19 Apr 2016 | 16:30 UTC — Insight Blog

RIN generation is up, but more biofuels mandates are on the way

By Wes Swift

With the latest batch of EPA Moderated Transaction System data due to be released in the next few days, giving some insight into RIN trading in the US, now seems like an appropriate time to take a dive into the current RIN situation.

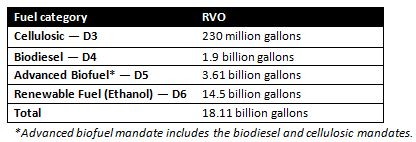

Last year, the biofuels industry produced 16.72 billion gallons of renewable fuels, generating 17.88 billion RINs. (Under the RFS, each gallon of biodiesel generates 1.5 RINs; hence the discrepancy between volume produced and RINs generated.)

Through the first two months of 2016, 2.844 billion total RINs have been generated on 2.687 billion gallons of renewable fuel. Compared with the same time frame in 2015, RIN generation is up 5% year on year.

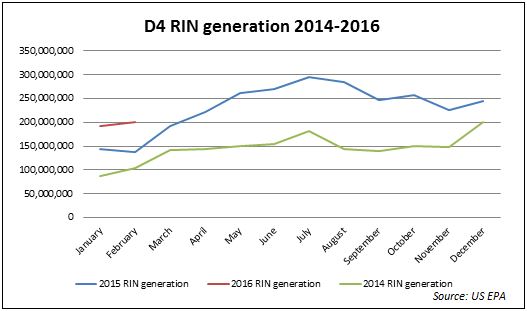

The biggest gain, percentage-wise, comes in D4 biodiesel RINs, which have increased 40% year on year through February. What’s most interesting is that, traditionally, biodiesel production and RIN generation is typically lowest in January and February. That could indicate that there could be quite a plethora of RINs by the end of the year, if previous production trends continue.

Since D4 biodiesel RINs can be used to satisfy three different portions of the RVO – the biodiesel, advanced biofuel or renewable fuel mandates – they are particularly useful in the RIN market. Hence, they’re priced higher compared with D5 and D6 RINs.

That robust RIN generation could be sorely needed. D5 advanced RINs are currently behind last year’s pace, at approximately 8 million RINs compared to last year’s 9.7 million through February. That’s most likely a reflection of the decrease in sugar cane ethanol imports into the US through the early part of the year. But the advanced mandate this year calls for 1.48 billion gallons of advanced fuel outside of the cellulosic and biodiesel mandates. Last year, advanced RIN generation came in at 146 million RINs, far below the 2016 mandate.

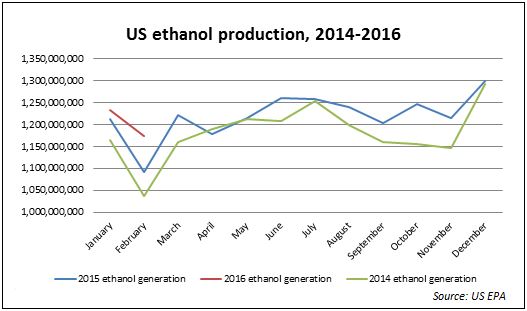

Meanwhile, ethanol RIN generation is ahead of last year’s pace, 2.426 million RINs compared with 2.333 million RINs in 2015. But February RIN generation fell to 1.18 billion RINs, below the 1.2 billion RINs per month needed to meet the 14.5 billion gallon mandate. But February usually is the lowest month for RIN generation as ethanol plants begin to shut down for maintenance.

Of course, the RIN market will be affected by more than just RINs generated this year. There’s still a large amount of RINs left over from 2015 that can be used to comply with up to 20% of this year’s RVOs. Published reports have placed the number of these “carry-over” RINs at 544 million D4 RINs and 1.46 billion D6 RINs.

Two key questions, though, will have an impact on RINs for the rest of the year.

First, will biofuel production and RIN generation continue at its current pace or slow down? At its current clip, biofuels RIN generation will come about substantially short of the required mandates. A large chunk of that deficit is in the advanced mandate, and certainly some of the robust biodiesel RIN generation can satisfy that burden. If production slows, however, obligated parties will have to tap into those banked “carry-over RINs,” taking away some of their flexibility.

Second, what will the EPA propose for its 2017 mandates for cellulosic, advanced and renewable fuel in June? (The EPA already released its 2017 biodiesel mandate, at 2.0 billion gallons.) The most volatile time for RIN prices comes in June and November, when the EPA publishes its proposed and final RVOs. If the 2017 mandates continue to climb, and if the number of carry-over RINs is liquidated to cover 2016 RVOs, it seems inevitable that RIN prices would be affected.