12 Jul 2016 | 10:31 UTC — Insight Blog

US methanol projects find economics changed on oil, gas prices

By Thad Walker

Over the past five years, interest in US methanol production has exploded. There has been the reopening of mothballed plants, relocation of southern-hemisphere plants and billion dollar investments in brown and greenfield projects. These investments were all predicated on a unique pricing relationship: a historically wide natural gas-to-crude ratio.

However, this pricing relationship has been altered, changing the economics of methanol production in the US and raising questions about the future economic viability of US ethanol expansions. This piece outlines and analyzes the changing economic nature of the US methanol landscape and shows that methanol economics are not as rosy as they were a few years ago.

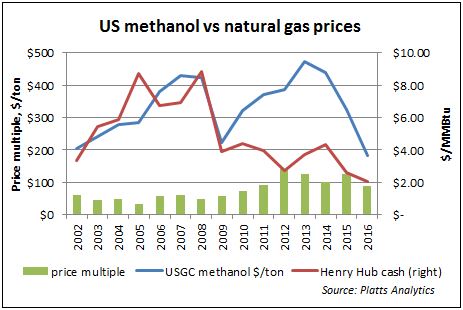

The increased price multiple between US natural gas, crude and methanol made methanol production economics favorable in the US. After methanol spent the past decade at a price multiple of less than 100x natural gas prices, it has averaged 112x since 2011, highlighting the value of turning natural gas into methanol. This has led to the proposals for nearly 34 million tons per year of new capacity to be added to the US market.

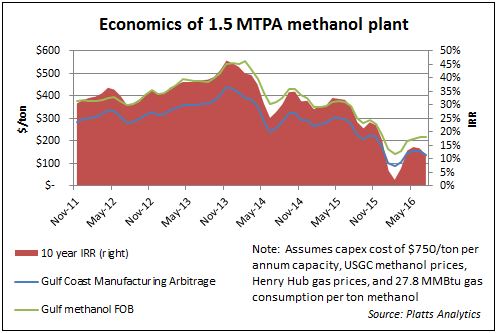

But our analysis shows that the economics of US methanol production have taken a hit in the lower oil price environment.

The IRR, or internal rate of return, is a metric used in capital budgeting to measure the profitability of potential investments. Hurdle rates for IRR vary but 10-20% is typically considered economically feasible. For example, the current IRR of a Permian oil well is 23%, the highest IRR of oil and gas basins in North America, based on Platts Bentek’s June 2016 IRR analysis.

For our analysis we considered the initial investment costs split between a construction timeline of two years, and natural gas for feedstock and methanol output for its first 10 years of operation.

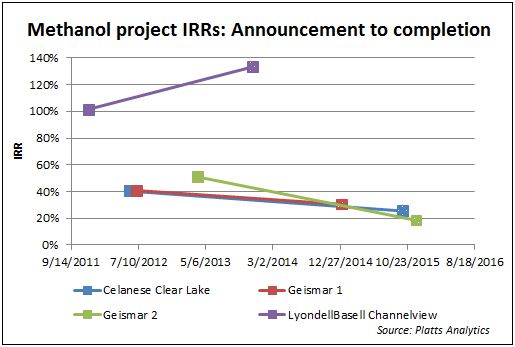

The methanol projects in the US that have been proposed, are under construction or are online all had unique traits that alter the economics of each project. For example, Methanex transported two 1 million mt/year units from Chile to Louisiana. Even after going over budget by roughly $200 million, the two units were relocated for a total price of $1.4 billion, or an average of $700/ton per annum of capacity. This was roughly $50/ton per annum less expensive than the average of all facilities analyzed. The first Geismar unit would have generated an IRR of 41% when proposed in July 2012, and the estimated IRR fell to 31% by the time the unit actually came online in January 2015.

The highest IRR can be traced to LyondellBasell’s Channelview facility, which was an existing facility mothballed in 2004 due to high natural gas prices and thus low margins. LyondellBasell announced in December 2011 it would bring the 780,000 mt/yr facility back online at an estimated cost of $150 million. While the decision at the time of announcement, assuming the initial construction costs were sunk, would have provided an IRR of 102%, the estimated IRR increased to 133% by the time the unit returned to operation in December 2013 as the value gap between natural gas and methanol widened even more.

The methanol expansions in the US have been eyeing the growing Chinese MTO market as a source of demand for the incremental demand. In fact, several projects have been proposed aiming to directly supply these olefin-producing plants.

Northwest Innovation Works announced plans to build three methanol projects in the Pacific Northwest in January 2014, and the $1.8 billion facilities would have each generated a 10-year IRR of 63%. In addition to having cheaper feedstock gas, averaging roughly 10 cents/MMBtu below the Gulf Cost benchmark over the past five years, the facility would also benefit from much closer proximity to China and therefore lower shipping costs. While natural gas prices in the Pacific Northwest have developed an increased discount to Henry Hub over the last few years as more heavily discounted Canadian volumes move into the region, the projects would now only return an IRR of 25%.

While a number of methanol units are under construction and expected to come online over the next few years, the economics are not near the level they stood during the higher-priced crude environment a few years ago. In fact, citing concerns over the current US pricing dynamics, BASF recently announced that it is reassessing its gas-to-propylene plant in the US.