28 Sep 2016 | 19:00 UTC — Insight Blog

Bullish at the top: How long can the sugar rush last?

By David Elward

The market is never as bullish as at its tops, nor as bearish as at its bottoms.

The first part of this trading adage is particularly pertinent to the state of play in the sugar market.

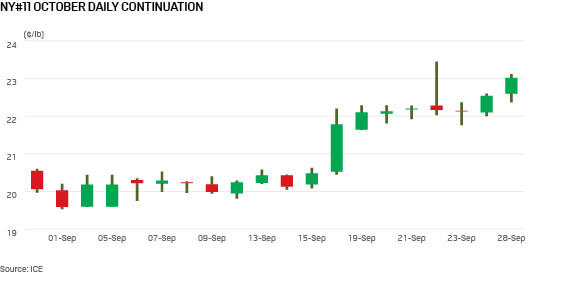

On Friday, September 16, ICE Sugar No.11, the raw sugar futures benchmark, began the day in unremarkable fashion. The October contract opened a touch higher than Thursday’s close at 20.53 c/lb and quickly slipped back to 20.45 c/lb.

A long summer of trading inertia had seen prices fluctuate within a range of around 19.5 c/lb to 21 c/lb for almost 15 weeks. There was little to suggest this day would be any different.

What happened next will be etched long in the memory.

By late afternoon the price had advanced 175 points to a high of 22.20 c/lb, with more than 4.7% of the gains made in two hours alone. It was the market’s largest one-day surge in over five years and returned prices to levels last seen in July 2012.

It capped a remarkable year for the supercharged sugar complex and once again marked itself out as the most eye-catching commodity. Measured against traditional safe-havens such as gold and silver, indexed returns have consistently shown sugar as one of the year’s leading commodity performers.

Explanations for the rally included: bullish crop updates from Brazil’s sugarcane heartlands in the Center-South region, where the 2016-17 season is nearing its midpoint; lower production from India, the world’s second largest producer behind Brazil, also generated chatter around additional imports; and technical charts had been hinting at a breakout to the upside.

You do not have to go too far to find a sugar analyst or physical trader who will tell you the price rally is overdone and a correction just around the corner. These views have been circulating since May, when NY11 was at 16.80 cents/lb on the front month, having increased 60% in nine months. The move had been supported by an injection of capital from hedge funds and individual traders, who looked at prices hovering around an historic low of 10 c/lb, spotted an investment opportunity and set about turning the speculators’ net short position of 80,000 lots into a net long of almost 300,000 lots.

The market anticipated a correction, and then a resumption of the upward trend. But the specs’ held onto their longs. The much-vaunted correction never came. Within weeks the price was above 20 c/lb and the specs expanded their net long position to a new high of 340,512 lots. Expectations of a correction were soon joined by opinions the rally was “overdone”. It lasted through the summer and has continued since the gains made September 16, as well as the subsequent price spikes which have propelled the market above 23 c/lb.

One strand of technical analysis would suggest that nothing unusual has happened. In the days leading up to the post-summer breakout, a bullish ‘flag’ pattern emerged for the October contract, with an ascending triangle in March. These patterns are quite reliable and sooner or later they break in the same direction of the underlying main trend – to the upside in this case.

Contrary to popular opinion

But how do we match up the dogged upward trend with the apparently overwhelming view the price rally is overdone?

An answer may lie in contrary opinion strategy. Otherwise known as psychological analysis, it assumes the view taken by the majority is usually wrong. A trader using this strategy would work out if the majority are bullish or bearish, and take the opposite position.

The global sugar balance sheet has been in deficit since the 2015-16 season, providing an underlying bullish narrative. But physical traders and analysts have emphasized the day-to-day bearish factors in recent months: CS Brazil’s bumper harvest in the early part of the season, the chief posterchild. For traders incorporating contrary opinion strategy in their approach, they would counter by taking a bullish position.

Speculators have been playing an increasing role in the pricing dynamics. The latest Commitments of Traders showed a new record spec net long of 347,983 lots, or 31% of open interest. It’s a diverse grouping, with strategies at play based on the reading of physical fundamentals and algorithmic trading. But a psychological element of trading could form part of the strategies at play.

Seasoned market watchers will know ‘the market is overbought’ is exactly the type of comment you get which actually suggests the rally is not finished. When traders point to ‘higher and higher levels’ is when the market is most likely near a peak.

What factors then could see the ‘majority’ view move turn bullish?

Bearish factors such as CS Brazil have recently moved into the bulls’ armory, with falling stock levels in India providing another factor to fuel the bullish narrative.

Global sugar stocks viewed on days-of-use basis fell to 138 in 2015-16 from 163 days in 2014-15, and will only stretch to 123 days in 2016-17, according to data from FO Licht presented at a conference in Nairobi, Kenya, last week. The last time the ratio was this low was in 2010-11, when prices surged above 35 c/lb.

How then to guess when sugar might be topping out? If contrary opinion strategy is at play, look out for when the majority view (us included) talks about the overwhelming bullish fundamentals.

When specs’ long liquidation finally occurs, the sheer scale of the specs position could unleash a severe price shock.

In the meantime, the rally could yet have some way to run.