and National Flexible is holding stocks for many customers until August or September as the post-Brexit fluctuations shake out.

However, polymer and dollar rates remain wild cards, he said.

“Currently the petrochemical companies have high margins. The question is, will they accept some erosion or close capacity? We shall see,” Twigg said.

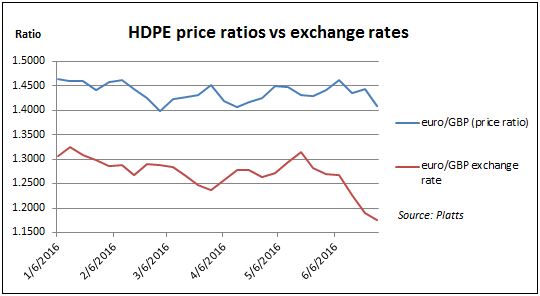

Prices not fully reflecting currency weakness

The UK industry’s recent prices are holding up and have not fully reflected the weaker British pound, as the chart below indicates. A number of reasons could account for this, such as levels of rebates and discounting when trades or purchases could be fixed on other FX terms. If so, any future hikes in net import bills might not be as high as discussed earlier.

Overall, the UK remains heavily intertwined in the wider European market. For many it will not be an easy departure, as markets remain volatile due to the high levels of uncertainty. However, in the medium to long term, things may not change that much, despite the rhetoric, when trade deals are renegotiated with the rest of Europe in the next two to three years.

Hetain Mistry, managing analyst, qualitative analysis, also contributed to this post.