19 Jan 2016 | 10:31 UTC — Insight Blog

The impact of Saudi ethane price increases on competitiveness

By Ben Gonzalez

At the end of December, Platts reported that Saudi Arabia increased the price of gasoline, domestic gas for power generation and ethane feedstock in its 2016 budget, part of a broader program to cut subsidies and reduce its budget deficit. As a part of this, the ethane price more than doubled from the long-standing fixed price of $0.75/MMBtu to $1.75/MMBtu, according to the official Saudi Press Agency.

So what does this mean for Saudi Arabia's position as the world's lowest-cost ethylene producer?

Setting the stage

According to Platts Analytics, Saudi Arabia has 13 steam crackers currently operating with a total ethylene capacity of 15.7 million mt/year. For 2016, we expect capacity to reach 16.9 million mt with the start of the 1.5 million mt/year Sadara cracker.

Additionally, the country will have a full year of production from the Petro-Rabigh unit 2 cracker, which started up in mid-2015. The largest facility in the country is the 2.45 million mt/year Petrokemya steam cracker in Al Jubail. The facility has a naphtha-based cracker with a capacity of 700,000 mt/year (Unit 1), an ethane/propane mix cracker with a capacity of 950,000 mt/year (Unit 2), and an ethane-based cracker with a capacity of 800,000 mt year (Unit 3).

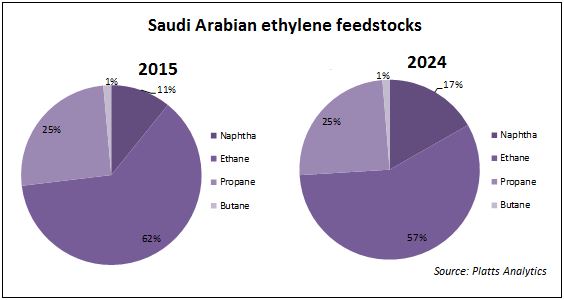

Approximately 62% of the ethylene produced in Saudi Arabia is from ethane, followed by 25% from propane, 10.8% from naphtha, and 1.4% from butane according to Platts Analytics. By 2024 we expect the percent of ethylene produced from naphtha to increase to 17%.

The question of competitiveness

How will this affect the competitiveness of Saudi ethylene producers in the region and the world moving forward? As reported by Platts, Saudi Arabia will remain the world’s lowest cost ethylene producer despite the significant increase in the cost of ethane. In order to compare regional prices we must look at everything on a $/mt basis. Using typical conversion factors, the $1.75/MMBtu Saudi ethane price on a $/mt basis is approximately $86/mt.

(To convert from $/MMBtu to $/mt we multiplied the $/MMBtu price by 66,000 Btu/gal. We then multiplied that by 742 gal/mt, and then divided by 1,000,000 to achieve the $/mt price.)

Even with the more than doubling of the ethane price, the feedstock cost for Saudi producers is much lower than the other producers in the Middle East using ethane and the US producers. The average US ethane price for January 12 was 15.13 cents/gal, or $112.26/mt using the aforementioned conversion factors. The price of naphtha in NW Europe and NE Asia for the same time period is $309.75/mt and $342.88/mt, respectively.

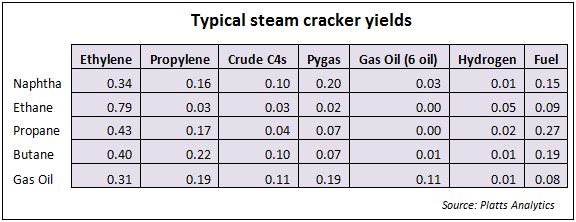

However, we must consider the amount of feedstock needed to produce one metric ton of ethylene. Using the typical cracker yields shown below, Platts Analytics calculated the price of feedstock to produce 1 mt of ethylene.

The estimated price of the amount of feedstock needed to produce 1 mt of ethylene is: $108.50/mt in Saudi Arabia using 100% ethane, $142.10/mt in the US using 100% ethane, $303.80/mt in other countries in the Middle East using 100% ethane, $911/mt in NW Europe using 100% naphtha, and $1,008.47/MT in NE Asia using 100% naphtha. When we factor in the co-products, and add estimated variable and fixed costs, we have the following approximate production costs.

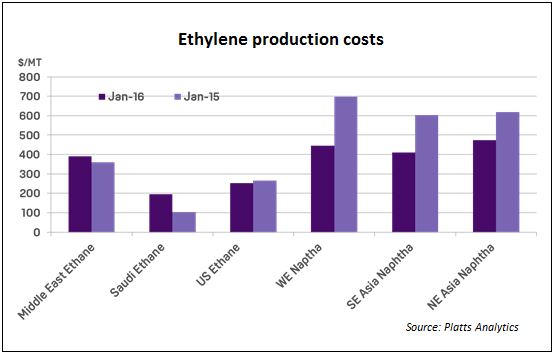

Regional production costs

The production costs above were calculated based on a 1 million mt/year cracker in each region using 100% of the same feedstock. However, this is often not the case. For instance, in the US, most crackers use a mixed feedstock comprised of NGLs, and the percentage of each component in the feedstock varies month to month. In Europe and Asia, producers are increasing flexibility in their units to take more LPG. In Saudi Arabia, as well as the Middle East, many crackers are using ethane, LPG, and naphtha in their feedstock mix.

The column chart above however can be viewed as the upper or lower end of ranges in production costs for each region. For instance, the Saudi ethane price shown in the chart can be interpreted as the lowest cost in the region. As mentioned above, most crackers are using a mixed feed of naphtha and LPG. The production costs for NW Europe and Asia naphtha crackers can be interpreted as the higher end of the range, as most crackers in both regions continue to increase flexibility to utilize more LPG.

Strategies to maintain margins

Saudi producers still hold the position as the most competitive ethylene producer globally followed by the US. The increase in production costs in Saudi Arabia will however erode margins. With only three components in the equation to work with — including net feedstock cost, variable cost and fixed cost — producers will have to increase efficiency in order to lower the variable costs.

Some strategies to increase efficiency by lowering variable cost can include horizontal and/or vertical integration including refinery/petrochemical integration or integration through the value chain — in this case, polymer plants.

Integration has proven to increase profitability by lowering costs through shared utility and labor costs, but does have its own costs added to it, including capital, transaction, and re-organization/management costs. We will see later this year how the producers in the Kingdom offset the higher production costs in order to maintain margins.

|

|

|||

| Platts Global Polyolefins Outlook |  |

||

|

Platts Global Polyolefins Outlook report and accompanying dataset helps you to understand how today's wide cracking margins are incentivizing a rush for new capacity and how this might erode the US feedstock advantage after 2017.

|

||

|

|

|||