29 Jun 2016 | 10:31 UTC — Insight Blog

Latin America grapples with lack of petrochemical investment

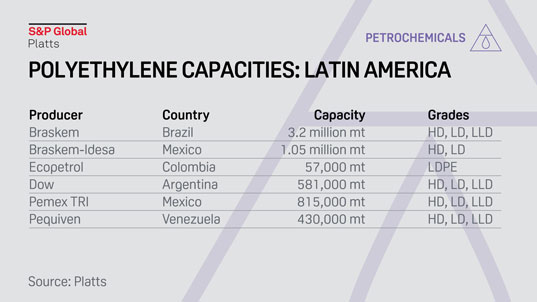

Not far from the Port of Coatzacoalcos in Mexico, a sprawling new petrochemical complex owned by Braskem-Idesa has risen from the ground, poised to help the country minimize its ballooning polyethylene deficit.

And while production has been slower to come on line than initially expected and there is talk within the market that delivery of enough ethane to run the 1 million mt/year ethylene-capacity steam cracker has been an issue, Braskem-Idesa is years ahead of their Latin American counterparts, many of whom are grappling with financial issues stemming from a low-crude environment and see their futures uncertain.

Beyond Mexico, proposed petrochemical expansions have fallen by the wayside in Latin America. Ambitious olefins/polymer projects in Brazil and Venezuela have been effectively paralyzed, while others in Peru and Bolivia also remain in limbo. Talk of major polymer expansions in Argentina, another country with some of the world’s largest shale gas reserves, has been just that.

Polyethylene production in Chile, a strong and growing market for resins, ended in May 2014.

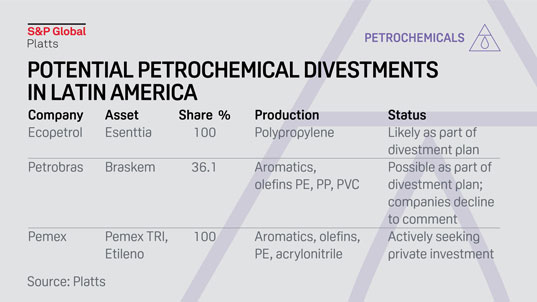

Since the plunge of oil prices during the second half of 2014, state-owned energy companies including Petrobras in Brazil, Ecopetrol in Colombia and Pemex in Mexico have all hinted at divestitures of their petrochemical assets as a way to cope with diminished oil revenue.

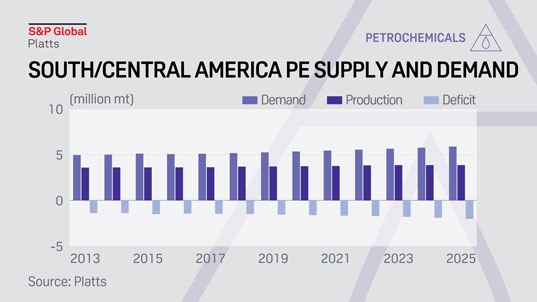

In 2015, the polyethylene deficit for Central and South America stood at more than 1.5 million metric tons, and that deficit is forecast to grow to more than 2 million metric tons by 2025, according to S&P Global Platts Analytics.

South America possesses the necessary natural resources and a growing middle class that will drive greater demand for polymers and other petrochemicals over the next 15 years. However, the Central and South American markets have not been able to take advantage of low-priced feedstocks like their North American neighbors.

The lack of investment in the region highlights why Latin America will be a hot market – and a battlefield – for North American resin producers in the coming years.

That’s not to say more investment could not eventually happen. After all, not many would have predicted the US turnaround just a decade ago.

At the most recent APLA conference, representatives of global petrochemical companies noted that Latin America does have resources to replicate the petrochemical growth seen in the US, but key decision makers in the region must work to make sure they are creating environments where the industry can thrive.

The key for these countries will be ensuring stable fiscal and investment climates, balanced contract terms, and clear regulatory requirements, based on market feedback.

Even if the new investments do not come to fruition, countries like Brazil, Colombia, Chile and Argentina are well positioned to benefit from the lower-priced petrochemicals expected to be exported from the US, Middle East and Asia over the next decade.